Am sharing my journey on how I started trading 15 years before when there was very limited resource. If you are a beginner who is looking to get started with Stock Market, this thread would be helpful.\U0001f9f5

— Kirubakaran Rajendran (@kirubaakaran) April 26, 2022

I have shared multiple information related to trading and investing through my historical data analysis by writing various articles, here's the master thread that contains all my work in one place.🧵

Many of my friends who work at Corporate culture are fed up with their work life, one question they keep asking me is how much money do I need to retire and live comfortably? Here\u2019s a short thread \U0001f9f5 pic.twitter.com/gNEOFOChlh

— Kirubakaran Rajendran (@kirubaakaran) May 24, 2022

Year 2022 has been disastrous for many asset classes, the world economy is at 40 year high inflation. Are we headed for another stock market crash? Here's a detailed analysis. \U0001f9f5 pic.twitter.com/ZYch9yBHEq

— Kirubakaran Rajendran (@kirubaakaran) May 19, 2022

I have closely observed FinNifty for couple of weeks and then started trading live since last 4 expiry. If you are looking to start trading with FinNifty weekly option then this thread might be of great help to you. \U0001f9f5

— Kirubakaran Rajendran (@kirubaakaran) July 12, 2022

Here's a detailed analysis of 920 Straddle with 25% SL using @stockmock_in platform. This analysis would show which days are max profitable, how it behaves on gap days and how it behaves on different VIX days. \U0001f9f5

— Kirubakaran Rajendran (@kirubaakaran) May 8, 2022

Every time after I make a SIP investment, market tends to go down in next couple of days. I always wondered I would have made higher returns with my SIP if I waited for market correction. Does making SIP during market correction generates higher returns. Here\u2019s the details \U0001f9f5 pic.twitter.com/bsnz9ySi96

— Kirubakaran Rajendran (@kirubaakaran) June 29, 2022

What is Rakesh Jhunjhunwala's Investing Strategy, is there a way where we retail investors can follow his strategy and generate similar returns like him? We did an extensive research and this is what we found. A short thread pic.twitter.com/2gq9vNqv22

— Kirubakaran Rajendran (@kirubaakaran) September 29, 2021

A small thread on Mindset of a successful trader. What differentiates best traders from the bad ones? Why 95% of the traders don\u2019t make money? Trading is an unpredictable game, how could one win in that? 1/n pic.twitter.com/ZHMZ2wZXxK

— Kirubakaran Rajendran (@kirubaakaran) March 25, 2021

A short thread on The 80/20 rule for Trading and Investing. If you really want to improve your trading result, follow this one simple approach which can immediately show you the reason why you weren\u2019t able to make profits in the stock market. pic.twitter.com/2clnYVzahE

— Kirubakaran Rajendran (@kirubaakaran) May 4, 2021

In general, making money from trading is real hard than any other business. And I believe discretionary trading is even more harder. Why do many beginners go bust within 90 days of their trading career? Here's a short thread on why discretionary trading is hard? pic.twitter.com/4av9E0YSkm

— Kirubakaran Rajendran (@kirubaakaran) November 18, 2021

Most beginners when building a trading strategy simply use current info and test with it, they don't know How to Get Historical Stock Futures lot size, list of stocks that are part of index like Nifty 50, Nifty 500 historically, I will share all such info in this thread

— Kirubakaran Rajendran (@kirubaakaran) September 9, 2021

Russian stock market crashed more than 70%, many investors are worried on what would happen if such things happen to Indian markets? Here's couple of important lesson you need to keep in mind before you start your SIP journey. A short thread pic.twitter.com/m0QQ1aGnsN

— Kirubakaran Rajendran (@kirubaakaran) March 8, 2022

Are you a trader who did an extensive backtest of your trading strategy only to witness a worst performance when you traded live? Wondering why your real live results are not matching with your backtest results? Then this short thread is for you. pic.twitter.com/sx8WsGeejJ

— Kirubakaran Rajendran (@kirubaakaran) February 24, 2022

Should you buy stocks that gets added to #Nifty50. A short thread with detailed analysis from 25+ years of Historical data. Nifty 50 is widely tracked index, all stocks that are being included/excluded with Nifty 50 will have an impact towards the stock returns for next one year pic.twitter.com/XUtYSUl0mm

