2/

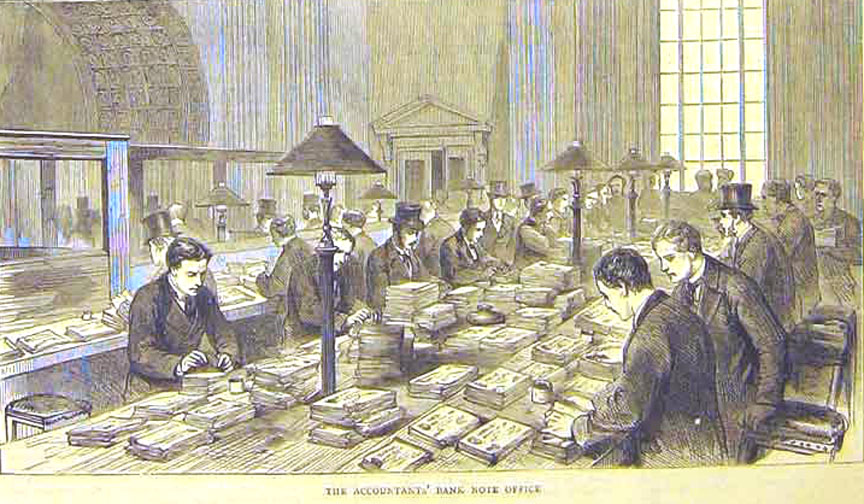

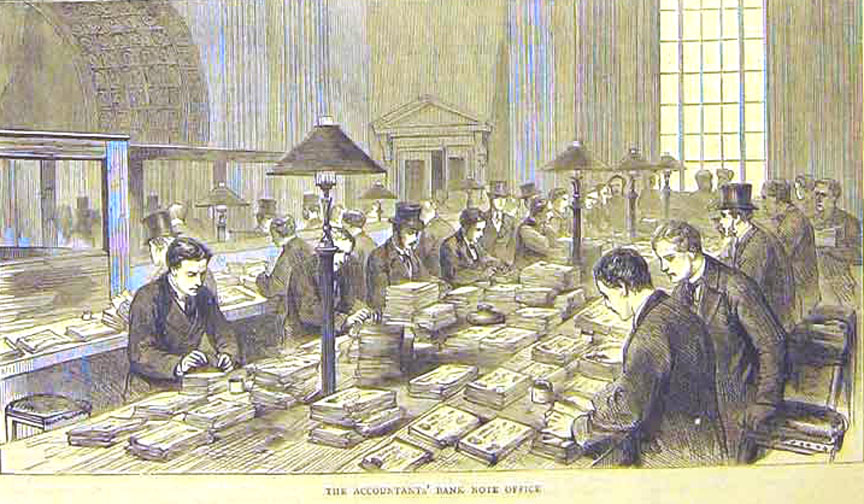

Accountancy is more likely to be mocked than celebrated (or condemned), but accountants, far more than poets, are the unacknowledged legislators of the world.

1/

2/

3/

4/

5/

6/

https://t.co/dApCRKT9yj

7/

https://t.co/5pJBIfYkUN

8/

https://t.co/IdK92zx2sX

https://t.co/lmCAQfTXQv

9/

10/

11/

12/

13/

14/

https://t.co/4TII4dPMMp

15/

16/

17/

https://t.co/hpSWKt1ahr

18/

19/

20/

21/

22/

https://t.co/pmWMTNsPRp

23/

https://t.co/gDyvaKtkwZ

24/

https://t.co/GmcR3tDc8B

25/

26/

27/

28/

https://t.co/alNpNJ8PZw

29/

30/

31/

32/

33/

34/

https://t.co/niVePUyzgf

eof/

More from Cory Doctorow #BLM

Today's Twitter threads (a Twitter thread).

Inside: Planet Money on HP's myriad ripoffs; Strength in numbers; and more!

