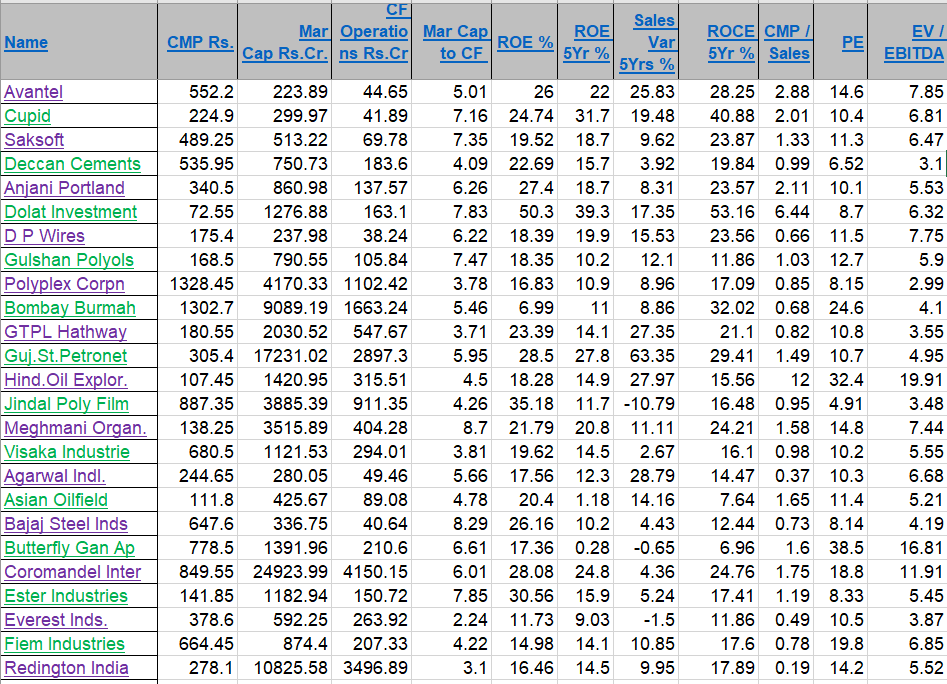

Financial Checklist !

Taking Maithan Alloys as Sample Stock !

Tax Payout Shown in 1n (above).

2n

Final Checklist for Buying Stocks - Dr Vijay Malik#Peacefulinvesting

— Dr Vijay Malik (@drvijaymalik) July 1, 2020

https://t.co/pjxiII2bkv via @drvijaymalik

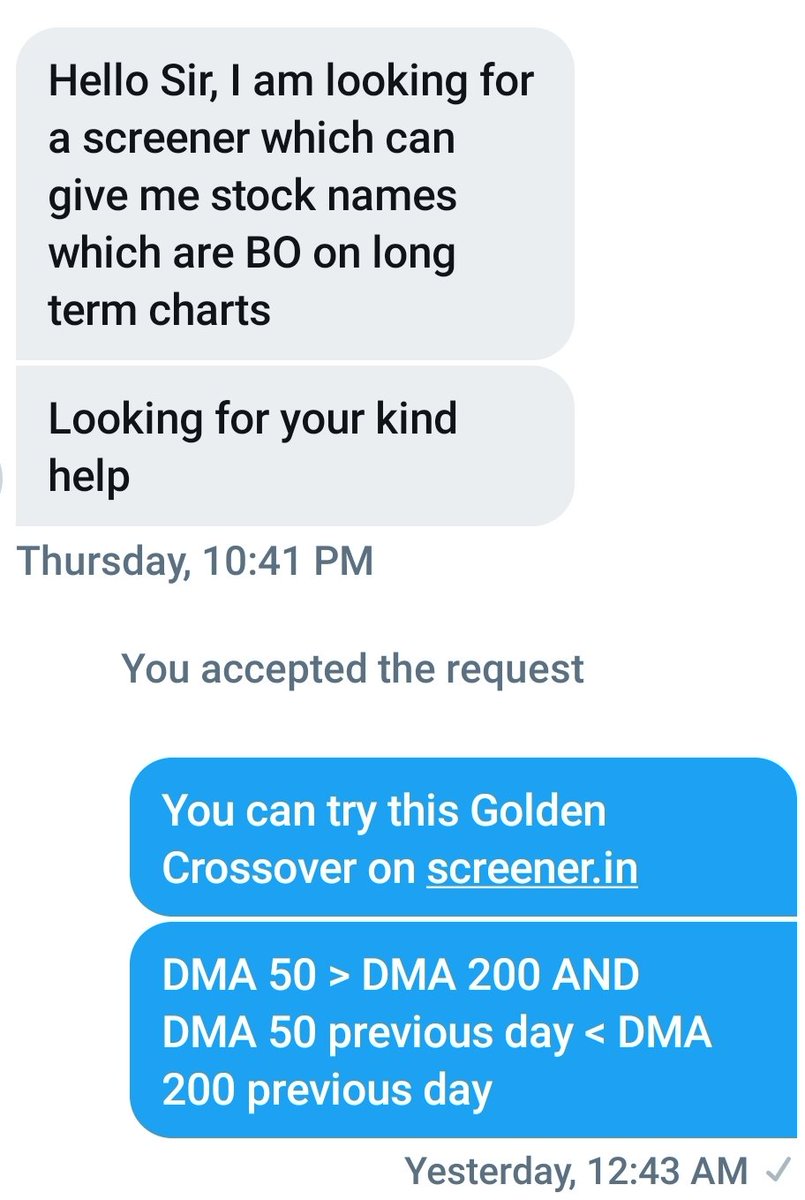

The absolute best 15 scanners which experts are using.

— Aditya Todmal (@AdityaTodmal) January 29, 2021

Got these scanners from the following accounts:

1. @Pathik_Trader

2. @sanjufunda

3. @sanstocktrader

4. @SouravSenguptaI

5. @Rishikesh_ADX

Share for the benefit of everyone.

If everyone was holding bitcoin on the old x86 in their parents basement, we would be finding a price bottom. The problem is the risk is all pooled at a few brokerages and a network of rotten exchanges with counter party risk that makes AIG circa 2008 look like a good credit.

— Greg Wester (@gwestr) November 25, 2018