So the cryptocurrency industry has basically two products, one which is relatively benign and doesn't have product market fit, and one which is malignant and does. The industry has a weird superposition of understanding this fact and (strategically?) not understanding it.

If everyone was holding bitcoin on the old x86 in their parents basement, we would be finding a price bottom. The problem is the risk is all pooled at a few brokerages and a network of rotten exchanges with counter party risk that makes AIG circa 2008 look like a good credit.

— Greg Wester (@gwestr) November 25, 2018

More from Patrick McKenzie

I like this heuristic, and have a few which are similar in intent to it:

Hiring efficiency:

How long does it take, measured from initial expression of interest through offer of employment signed, for a typical candidate cold inbounding to the company?

What is the *theoretical minimum* for *any* candidate?

How long does it take, as a developer newly hired at the company:

* To get a fully credentialed machine issued to you

* To get a fully functional development environment on that machine which could push code to production immediately

* To solo ship one material quanta of work

How long does it take, from first idea floated to "It's on the Internet", to create a piece of marketing collateral.

(For bonus points: break down by ambitiousness / form factor.)

How many people have to say yes to do something which is clearly worth doing which costs $5,000 / $15,000 / $250,000 and has never been done before.

Here's how I'd measure the health of any tech company:

— Jeff Atwood (@codinghorror) October 25, 2018

How long, as measured from the inception of idea to the modified software arriving in the user's hands, does it take to roll out a *1 word copy change* in your primary product?

Hiring efficiency:

How long does it take, measured from initial expression of interest through offer of employment signed, for a typical candidate cold inbounding to the company?

What is the *theoretical minimum* for *any* candidate?

How long does it take, as a developer newly hired at the company:

* To get a fully credentialed machine issued to you

* To get a fully functional development environment on that machine which could push code to production immediately

* To solo ship one material quanta of work

How long does it take, from first idea floated to "It's on the Internet", to create a piece of marketing collateral.

(For bonus points: break down by ambitiousness / form factor.)

How many people have to say yes to do something which is clearly worth doing which costs $5,000 / $15,000 / $250,000 and has never been done before.

More from Crypto

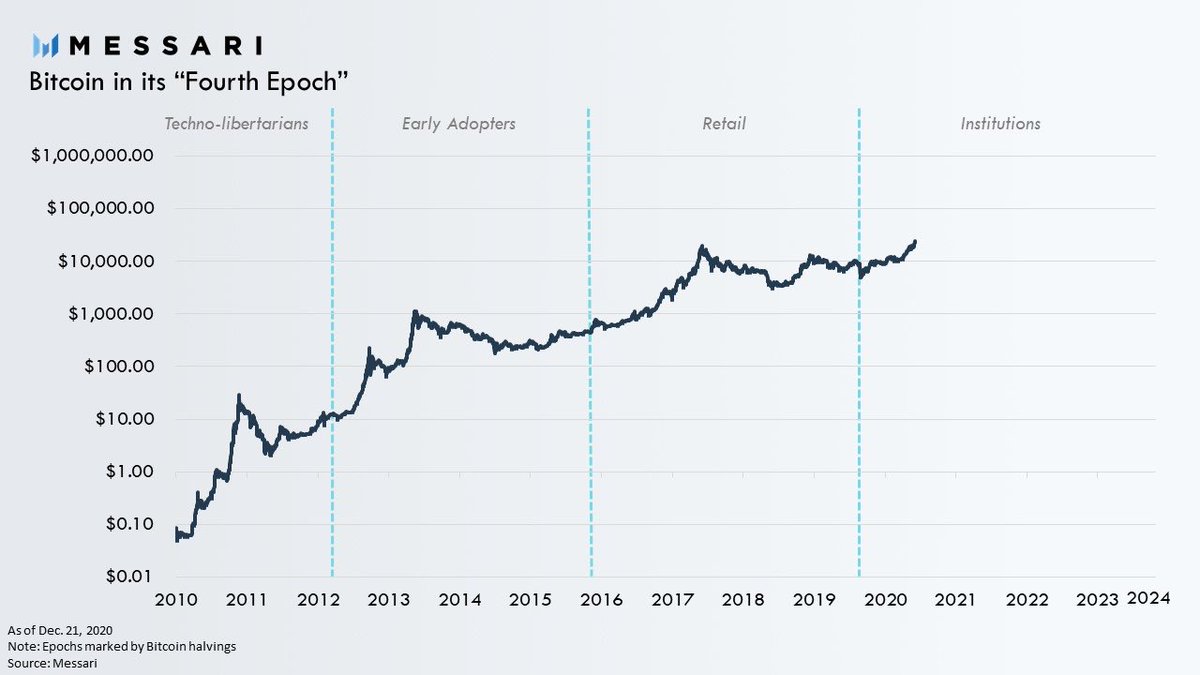

Excited to share our 2020 #Bitcoin review.