Archived at: https://t.co/esjoT3u5Gr

#Pluralistic

1/

On Feb 22, I'm delivering a keynote address for the NISO Plus conference, "The day of the comet: what trustbusting means for digital manipulation."

https://t.co/Z84xicXhGg

2/

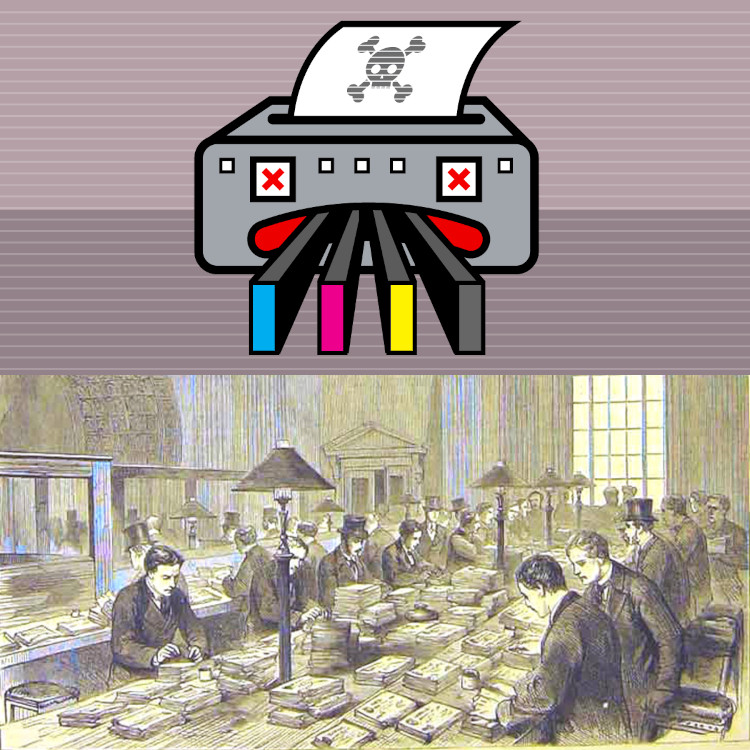

Planet Money on HP's myriad ripoffs: Ink-stained wretches of the world, unite!

https://t.co/k5ASdVUrC2

3/

Strength in numbers: The crisis in accounting.

https://t.co/DjfAfHWpNN

4/

#15yrsago Bad Samaritan family won’t return found expensive camera https://t.co/Rn9E5R1gtV

#10yrsago What does Libyan revolution mean for https://t.co/Jz28qHVhrV? https://t.co/dN1e4MxU4r

5/

Inside: Planet Money on HP's myriad ripoffs; Strength in numbers; and more!

Archived at: https://t.co/esjoT3u5Gr

#Pluralistic

1/

On Feb 22, I'm delivering a keynote address for the NISO Plus conference, "The day of the comet: what trustbusting means for digital manipulation."

https://t.co/Z84xicXhGg

2/

Planet Money on HP's myriad ripoffs: Ink-stained wretches of the world, unite!

https://t.co/k5ASdVUrC2

3/

Back in November, I published an article for @EFF about @HP's latest printer-ink ripoff: after offering its customers a free-ink-for-life plan, it unilaterally switched them all to a $1/month-for-life plan.https://t.co/bsc73xPSuo

— Cory Doctorow #BLM (@doctorow) February 18, 2021

1/ pic.twitter.com/tagduPupA5

Strength in numbers: The crisis in accounting.

