https://t.co/mgWQbsFQGN

1/Today's @bopinion post is about Trump's taxes, and what they show about how America allocates capital.

We appear to have some big problems.

https://t.co/mgWQbsFQGN

Why would creditors give money to a guy who wastes the money on bad businesses and doesn't even pay them back?

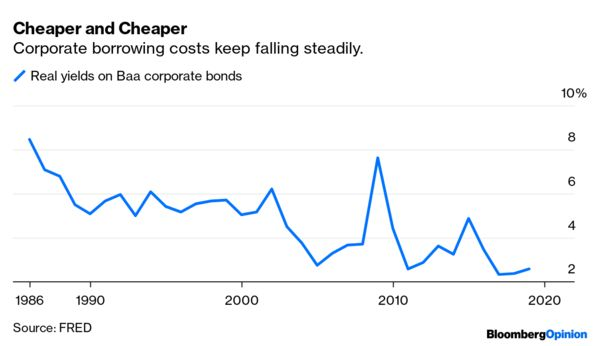

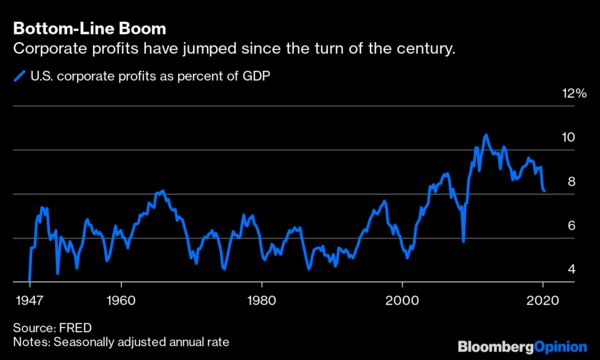

Why hasn't an abundance of cheap capital caused the return on financial capital to fall? Interest rates are low, but stock returns have held up strongly.

When you increase the supply of loanable funds, prices are supposed to go down. In other words, cheap capital should fund a lot of marginal businesses that compete away profits...

Simcha Barkai and Matt Rognlie have both written about this:

1. https://t.co/OLln8npr8b

2. https://t.co/BY1EWyluD7

https://t.co/xNzE9SO8nY

https://t.co/BY1EWyluD7

And it doesn't really explain Trump, does it? He's not a monopolist, and he doesn't even make profit. He's just a huckster who can borrow cheaply because he's famous.

Financiers are willing to throw tons of cheap money at big powerful companies or at famous hucksters like Trump, but charge inordinate prices to fund new entrants or marginal businesses.

We need to figure out what's going wrong, and fix it!

(end)

https://t.co/dHVCEQGa9q

More from Noah Smith 🐇

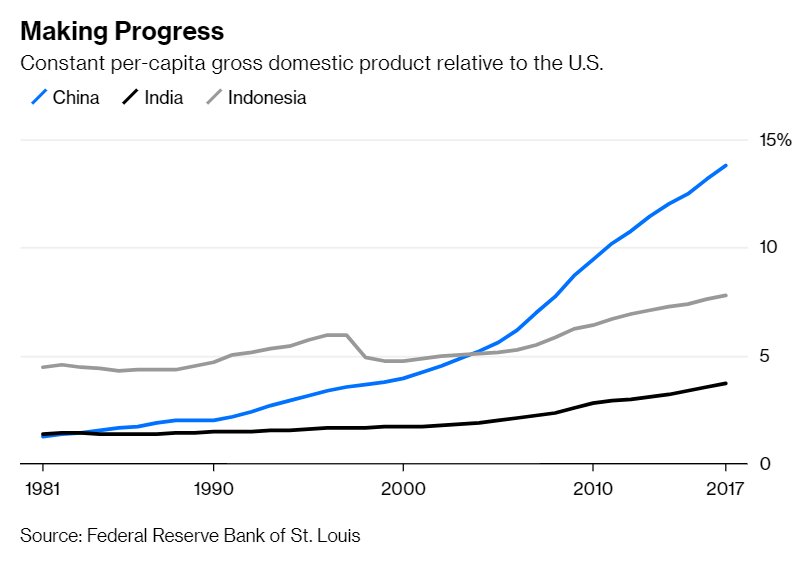

Today's @bopinion post is about how poor countries started catching up to rich ones.

It looks like decolonization just took a few decades to start

Basic econ theory says poor countries should grow faster than rich ones.

But for much of the Industrial Revolution, the opposite happened.

https://t.co/JjjVtWzz5c

Why? Probably because the first countries to discover industrial technologies used them to conquer the others!

But then colonial empires went away. And yet still, for the next 30 years or so, poor countries fell further behind rich ones.

https://t.co/hilDvv0IQV

Why??

Possible reasons:

1. Bad institutions (dictators, communism, autarkic trade regimes)

2. Civil wars

3. Lack of education

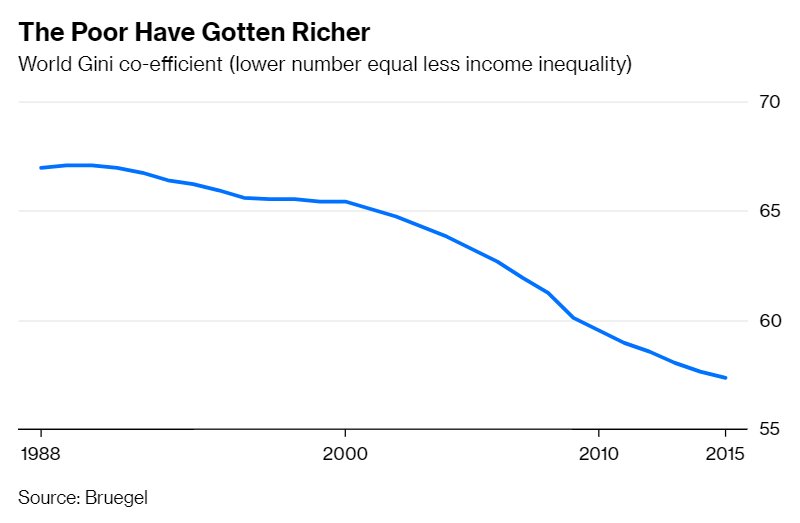

But then, starting in the 80s (for China) and the 90s (for India and Indonesia), some of the biggest poor countries got their acts together and started to catch up!