— Kirubakaran Rajendran (@kirubaakaran) June 13, 2021

Investing for long term is always projected as a complex task, reading about the nature of company business, balance sheets, Profit and loss statements etc. Is there any easy way to find the best stocks to invest for long term? That's what this thread is all about. pic.twitter.com/DJw06FMfw2

— Kirubakaran Rajendran (@kirubaakaran) March 21, 2022

Many beginners give utmost importance to trading strategy but least bothered about position sizing. Knowing how much is too much in a trade? This information is very crucial which determines the long term success of a trader. In this thread will explain what is position sizing pic.twitter.com/tkuOJ3JQ6L

— Kirubakaran Rajendran (@kirubaakaran) March 1, 2022

Here's a thread on complete data analysis of #NSE500 stocks, to start with, first checked the momentum factor, what was the last 12 months returns of all sectors of NSE 500. IT sector stocks top the list with average returns of 90% in last one year. 1/n pic.twitter.com/3VwS5XY11Z

— Kirubakaran Rajendran (@kirubaakaran) March 2, 2021

A thread on Position Sizing #Trading is the only profession where you can see Doctors, Engineers, and many other successful professionals try their luck with stock market, these people excel in their own respective field but struggle a lot when it comes to trading.1/n

— Kirubakaran Rajendran (@kirubaakaran) February 16, 2021

Nifty 14500 CE trade which made day low price of 0.15 and day high price of 2139, due to erroneous order by a broker who lost 250 crores. Some ppl claim few others brokers made 50 to 75 crores profits. But what really happened? Here's the tick data analysis that shows true info\U0001f9f5

