2/

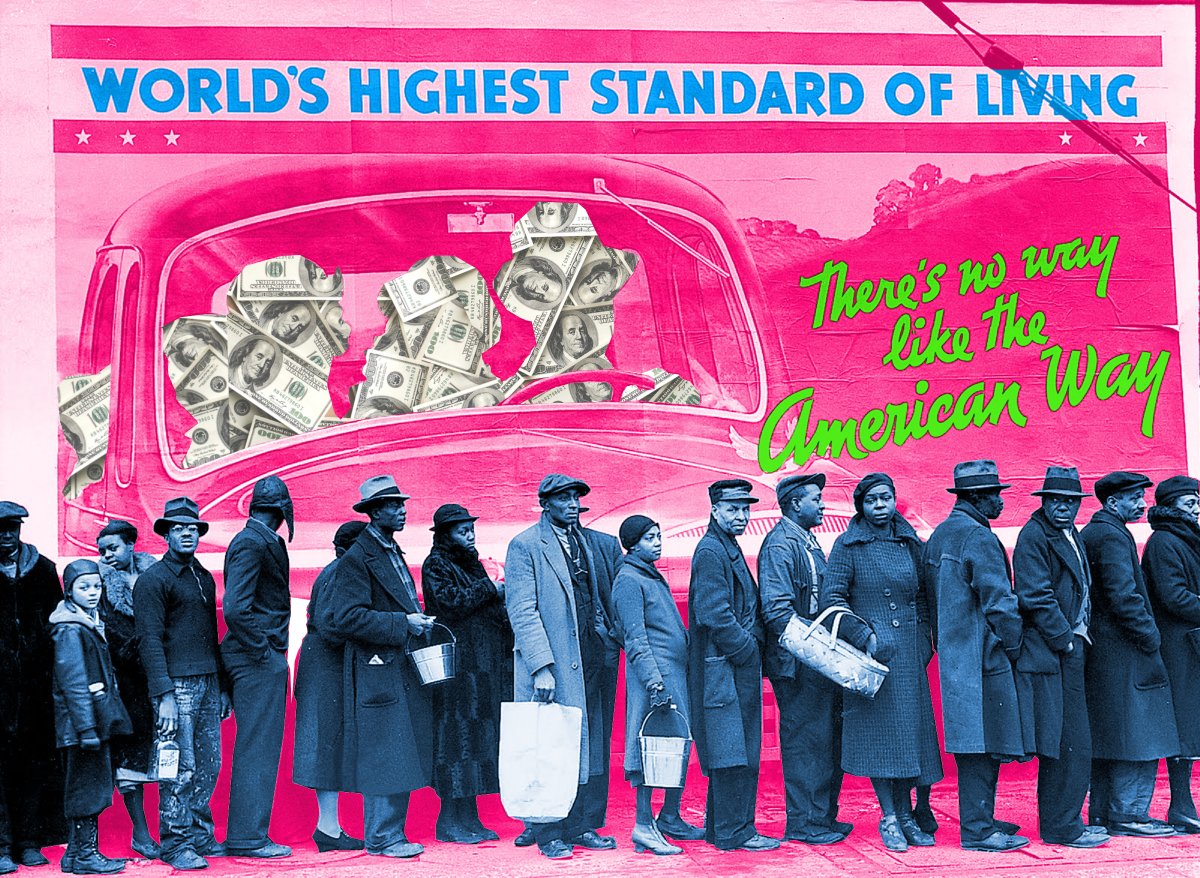

We are in an extraordinary moment, but not an entirely unprecedented one. Since the earliest days, societies have had to cope with disasters that wiped out the ability of everyday people to service their debts and thus threatened to destroy their societies.

1/

2/

https://t.co/6noe3xiiW5

3/

4/

5/

6/

7/

8/

9/

10/

Regulators have unshackled new forms of predatory lending (aka "fintech") with APRs in the hundreds or thousands of percent:

https://t.co/lIrL7kU93L

11/

https://t.co/ULX8hBCO5a

12/

Hudson: "Rising debt overhead serves the business and financial sector by lowering wages while extracting more interest, financial fees, rent and insurance."

13/

14/

But that's no longer possible. We've hit bottom.

15/

16/

17/

18/

19/

20/

21/

22/

More from Cory Doctorow #BLM

Today's Twitter threads (a Twitter thread).

Inside: Stop saying "it's not censorship if it's not the government"; Trump's swamp gators find corporate refuge; and more!