2020 will be remembered as the year the long fabled institutions finally arrived and #Bitcoin became a bonafide macroeconomic asset.

Below are the top highlights of each month for Bitcoin’s historic year.

1/

Bitcoin is now at all-time highs capping off an extremely successful year.

But it was by no means stable ride up.

2020 was a historically volatile year.

@YoungCryptoPM and I provided a detailed overview of every month of 2020 in all its

Jan.

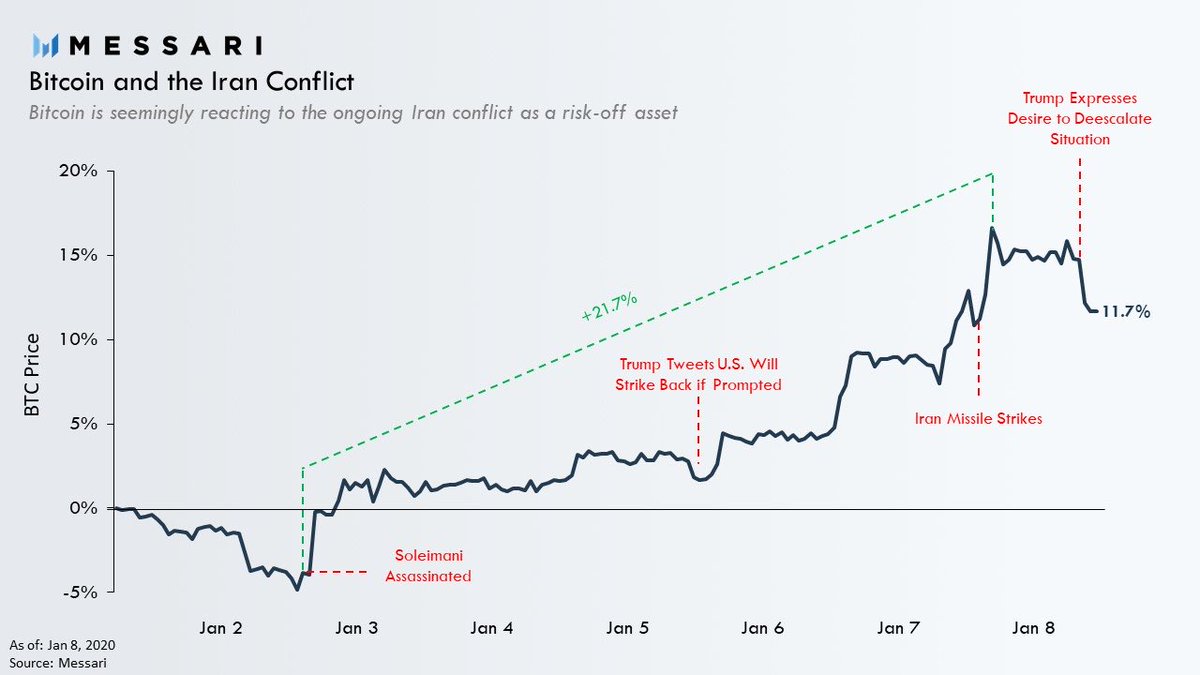

3 days into the new year the US assassinated Iran’s top general Soleimani.

BTC surprisingly reacted to the events behaving like a safe haven as the risk of war increased.

The events provided the first hints of BTC potentially having graduated to a legitimate macro asset.

Feb.