— Kirubakaran Rajendran (@kirubaakaran) June 3, 2022

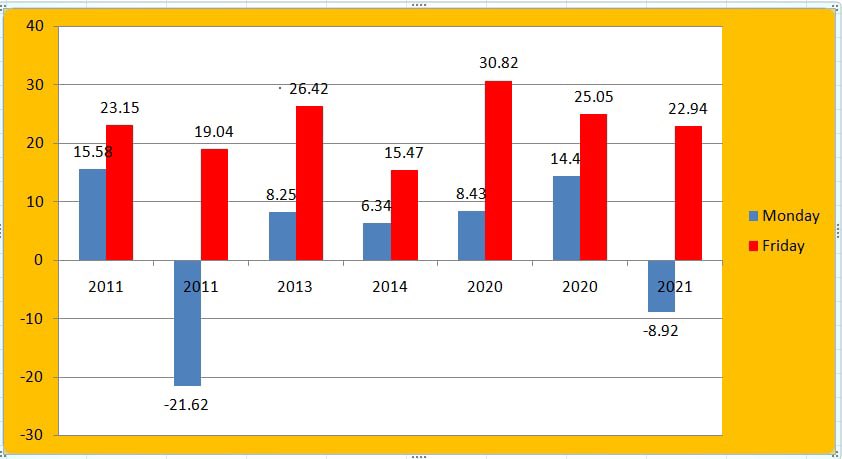

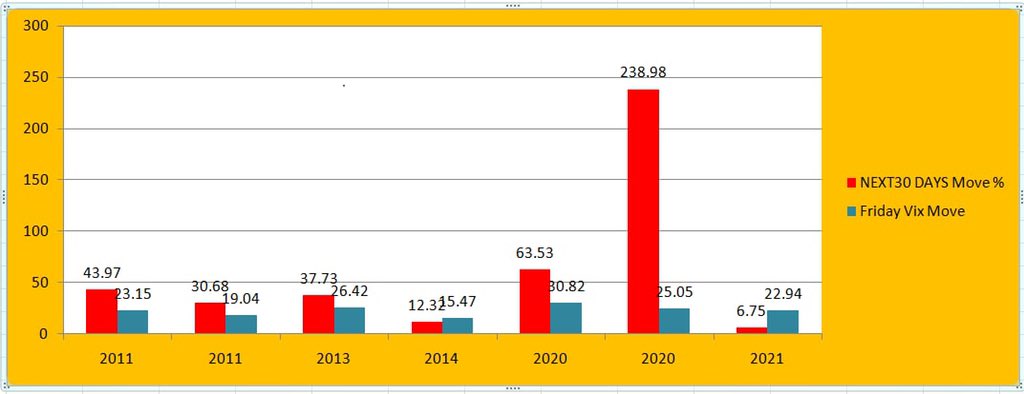

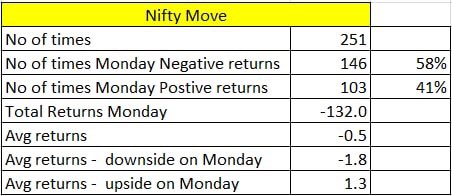

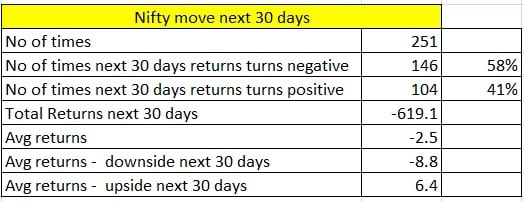

Whenever #Nifty & #BankNifty closes less than -1% on Fridays, what happens on Monday and what happens on next 30 days. Interesting analysis, will be sharing the details shortly.

— Kirubakaran Rajendran (@kirubaakaran) November 27, 2021

What happens if we buy a stock in cash segment that gets added to F&O ban list and sell that stock once it comes of F&O ban list. Tested this #TradingStrategy with last 5 years of historical data, here's the details. pic.twitter.com/dcFLkX49jY

— Kirubakaran Rajendran (@kirubaakaran) October 20, 2021

When it comes to investing, most beginners who want to get started with stock market investing opt for mutual funds. But do you know how many mutual funds there are in India? There are more than 2,500\xa0mutual fund schemes.

— Kirubakaran Rajendran (@kirubaakaran) June 8, 2022

How do we decide which one to invest?Here\u2019s a short \U0001f9f5 pic.twitter.com/tIp14488hE

Monthly SIP is one most underrated investment option many people tend to ignore during their early stage of professional career. You really don\u2019t need to invest lot of money, in fact just investing Rs.5000 every month at the Age of 25 can you fetch you almost 2 Crores corpus. \U0001f9f5

— Kirubakaran Rajendran (@kirubaakaran) June 20, 2022

\u201cWhenever I enter into a trade, I end up losing money. Should I stop trading and start investing?\u201d This is a common question that comes in our mind very often during our early phase. Here\u2019s a short thread that explains what we are doing wrong and how to correct it?

— Kirubakaran Rajendran (@kirubaakaran) May 11, 2022

More from Kirubakaran Rajendran

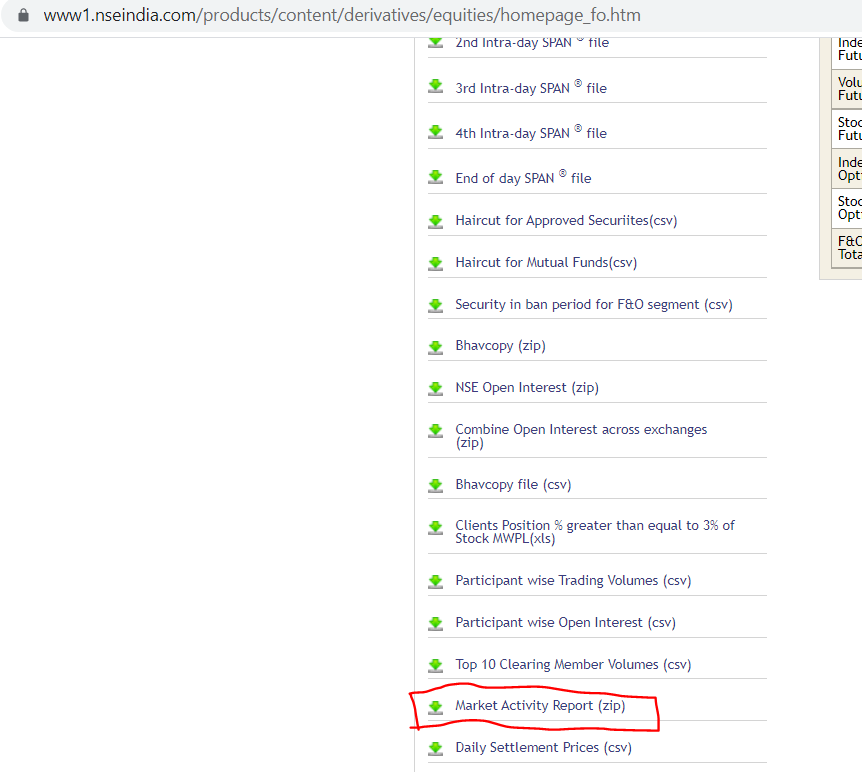

Most beginners when building a trading strategy simply use current info and test with it, they don't know How to Get Historical Stock Futures lot size, list of stocks that are part of index like Nifty 50, Nifty 500 historically, I will share all such info in this thread