Archived at: https://t.co/7JMcAbaULj

#Pluralistic

1/

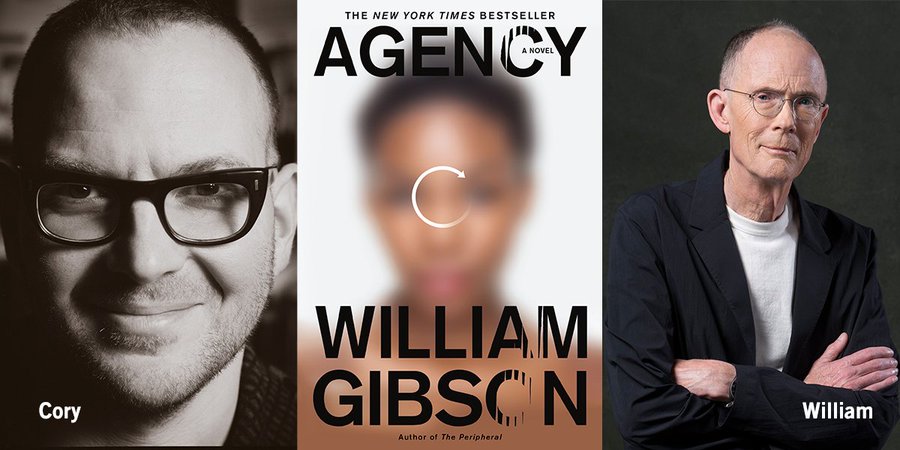

Monday night, I'll be helping William Gibson launch the paperback edition of his novel AGENCY at a Strand Bookstore videoconference. Come say hi!

https://t.co/k3fvBdqOK0

2/

Stop saying "it's not censorship if it's not the government": I didn't expect the Spanish Inquisition.

https://t.co/7I0MpCTez5

3/

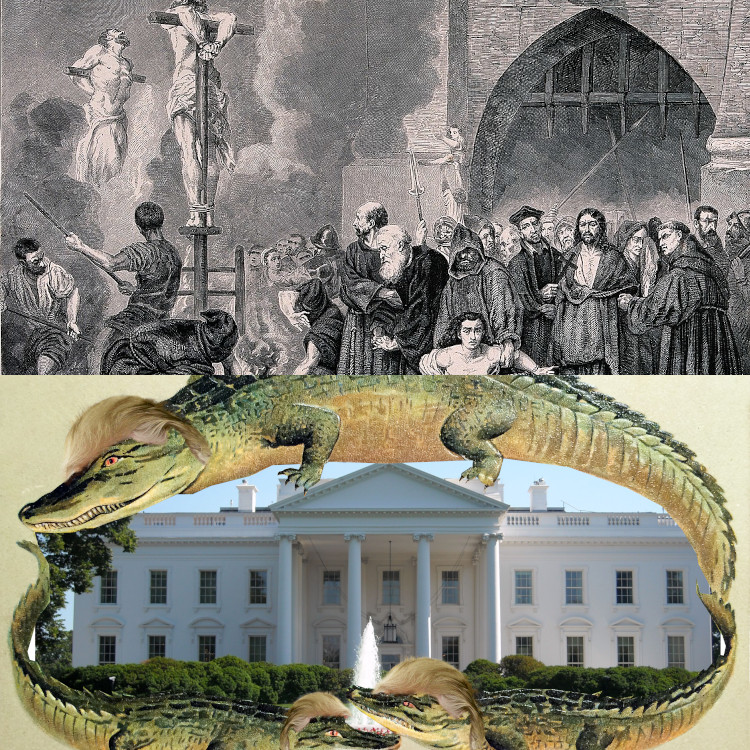

Trump's swamp gators find corporate refuge: The Swamped project.

https://t.co/MUJyIOr2iw

4/

#15yrsago A-Hole bill would make a secret technology into the law of the land https://t.co/57bJaM1Byr

#15yrsago Hollywood’s MP loses the election — hit the road, Sam! https://t.co/12ssYpV46B

#15yrsago How William Gibson discovered science fiction https://t.co/MYR0go37nW

5/

Inside: Stop saying "it's not censorship if it's not the government"; Trump's swamp gators find corporate refuge; and more!

Archived at: https://t.co/7JMcAbaULj

#Pluralistic

1/

Monday night, I'll be helping William Gibson launch the paperback edition of his novel AGENCY at a Strand Bookstore videoconference. Come say hi!

https://t.co/k3fvBdqOK0

2/

Stop saying "it's not censorship if it's not the government": I didn't expect the Spanish Inquisition.

https://t.co/7I0MpCTez5

3/

If you think "It's not censorship unless the government does it," I want to change your mind.

— Cory Doctorow #BLM (@doctorow) January 24, 2021

It's absolutely true that the First Amendment only prohibits government action to suppress speech based on its content, but the First Amendment is not the last word on censorship.

1/ pic.twitter.com/ycbLLDhtrd

Trump's swamp gators find corporate refuge: The Swamped project.

https://t.co/MUJyIOr2iw

4/

Have you seen the stories about how Trump administration officials and staffers for Ted Cruz are finding that no one in the private sector will hire them because they are forever tainted by their former bosses' disgraceful behavior?

— Cory Doctorow #BLM (@doctorow) January 24, 2021

They're bullshit.https://t.co/XvYDPpR9yd

1/ pic.twitter.com/VxisK4d8jV

#15yrsago A-Hole bill would make a secret technology into the law of the land https://t.co/57bJaM1Byr

#15yrsago Hollywood’s MP loses the election — hit the road, Sam! https://t.co/12ssYpV46B

#15yrsago How William Gibson discovered science fiction https://t.co/MYR0go37nW

5/

Today's Twitter threads (a Twitter thread).

Inside: Mashing the Bernie meme; Know Nothings, conspiratorialism and Pastel Q; and more!

