Whenever I am bored, I just go watch Alpha Series on @IIC_Conference

Learn something new everytime.

Watching @tusharbohra present on API industry

https://t.co/WYr2DIpVfD

Highly recommended.

More from Tar ⚡

"Rocket Emojis with to the moon tags"

this business wouldn't hit 3lk cr market cap in next 3 yrs but it can steadily compound at 25-30% YoY for next 10 yrs

At 25% CAGR over 10 yrs, you get a 10 bagger

Keep expectations in check.

Lets talk results #lauruslabs

— Tar \u26a1 (@itsTarH) July 29, 2021

Always zoom out and view the results, never take a QoQ approach.

Here is how Sales, Op.Profit and PAT looks like when you zoom out.

The upwards trends continues.

No business will move linearly up or linearly down. pic.twitter.com/O9UUt1rEE5

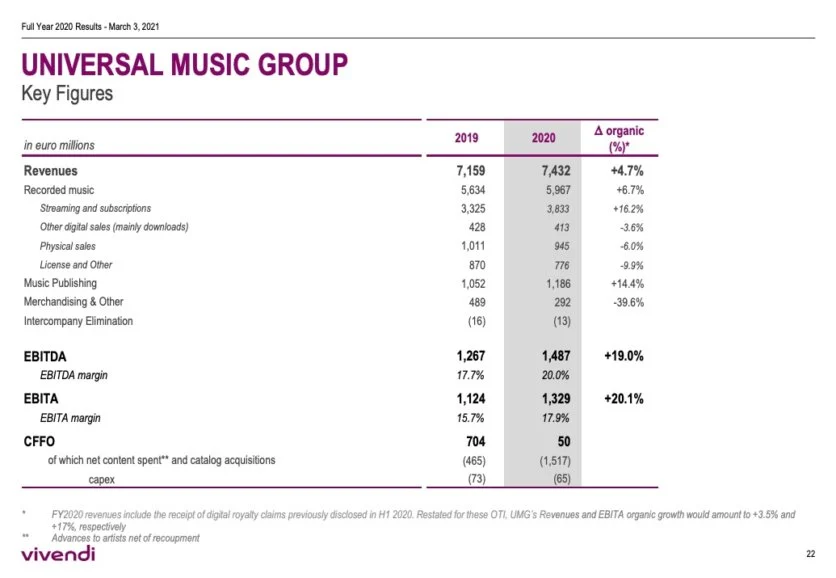

A business like Universal which controls more than 1/3rd of all published music globally is selling for less than 6x FY20 Sales.

Why are Indian businesses like Saregama / Tips selling for 11x, 20x their sales?

If I include all of the revenue generated by entire firm, its selling for ~4.5x FY20 Sales

Universal Listing Market Cap ~ 40 Billion USD

FY 20 Revenues ~ 8.87 B USD or 7.4B EUR

Catalogue of Music includes every international artist you can possibly name

Either Universal is grossly undervalued or Saregama/Tips are grossly overvalued.

https://t.co/aHzWSYtcUt

Homework for all the interested participants here:

— Intrinsic Compounding (@soicfinance) June 27, 2021

Q1.Why 20% and not 50%+ Margins for UMG

Q2. Differences in dynamics between Western&Indian cos?

Q3. Trends in West vs Trends in India in the industry.

Research and find the answers. My job is done \U0001f601\U0001f64f

https://t.co/v0EMoCuYKX

If you see the ebitda of universal music its low 20% compared to our saregama 30% or tips 50%. So when you compare earnings saregama is 40x and tips is 30x and universal music is 30x. Also these type of companies are less( low or no capex with excellent and growinh cashflows)

— Srikanth V (@mynameisnani75) June 27, 2021

You May Also Like

Like company moats, your personal moat should be a competitive advantage that is not only durable—it should also compound over time.

Characteristics of a personal moat below:

I'm increasingly interested in the idea of "personal moats" in the context of careers.

— Erik Torenberg (@eriktorenberg) November 22, 2018

Moats should be:

- Hard to learn and hard to do (but perhaps easier for you)

- Skills that are rare and valuable

- Legible

- Compounding over time

- Unique to your own talents & interests https://t.co/bB3k1YcH5b

2/ Like a company moat, you want to build career capital while you sleep.

As Andrew Chen noted:

People talk about \u201cpassive income\u201d a lot but not about \u201cpassive social capital\u201d or \u201cpassive networking\u201d or \u201cpassive knowledge gaining\u201d but that\u2019s what you can architect if you have a thing and it grows over time without intensive constant effort to sustain it

— Andrew Chen (@andrewchen) November 22, 2018

3/ You don’t want to build a competitive advantage that is fleeting or that will get commoditized

Things that might get commoditized over time (some longer than

Things that look like moats but likely aren\u2019t or may fade:

— Erik Torenberg (@eriktorenberg) November 22, 2018

- Proprietary networks

- Being something other than one of the best at any tournament style-game

- Many "awards"

- Twitter followers or general reach without "respect"

- Anything that depends on information asymmetry https://t.co/abjxesVIh9

4/ Before the arrival of recorded music, what used to be scarce was the actual music itself — required an in-person artist.

After recorded music, the music itself became abundant and what became scarce was curation, distribution, and self space.

5/ Similarly, in careers, what used to be (more) scarce were things like ideas, money, and exclusive relationships.

In the internet economy, what has become scarce are things like specific knowledge, rare & valuable skills, and great reputations.