Please note that there is no way to get the historical lot size of stocks futures, NSE don't publish it directly, so we need to do some calculated steps to get that data. Download Market Activity report https://t.co/HKLkSVtXEI

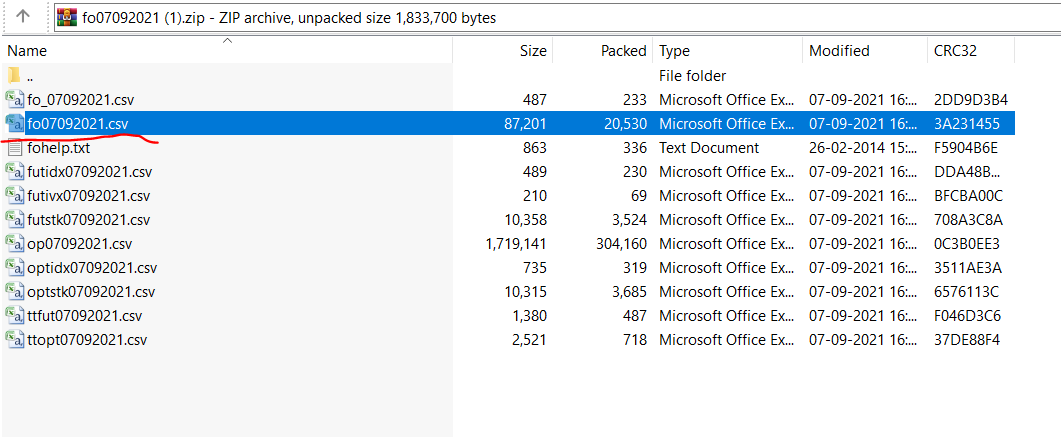

The zip file contains multiple files, open the second file.

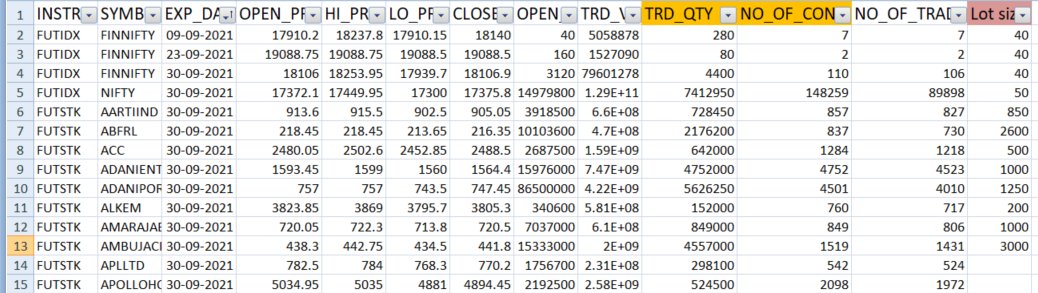

The file will contain stock symbol, expiry date, OHLC data, along with that you get traded quantity and No of contracts traded, using this data we can calculate the lot size of every stock symbol. Simply divide Traded QTY / NO of contracts gives you the lot size.

So to get the historical stock futures data, all you need to do is change the date in the below link

https://t.co/xIBXsPpIVt For an example, to get the historical stock futures lot size data for Sep 2016, use https://t.co/Criu7S3Fi5

Please note that there is no way to get the historical lot size of stocks futures, NSE don't publish it directly, so we need to do some calculated steps to get that data. Download Market Activity report https://t.co/HKLkSVtXEI

The zip file contains multiple files, open the second file.

The file will contain stock symbol, expiry date, OHLC data, along with that you get traded quantity and No of contracts traded, using this data we can calculate the lot size of every stock symbol. Simply divide Traded QTY / NO of contracts gives you the lot size.

So to get the historical stock futures data, all you need to do is change the date in the below link

https://t.co/xIBXsPpIVt For an example, to get the historical stock futures lot size data for Sep 2016, use https://t.co/Criu7S3Fi5

More from Thread

This is a result of credit fueled big ticket purchases of which buying a home is a big component. No amount of saving will cover the housing EMIs payable over one year. To this, add EMIs of 1 or 2 cars, and you've monthly EMIs running into 1 Lakh+. Now, add monthly house-hold +

+ expense, school fee and other sundry expenses and suddenly, you'll find a family unable to sustain itself w/o cash-flow for even 3-4 months. And most important of them all -

HAVING ASSETS IS NOT SAME AS HAVING CASH.

