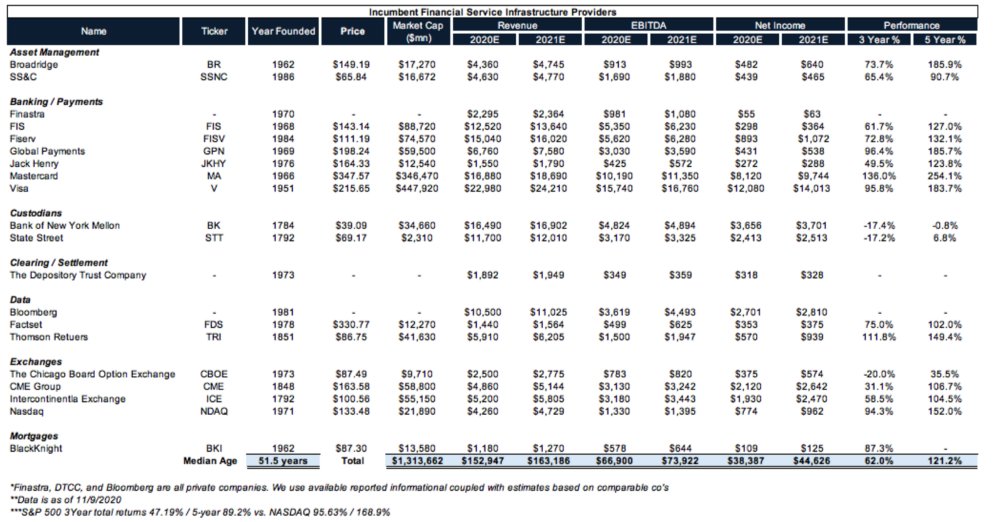

0/ We've highlighted FinTech infrastructure co's like BR, FIS, JKHY, MA, V, ICE, NDAQ, etc. as companies w/ a variety of moats that have led to dominant mkt share & outperformance despite being 50+ years old on avg.

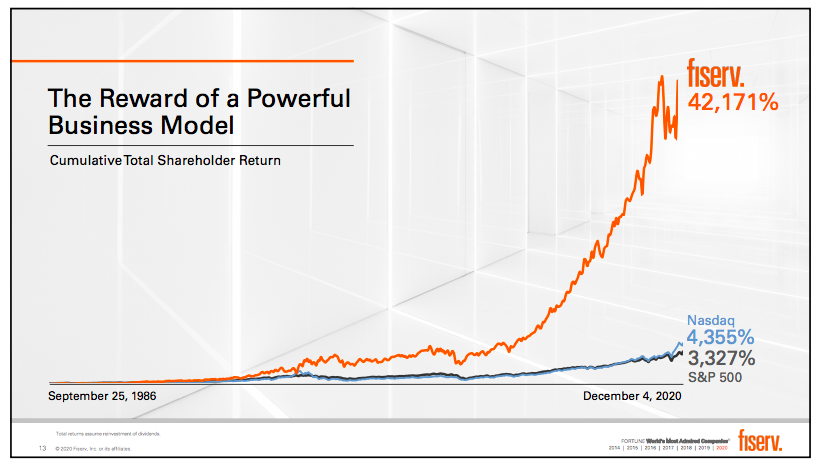

$FISV had their investor day yesterday and laid out the why.

