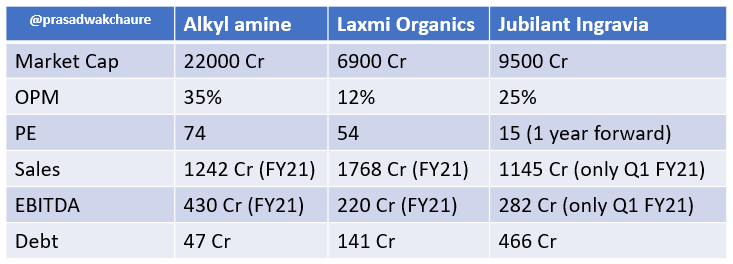

Why #JubilantIngrevia can be next big growth story?

Here is the thread.

Pharma serving to regulated market are under stress due product price erosion. Market is comfortably giving higher multiples to step down segment in value chain i.e. raw material suppliers.

Jubilant Ingravia has posted superb Q1 numbers which fetched my attention. Stock is trading below one year forward 15x PE multiples & 2x of sales.

Key points:

Super diversified product & client portfolio

Leadership position for many products in India and in the World

Last year company reduced debt by 600 Cr while lined up 900 Cr Capex for next 3 years

1.Molasses to Ethanol to Acetaldehyde to Pyridine derivatives to Nutritional products

2.Ethanol to acetic anhydride

3.Ethanol to ethyl acetate

4. Ethanol to acetic acid to ketene to Diketene

https://t.co/8ZAj2kgcHE

Research report by @VineetGala is nice read

https://t.co/R1pKR7CbMg

You May Also Like

This is NONSENSE. The people who take photos with their books on instagram are known to be voracious readers who graciously take time to review books and recommend them to their followers. Part of their medium is to take elaborate, beautiful photos of books. Die mad, Guardian.

THEY DO READ THEM, YOU JUDGY, RACOON-PICKED TRASH BIN

If you come for Bookstagram, i will fight you.

In appreciation, here are some of my favourite bookstagrams of my books: (photos by lit_nerd37, mybookacademy, bookswrotemystory, and scorpio_books)

Beautifully read: why bookselfies are all over Instagram https://t.co/pBQA3JY0xm

— Guardian Books (@GuardianBooks) October 30, 2018

THEY DO READ THEM, YOU JUDGY, RACOON-PICKED TRASH BIN

If you come for Bookstagram, i will fight you.

In appreciation, here are some of my favourite bookstagrams of my books: (photos by lit_nerd37, mybookacademy, bookswrotemystory, and scorpio_books)

@EricTopol @NBA @StephenKissler @yhgrad B.1.1.7 reveals clearly that SARS-CoV-2 is reverting to its original pre-outbreak condition, i.e. adapted to transgenic hACE2 mice (either Baric's BALB/c ones or others used at WIV labs during chimeric bat coronavirus experiments aimed at developing a pan betacoronavirus vaccine)

@NBA @StephenKissler @yhgrad 1. From Day 1, SARS-COV-2 was very well adapted to humans .....and transgenic hACE2 Mice

@NBA @StephenKissler @yhgrad 2. High Probability of serial passaging in Transgenic Mice expressing hACE2 in genesis of SARS-COV-2

@NBA @StephenKissler @yhgrad B.1.1.7 has an unusually large number of genetic changes, ... found to date in mouse-adapted SARS-CoV2 and is also seen in ferret infections.

https://t.co/9Z4oJmkcKj

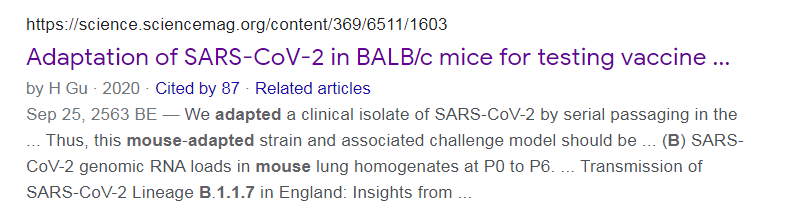

@NBA @StephenKissler @yhgrad We adapted a clinical isolate of SARS-CoV-2 by serial passaging in the ... Thus, this mouse-adapted strain and associated challenge model should be ... (B) SARS-CoV-2 genomic RNA loads in mouse lung homogenates at P0 to P6.

https://t.co/I90OOCJg7o

@NBA @StephenKissler @yhgrad 1. From Day 1, SARS-COV-2 was very well adapted to humans .....and transgenic hACE2 Mice

1. From Day 1, SARS-COV-2 was very well adapted to humans .....and transgenic hACE2 Mice

— Billy Bostickson \U0001f3f4\U0001f441&\U0001f441 \U0001f193 (@BillyBostickson) January 30, 2021

"we generated a mouse model expressing hACE2 by using CRISPR/Cas9 knockin technology. In comparison with wild-type C57BL/6 mice, both young & aged hACE2 mice sustained high viral loads... pic.twitter.com/j94XtSkscj

@NBA @StephenKissler @yhgrad 2. High Probability of serial passaging in Transgenic Mice expressing hACE2 in genesis of SARS-COV-2

1. High Probability of serial passaging in Transgenic Mice expressing hACE2 in genesis of SARS-COV-2!

— Billy Bostickson \U0001f3f4\U0001f441&\U0001f441 \U0001f193 (@BillyBostickson) January 2, 2021

2 papers:

Human\u2013viral molecular mimicryhttps://t.co/irfH0Zgrve

Molecular Mimicryhttps://t.co/yLQoUtfS6s https://t.co/lsCv2iMEQz

@NBA @StephenKissler @yhgrad B.1.1.7 has an unusually large number of genetic changes, ... found to date in mouse-adapted SARS-CoV2 and is also seen in ferret infections.

https://t.co/9Z4oJmkcKj

@NBA @StephenKissler @yhgrad We adapted a clinical isolate of SARS-CoV-2 by serial passaging in the ... Thus, this mouse-adapted strain and associated challenge model should be ... (B) SARS-CoV-2 genomic RNA loads in mouse lung homogenates at P0 to P6.

https://t.co/I90OOCJg7o