Global inequality began to fall.

It looks like decolonization just took a few decades to start

Basic econ theory says poor countries should grow faster than rich ones.

But for much of the Industrial Revolution, the opposite happened.

https://t.co/JjjVtWzz5c

Why? Probably because the first countries to discover industrial technologies used them to conquer the others!

But then colonial empires went away. And yet still, for the next 30 years or so, poor countries fell further behind rich ones.

https://t.co/hilDvv0IQV

Why??

Possible reasons:

1. Bad institutions (dictators, communism, autarkic trade regimes)

2. Civil wars

3. Lack of education

But then, starting in the 80s (for China) and the 90s (for India and Indonesia), some of the biggest poor countries got their acts together and started to catch up!

Global inequality began to fall.

Time for panel #3: Big Tech and regulation!

I will be live-tweeting again, and you can also watch video at either the Twitter or Facebook links below!

Kaissar: Every industry gets regulated when it gets big. The question is what kind of regulation Big Tech will get,and whether the companies will be proactive in shaping it.

Kaissar: More profitable companies have higher returns. Why? Maybe it's a risk factor, because more profit = higher risk of getting regulated.

Bershidskyis showing a diagram of GDPR complaince pop-ups. What a massive ill-conceived bureaucratic mess.

Ritholtz: It's 2018 and we're still talking about Facebook privacy settings?! If you're still giving your personal data to Facebook, you just don't care about privacy!

I will be live-tweeting again, and you can also watch video at either the Twitter or Facebook links below!

Bloomberg Ideas conference now starting! I will be live-tweeting it. You can watch on our Facebook or Twitter pages (links below)! https://t.co/Mbr9dZzWBy

— Noah Smith (@Noahpinion) October 25, 2018

Kaissar: Every industry gets regulated when it gets big. The question is what kind of regulation Big Tech will get,and whether the companies will be proactive in shaping it.

Kaissar: More profitable companies have higher returns. Why? Maybe it's a risk factor, because more profit = higher risk of getting regulated.

Bershidskyis showing a diagram of GDPR complaince pop-ups. What a massive ill-conceived bureaucratic mess.

Ritholtz: It's 2018 and we're still talking about Facebook privacy settings?! If you're still giving your personal data to Facebook, you just don't care about privacy!

More from Trump

Having a Twitter account is not a right.

If you incite violence on Twitter, the company can - and should - stop you. Good call.

Plans for “future armed protests” are spreading on Twitter and elsewhere, the company warned, “including a proposed secondary attack on the US Capitol and state capitol buildings on January 17, 2021”.

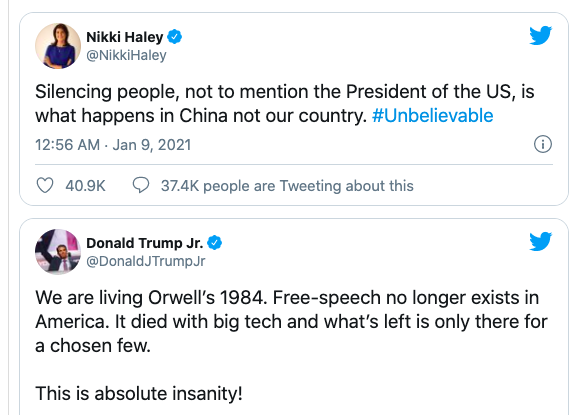

Yes, people who boosted their careers off of Trump - his sycophants, his kids & people like Haley, who helped him attack and undermine human rights around the world - are boo-hooing right now.

Always beware of powerful people pretending to be victims.

https://t.co/0A5D5eJFvL

But no one should react with glee. The president of the United States has been inciting violence, and Republican Party leaders, along with a willing, violent mob, have been aiding his attempts to overthrow the democratic process.

That's the real story here.

The dangers are real, and we've all seen them. That Twitter even had to contemplate banning any politician for inciting violence is awful. That they had to ban the sitting president for it is even worse.

If you incite violence on Twitter, the company can - and should - stop you. Good call.

Plans for “future armed protests” are spreading on Twitter and elsewhere, the company warned, “including a proposed secondary attack on the US Capitol and state capitol buildings on January 17, 2021”.

Yes, people who boosted their careers off of Trump - his sycophants, his kids & people like Haley, who helped him attack and undermine human rights around the world - are boo-hooing right now.

Always beware of powerful people pretending to be victims.

https://t.co/0A5D5eJFvL

But no one should react with glee. The president of the United States has been inciting violence, and Republican Party leaders, along with a willing, violent mob, have been aiding his attempts to overthrow the democratic process.

That's the real story here.

The dangers are real, and we've all seen them. That Twitter even had to contemplate banning any politician for inciting violence is awful. That they had to ban the sitting president for it is even worse.