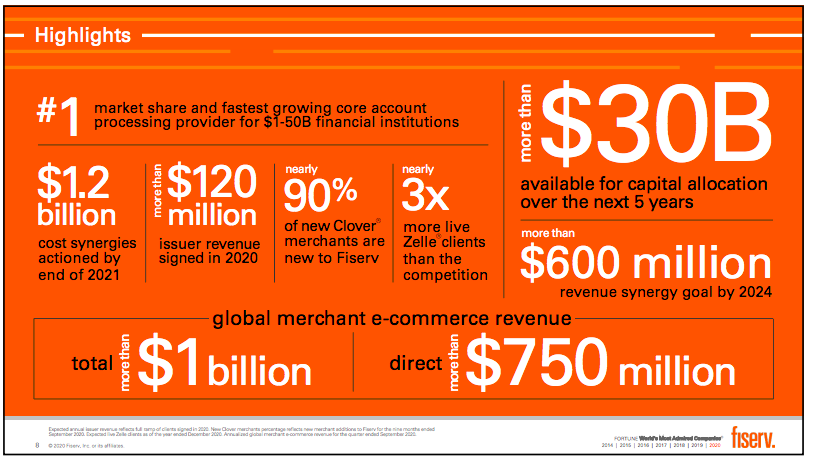

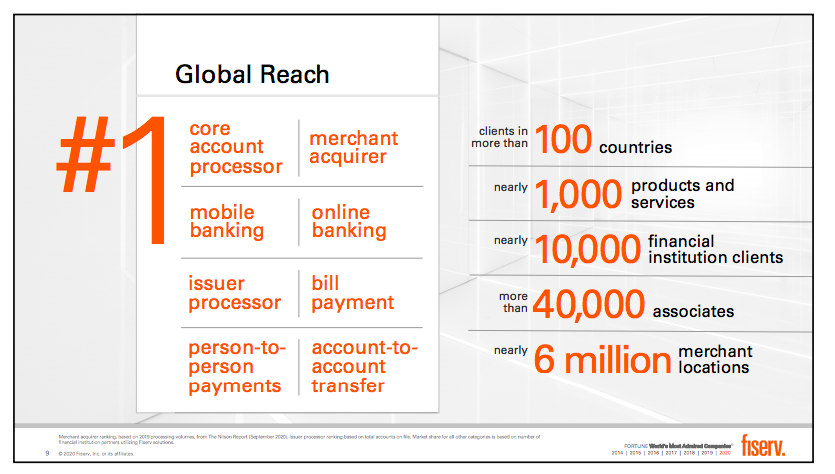

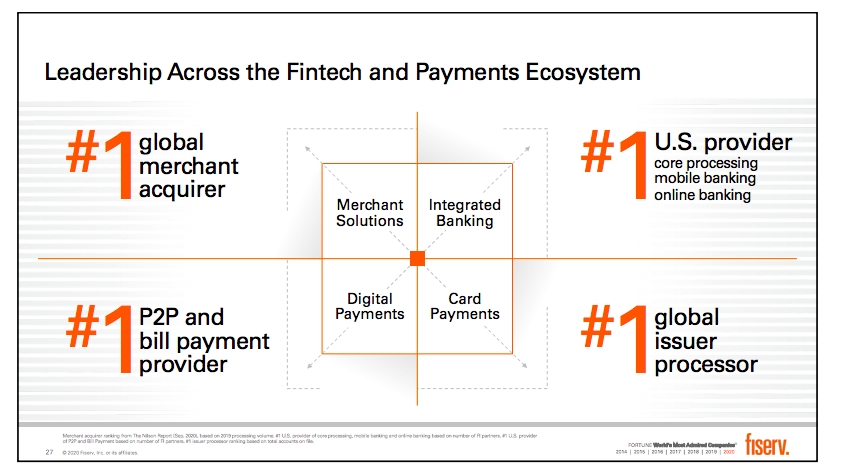

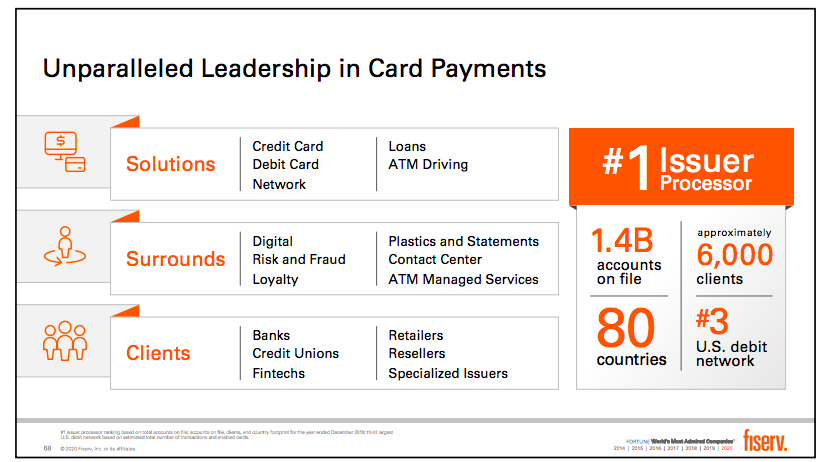

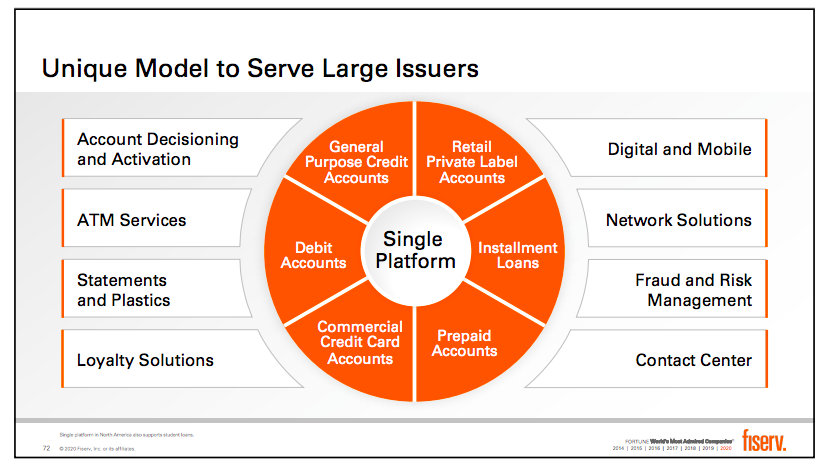

All while being #1 as a core account processor, merchant acquirer, bill pay, P2P payments, etc...

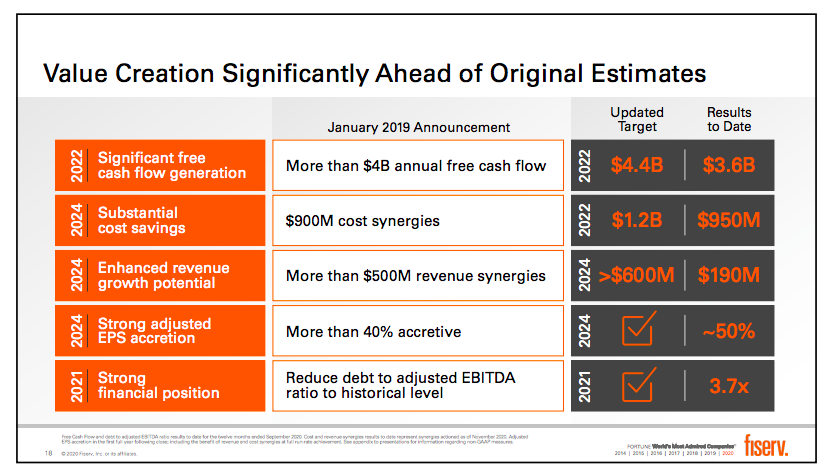