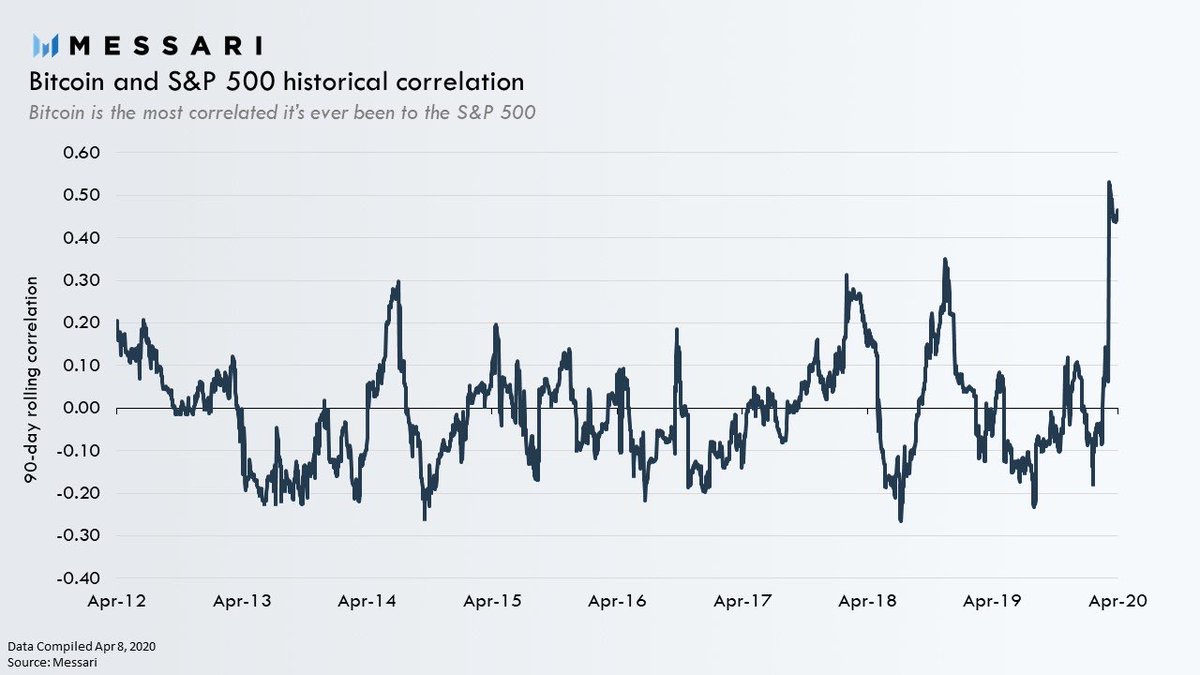

COVID-19 reached a tipping point causing markets to crash.

BTC’s correlation with the S&P 500 reached an ATH in the following weeks.

This is when everyone learned BTC was not a recession hedge, it was a hedge against inflation and loss of confidence in fiat currencies. https://t.co/JB7dJ3qp6M