Archived at: https://t.co/cKWPSzuYHE

#Pluralistic

1/

Mashing the Bernie meme: What if every video game, except Bernie with mittens?

https://t.co/Zcs71oUras

2/

Inside: Mashing the Bernie meme; Know Nothings, conspiratorialism and Pastel Q; and more!

Archived at: https://t.co/cKWPSzuYHE

#Pluralistic

1/

Mashing the Bernie meme: What if every video game, except Bernie with mittens?

https://t.co/Zcs71oUras

2/

The remix culture of the early 2000s left an indelible impression on me, an enduring delight in the power of whimsy, juxtaposition, virtuosity and ingenuity - and the ability of strangers all over the world to collaborate without any explicit coordination.

— Cory Doctorow #BLM (@doctorow) January 31, 2021

1/ pic.twitter.com/hMKzmoxjLu

You May Also Like

#sculpture #story -

Chandesha-Anugraha Murti - One of the Sculpture in Brihadeshwara Temple at Gangaikonda Cholapuram - built by Raja Rajendra Chola I

This Sculpture depicts Bhagwan Shiva along with Devi Paravathi blessing Chandeshwara - one of the 63 Nayanmars.

#Thread

Chandeshwara/Chandikeshwara is regarded as custodian of Shiva Temple's wealth&most of Shiva temples in South India has separate sannathi for him.

His bhakti for Bhagwan Shiva elevated him as one of foremost among Nayanmars.

He gave importance to Shiva Pooja&protection of cows.

There are series of paintings, illustrating the #story of Chandikeshwar in the premises of

Sri Sathiyagireeswarar #Temple at Seinganur,near Kumbakonam,TN

Chandikeshwara's birth name

is Vichara sarman.He was born in the village of Senganur on the banks of River Manni.

His Parent names were Yajnathatan and Pavithrai.

Vichara Sarman was a gifted child and he learnt Vedas and Agamas at a very young age.

He was very devout and would always think about Bhagwan Shiva.

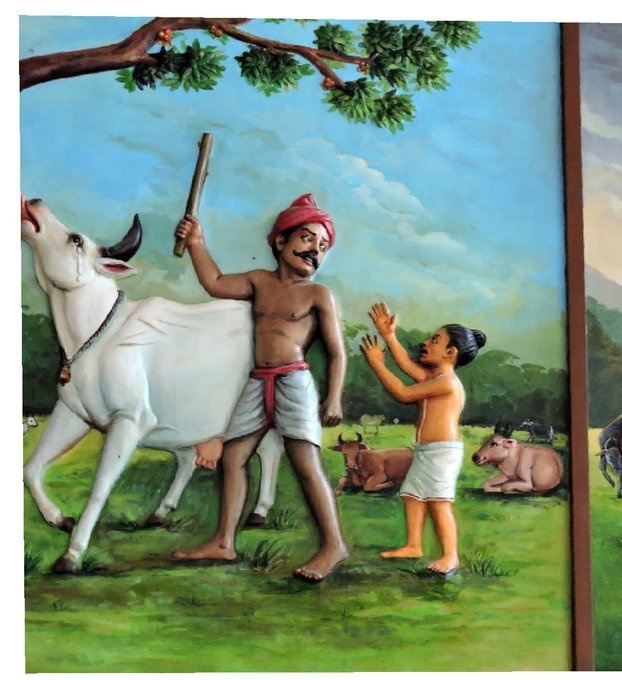

One day he saw a cowherd man brutally assaulting a cow,Vichara Sarman could not tolerate this. He spoke to cowherd: ‘Do you not know that the cow is worshipful & divine? All gods & Devas reside in https://t.co/ElLcI5ppsK it is our duty to protect cows &we should not to harm them.

Chandesha-Anugraha Murti - One of the Sculpture in Brihadeshwara Temple at Gangaikonda Cholapuram - built by Raja Rajendra Chola I

This Sculpture depicts Bhagwan Shiva along with Devi Paravathi blessing Chandeshwara - one of the 63 Nayanmars.

#Thread

Chandeshwara/Chandikeshwara is regarded as custodian of Shiva Temple's wealth&most of Shiva temples in South India has separate sannathi for him.

His bhakti for Bhagwan Shiva elevated him as one of foremost among Nayanmars.

He gave importance to Shiva Pooja&protection of cows.

There are series of paintings, illustrating the #story of Chandikeshwar in the premises of

Sri Sathiyagireeswarar #Temple at Seinganur,near Kumbakonam,TN

Chandikeshwara's birth name

is Vichara sarman.He was born in the village of Senganur on the banks of River Manni.

His Parent names were Yajnathatan and Pavithrai.

Vichara Sarman was a gifted child and he learnt Vedas and Agamas at a very young age.

He was very devout and would always think about Bhagwan Shiva.

One day he saw a cowherd man brutally assaulting a cow,Vichara Sarman could not tolerate this. He spoke to cowherd: ‘Do you not know that the cow is worshipful & divine? All gods & Devas reside in https://t.co/ElLcI5ppsK it is our duty to protect cows &we should not to harm them.