They highlight the progress on the deal & new goals post integration.

M&A is a skill & FISV has it financially; tech integration leaves something to be desired

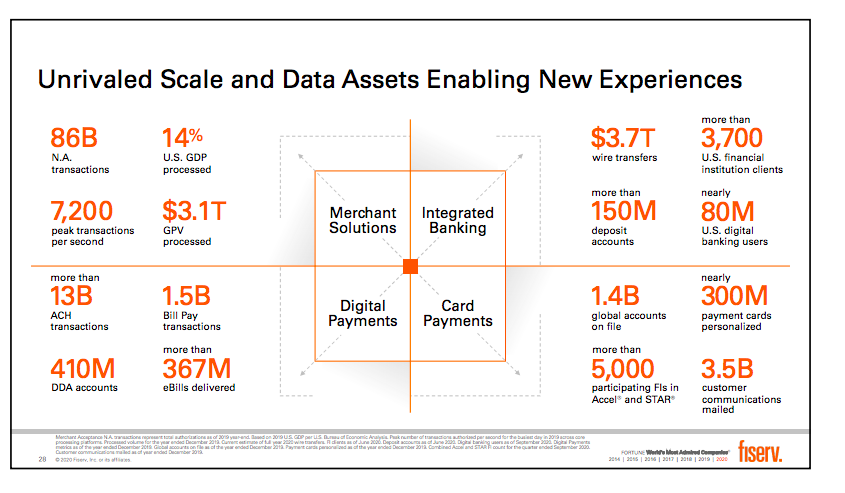

(i) Merchant Solutions

(ii) Integrated Banking

(iii) Digital Payments

(iv) Card Payments

They conduct more than 12,000 financial tx / second & reach nearly ~100% of US households