+

+ From personal experience, I think this is what you need to do:

- Maintain between Rs 1-2 Lakhs in emergency cash at all times.

- Use your Credit Cards wisely. They can be good source of large credit in an emergency.

- Work out your monthly house-hold expenses and EMIs

+

- Build a cash-reserve to cover your household expenses for a 6-month or 1-year period.

- Consider food, electricity, mobile/internet, your kids school fee, fuel, rent etc.

- Then work out your EMI obligations and see what level of reserves you can create for them.

- Maintain+

+ this back-up fund in cash/near cash assets.

- So, that you can utilize them as per requirement and are not subject to market forces.

One thing I\u2019ve learnt from the Covid catastrophe is that the so many batch mates from engineering (and maybe b school) have no savings. So many people with like 20 years of really affluent work experience are two month\u2019s salary away from crowd funding to feed their families.

— Sidin (@sidin) July 9, 2021

+ expense, school fee and other sundry expenses and suddenly, you'll find a family unable to sustain itself w/o cash-flow for even 3-4 months. And most important of them all -

HAVING ASSETS IS NOT SAME AS HAVING CASH.

+

+ From personal experience, I think this is what you need to do:

- Maintain between Rs 1-2 Lakhs in emergency cash at all times.

- Use your Credit Cards wisely. They can be good source of large credit in an emergency.

- Work out your monthly house-hold expenses and EMIs

+

- Build a cash-reserve to cover your household expenses for a 6-month or 1-year period.

- Consider food, electricity, mobile/internet, your kids school fee, fuel, rent etc.

- Then work out your EMI obligations and see what level of reserves you can create for them.

- Maintain+

+ this back-up fund in cash/near cash assets.

- So, that you can utilize them as per requirement and are not subject to market forces.

Lifelong learning is a competitive advantage.

But contrary to what you’ve been told, lifelong learners are built, not born.

THREAD: 20 lifelong learning habits you can start developing today.

Stimulate Dynamically

The mind is a muscle - it needs to be stimulated dynamically to continue to grow.

Don’t rely on one “exercise” - develop a menu of options.

Write, read, listen, watch. Solve puzzles, play games. Enjoy it!

Stimulate dynamically, learn dynamically.

Build Learning Circles

The most powerful learning is communal, not individual.

Build learning circles with other intellectually curious minds.

Engage regularly with no set intention or goal.

Community is everything. Embrace it.

Keep Asking Why

“Why?” is the most useful tool in our learning toolkit.

But somewhere along the line, we are told to stop asking why and just accept “facts” as we are told them.

Reject the norm.

If you want to understand the world, take a cue from our kids - keep asking why!

Adopt a Process Orientation

Prioritize process.

Learn for the sake of learning, not always for a specific goal.

When you prioritize process, you become flexible in where you are headed.

Life is a winding, confusing journey - forward progress is all that matters.

But contrary to what you’ve been told, lifelong learners are built, not born.

THREAD: 20 lifelong learning habits you can start developing today.

Stimulate Dynamically

The mind is a muscle - it needs to be stimulated dynamically to continue to grow.

Don’t rely on one “exercise” - develop a menu of options.

Write, read, listen, watch. Solve puzzles, play games. Enjoy it!

Stimulate dynamically, learn dynamically.

Build Learning Circles

The most powerful learning is communal, not individual.

Build learning circles with other intellectually curious minds.

Engage regularly with no set intention or goal.

Community is everything. Embrace it.

Keep Asking Why

“Why?” is the most useful tool in our learning toolkit.

But somewhere along the line, we are told to stop asking why and just accept “facts” as we are told them.

Reject the norm.

If you want to understand the world, take a cue from our kids - keep asking why!

First principles thinking is a powerful mental model for driving non-linear outcomes. It also requires a willingness to ask difficult, uncomfortable questions.

— Sahil Bloom (@SahilBloom) March 14, 2021

Here are a few to help you get started: pic.twitter.com/KyuAr7IUf7

Adopt a Process Orientation

Prioritize process.

Learn for the sake of learning, not always for a specific goal.

When you prioritize process, you become flexible in where you are headed.

Life is a winding, confusing journey - forward progress is all that matters.