https://t.co/DjfAfHWpNN

4/

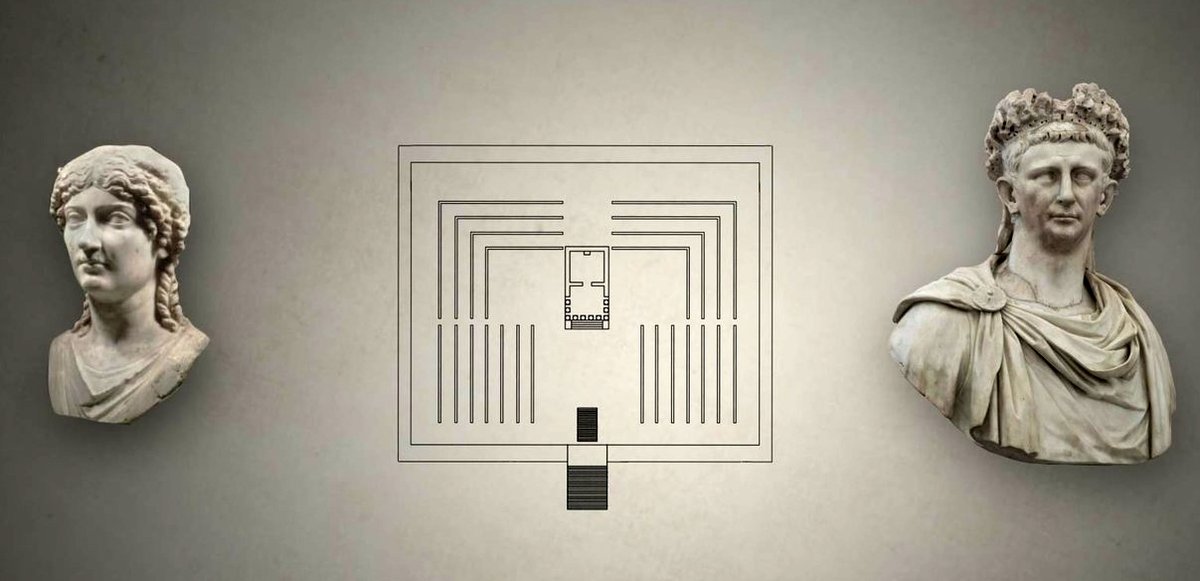

Accountancy is more likely to be mocked than celebrated (or condemned), but accountants, far more than poets, are the unacknowledged legislators of the world.

— Cory Doctorow #BLM (@doctorow) February 18, 2021

1/ pic.twitter.com/FaNQc66gQN

#15yrsago Bad Samaritan family won’t return found expensive camera https://t.co/Rn9E5R1gtV

#10yrsago What does Libyan revolution mean for https://t.co/Jz28qHVhrV? https://t.co/dN1e4MxU4r

5/

More from History

You May Also Like

A brief analysis and comparison of the CSS for Twitter's PWA vs Twitter's legacy desktop website. The difference is dramatic and I'll touch on some reasons why.

Legacy site *downloads* ~630 KB CSS per theme and writing direction.

6,769 rules

9,252 selectors

16.7k declarations

3,370 unique declarations

44 media queries

36 unique colors

50 unique background colors

46 unique font sizes

39 unique z-indices

https://t.co/qyl4Bt1i5x

PWA *incrementally generates* ~30 KB CSS that handles all themes and writing directions.

735 rules

740 selectors

757 declarations

730 unique declarations

0 media queries

11 unique colors

32 unique background colors

15 unique font sizes

7 unique z-indices

https://t.co/w7oNG5KUkJ

The legacy site's CSS is what happens when hundreds of people directly write CSS over many years. Specificity wars, redundancy, a house of cards that can't be fixed. The result is extremely inefficient and error-prone styling that punishes users and developers.

The PWA's CSS is generated on-demand by a JS framework that manages styles and outputs "atomic CSS". The framework can enforce strict constraints and perform optimisations, which is why the CSS is so much smaller and safer. Style conflicts and unbounded CSS growth are avoided.

Legacy site *downloads* ~630 KB CSS per theme and writing direction.

6,769 rules

9,252 selectors

16.7k declarations

3,370 unique declarations

44 media queries

36 unique colors

50 unique background colors

46 unique font sizes

39 unique z-indices

https://t.co/qyl4Bt1i5x

PWA *incrementally generates* ~30 KB CSS that handles all themes and writing directions.

735 rules

740 selectors

757 declarations

730 unique declarations

0 media queries

11 unique colors

32 unique background colors

15 unique font sizes

7 unique z-indices

https://t.co/w7oNG5KUkJ

The legacy site's CSS is what happens when hundreds of people directly write CSS over many years. Specificity wars, redundancy, a house of cards that can't be fixed. The result is extremely inefficient and error-prone styling that punishes users and developers.

The PWA's CSS is generated on-demand by a JS framework that manages styles and outputs "atomic CSS". The framework can enforce strict constraints and perform optimisations, which is why the CSS is so much smaller and safer. Style conflicts and unbounded CSS growth are avoided.