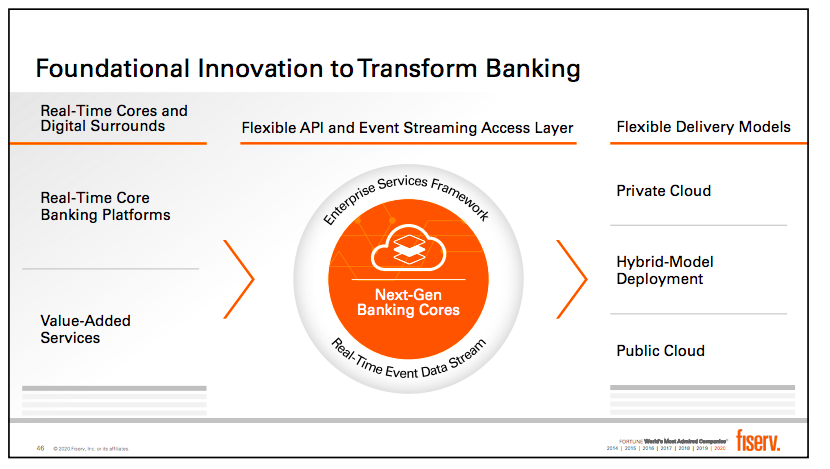

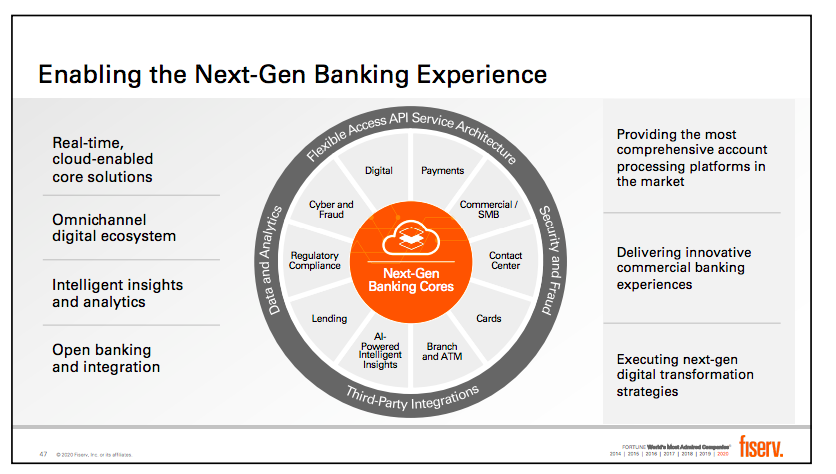

(i) Flexible API Service Architecture

(ii) Security & Fraud Tools

(iii) Third Party Integrations

(iv) Data & Analytics

This is a slide I imagine a number of BaaS companies look to emulate in future decks.