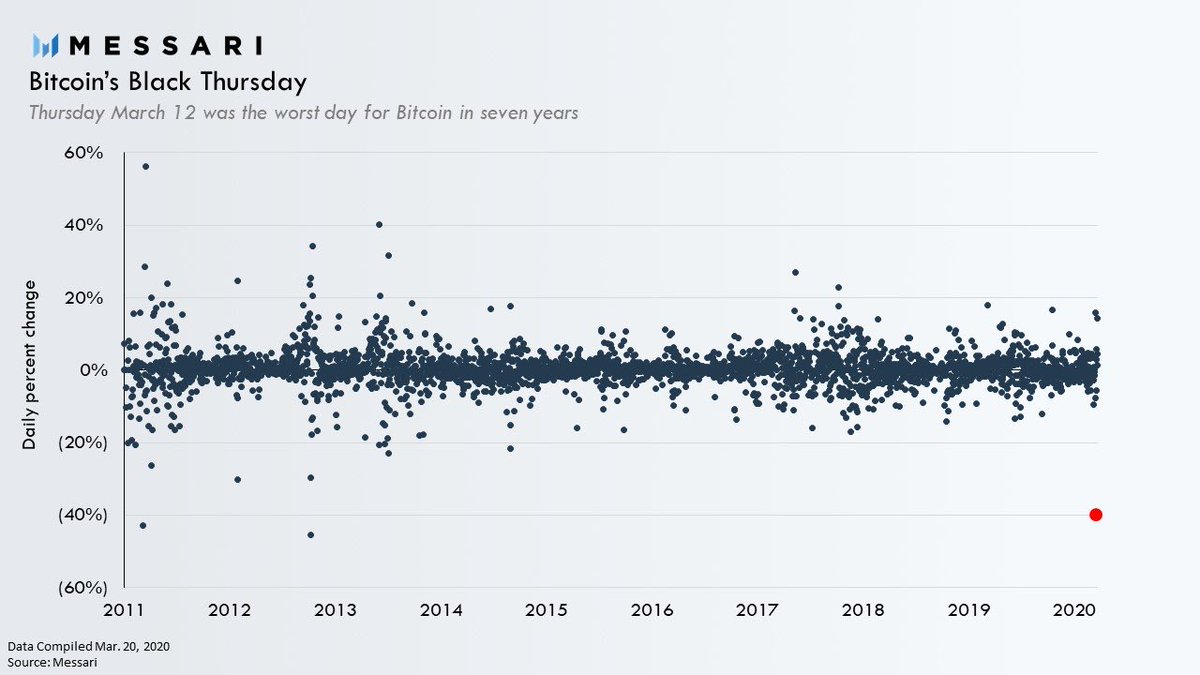

Mar.

Financial markets in free fall.

The liquidity crisis was so severe BTC experienced one of it’s worst days ever.

Now known as Black Thursday, on March 12, BTC plummeted as much as 50% to below $4,000 at its lowest point on the day.

BTC closed the day down 40%

2020 will be remembered as the year the long fabled institutions finally arrived and #Bitcoin became a bonafide macroeconomic asset.

Below are the top highlights of each month for Bitcoin’s historic year.

1/

Bitcoin is now at all-time highs capping off an extremely successful year.

But it was by no means stable ride up.

2020 was a historically volatile year.

@YoungCryptoPM and I provided a detailed overview of every month of 2020 in all its

Jan.

3 days into the new year the US assassinated Iran’s top general Soleimani.

BTC surprisingly reacted to the events behaving like a safe haven as the risk of war increased.

The events provided the first hints of BTC potentially having graduated to a legitimate macro asset.

Feb.

COVID-19 reached a tipping point causing markets to crash.

BTC’s correlation with the S&P 500 reached an ATH in the following weeks.

This is when everyone learned BTC was not a recession hedge, it was a hedge against inflation and loss of confidence in fiat currencies. https://t.co/JB7dJ3qp6M

1/ Figure I should get out ahead of this issue:

— Dan McArdle (@robustus) June 22, 2018

Bitcoin is a hedge against inflation & loss of confidence in fiat, NOT a hedge against a typical recession.

Mar.

Financial markets in free fall.

The liquidity crisis was so severe BTC experienced one of it’s worst days ever.

Now known as Black Thursday, on March 12, BTC plummeted as much as 50% to below $4,000 at its lowest point on the day.

BTC closed the day down 40%

I'm sure someone else has explained this, but it is just so cool and I want to explain how this works.

So Curve is awesome for swaps between similar assets, right? The fact that they trade very close to each other is a key part about how Curve works, using it's custom swap invariant function.

That's step 1

Step 2 is that Synthetix is awesome for creating "synthetic assets" (aka synths) which are assets that trade like other assets, that are backed by another, entirely different asset. Basically, a plastic banana that I can buy and sell like a real banana.

Synthetix has a feature that lets you swap between any two synths with zero slippage and a flat fee. That's because it is simply converting the sythentic asset into another synthetic asset, the backing for the synth doesn't change it just uses a different price oracle now.

This is important. Absolutely no slippage, at any size

Swap $1m sUSD for $1m sBTC? flat 0.3% fee

Swap $10m sUSD for $10m sBTC? flat 0.3% fee

swap $100m sUSD for $100m sBTC? Well, there isn't that many synths in Curve, yet but you get the point. The only limit is the pool depth

— Andre Cronje (@AndreCronjeTech) January 15, 2021

So Curve is awesome for swaps between similar assets, right? The fact that they trade very close to each other is a key part about how Curve works, using it's custom swap invariant function.

That's step 1

Step 2 is that Synthetix is awesome for creating "synthetic assets" (aka synths) which are assets that trade like other assets, that are backed by another, entirely different asset. Basically, a plastic banana that I can buy and sell like a real banana.

Synthetix has a feature that lets you swap between any two synths with zero slippage and a flat fee. That's because it is simply converting the sythentic asset into another synthetic asset, the backing for the synth doesn't change it just uses a different price oracle now.

This is important. Absolutely no slippage, at any size

Swap $1m sUSD for $1m sBTC? flat 0.3% fee

Swap $10m sUSD for $10m sBTC? flat 0.3% fee

swap $100m sUSD for $100m sBTC? Well, there isn't that many synths in Curve, yet but you get the point. The only limit is the pool depth