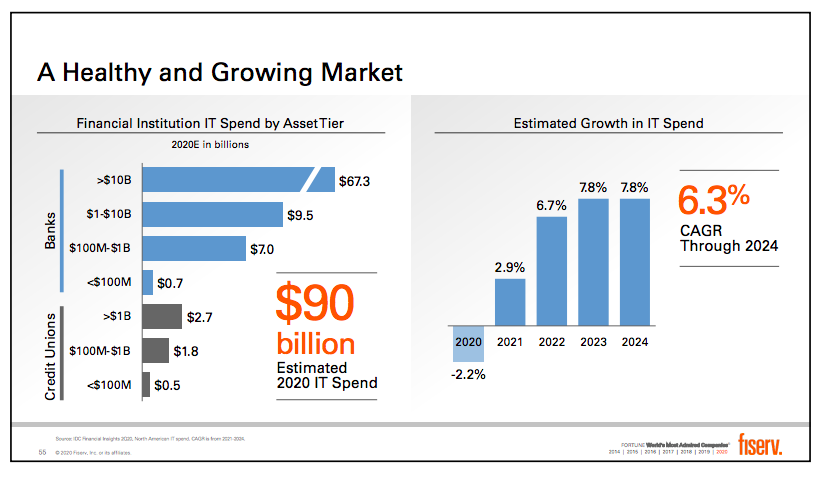

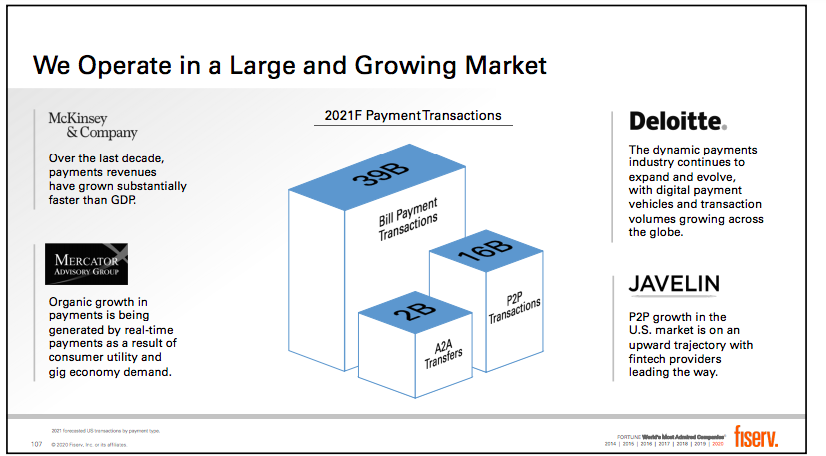

They believe $90B was spent in '20 by Financial Institution on IT which is projected to grow at a 6.3% CAGR through '24.

For those that believe FinTech B2B infrastructure is saturated thats a portion of the pie

With talks of @Marqeta going public next year this will be an interesting comp for this business line.

This is part of the oppty co's like Marqeta & Galileo saw $FISV won't entertain the startup.

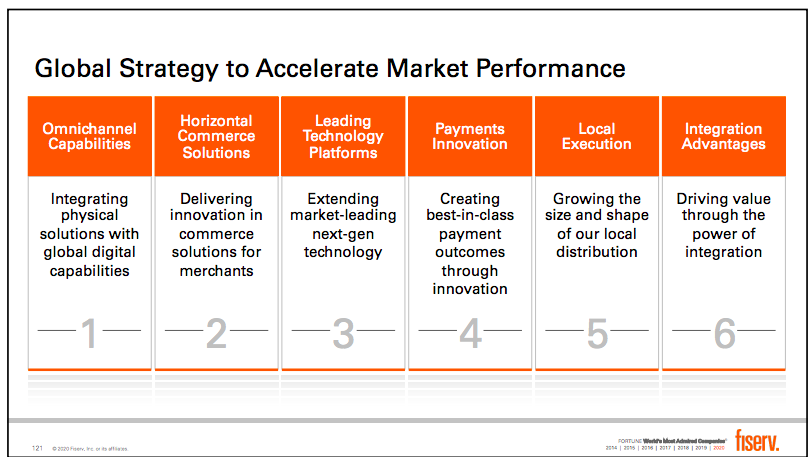

(i) Omnichannel Capabilities

(ii) Horizontal Commerce Solutions

(iii) Leading Technology

(iv) Payments Innovation

(v) Local Execution

(vi) Integration Advantages

More from Trading

DJ @ITRADE191 multiple chart analysis for INTRADAY TRADING.

1. Core setup

2. Pivot points trades

3. PDH/PDL trades

4. Open interest addictions combined with rejections on charts.

5. Website to confirm bias

Very quick read.

Share if you liked for the benefit of everyone.

•Main setup of @ITRADE191

He used this setup daily for all trades.

1. EMA crossover 10/20

2. Supertrend 10/3

3. Vwap

4. RSI >

•Volume always greater than

•Candle Rejecting from

•Pivot settings

1. Core setup

2. Pivot points trades

3. PDH/PDL trades

4. Open interest addictions combined with rejections on charts.

5. Website to confirm bias

Very quick read.

Share if you liked for the benefit of everyone.

•Main setup of @ITRADE191

He used this setup daily for all trades.

1. EMA crossover 10/20

2. Supertrend 10/3

3. Vwap

4. RSI >

@MiteshFan @Mitesh_Engr @Abhishekkar_ MY TRADING SETUP .... I've been using it for a long time .. result good try it \U0001f607 pic.twitter.com/XThUD0ftbl

— itrade(DJ) (@ITRADE191) June 13, 2020

•Volume always greater than

Volume Should always be above 20 pic.twitter.com/CPgxLgpPKF

— itrade(DJ) (@ITRADE191) June 13, 2020

•Candle Rejecting from

— itrade(DJ) (@ITRADE191) August 25, 2020

•Pivot settings

— itrade(DJ) (@ITRADE191) October 20, 2020