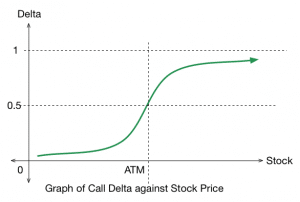

Delta is a measure of the sensitivity of an option’s price changes relative to the changes in the underlying asset’s price. In other words, if the price of the underlying asset increases by 1 points, the price of the option will change by delta amount.

There are various Options Greeks like: Delta, Gamma, Vega, Rho, Theta.

A complete guide on how these #Option Greeks impact option price.

Delta is a measure of the sensitivity of an option’s price changes relative to the changes in the underlying asset’s price. In other words, if the price of the underlying asset increases by 1 points, the price of the option will change by delta amount.

As the options become ITM, the value of delta tends towards +1 for call and -1 for put.

Delta is important greeks to determine the hedge ratio for investors who want to hedge their portfolio.

Gamma (Γ) is a measure of the delta’s change relative to the changes in the price of the underlying asset.

If the price of the underlying asset increases by 1 points, the option’s delta will change by the gamma amount.

Long options (call/put) have positive Gamma.

Think like this, Delta is basically the velocity and gamma is acceleration as taught in the physics.

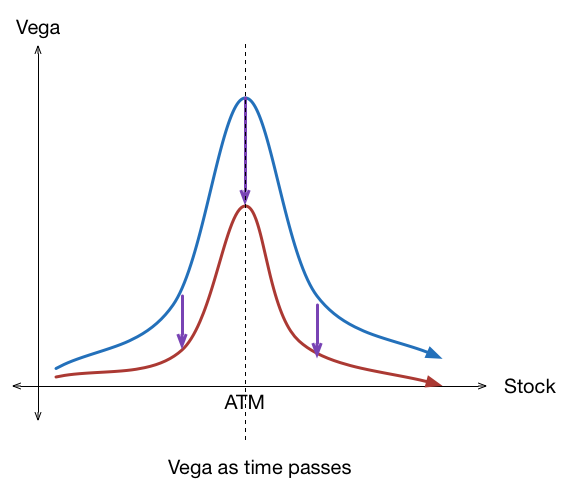

Vega (ν) is an option Greek that measures the sensitivity of an option price relative to the volatility of the underlying asset. If the volatility of the underlying asset increases by 1%, the option price will change by the vega amount.

Rising vega is a friend of option buyers and falling vega is a friend of option sellers.

Rho (ρ) measures the sensitivity of the option price relative to interest rates and it is least significant Option Greeks because option price are less sensitive to interest rate. If an interest rate increases by 1%, the option price will change by the rho amount.

Similarly, if the interest rate decrease, then the value of the call option will fall and the value of the put option will rise.

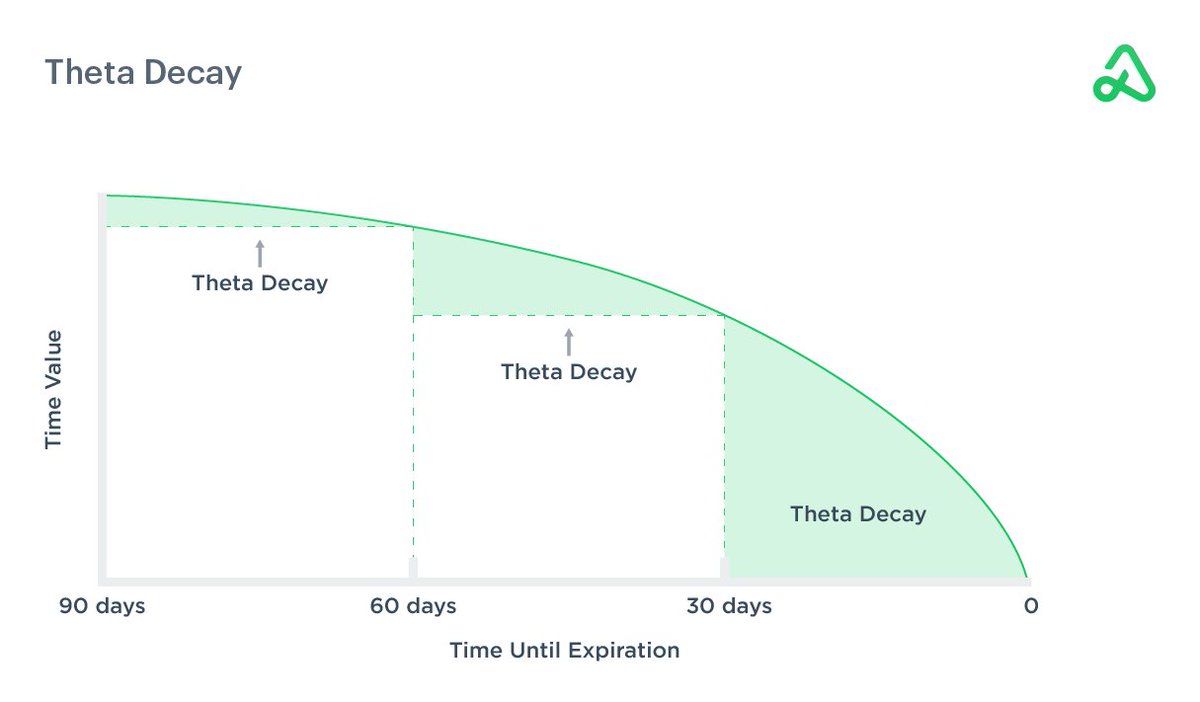

Theta (θ) is a measure of the sensitivity of the option price relative to the option’s time to maturity. If the option’s time to maturity decreases by one day, the option’s price will change by the theta amount.

Also, the value of the option for far expiry will be more than near expiry as it has more time left for expiry.

For me, the most important Greeks are Theta and Vega, as I am an option seller.

If you found this useful, please do RT the first tweet.

Follow @YMehta_ for more such learning related to trading.

https://t.co/K0Osq2Yx8l

There are various Options Greeks like: Delta, Gamma, Vega, Rho, Theta.

— Yash Mehta (@YMehta_) September 4, 2022

A complete guide on how these #Option Greeks impact option price.

More from Yash Mehta

In the early stage, most of the traders & investors use indicators in their analysis.

Here is a master thread of how most of the indicators can be used in trading/investing to increase accuracy for free🧵:

Also, the last indicator and strategy is my favourite of all in trading.

1/ Moving Average is a very common indicator.

This thread is on what are the different ways of using the moving average

2/ RSI is one of the momentum indicator for traders.

In this thread, I have shared different ways of using RSI. Also, an investing strategy is shared, which can help you to pick stocks that can give you good

3/ CCI is another amazing indicator that is used by momentum traders.

Shared few strategies with CCI which a trader and investor both can

4/ CPR is one of the most popular indicator in the trading community.

This thread covers everything about the CPR indicator and how to use this indicator in

Here is a master thread of how most of the indicators can be used in trading/investing to increase accuracy for free🧵:

Also, the last indicator and strategy is my favourite of all in trading.

1/ Moving Average is a very common indicator.

This thread is on what are the different ways of using the moving average

Moving Averages is a common indicator which most of us (novice/professional) use in the stock market for trading and investment.

— Yash Mehta (@YMehta_) October 11, 2021

This learning thread would be on

"\U0001d650\U0001d668\U0001d65a\U0001d668 \U0001d664\U0001d65b \U0001d648\U0001d664\U0001d66b\U0001d65e\U0001d663\U0001d65c \U0001d63c\U0001d66b\U0001d65a\U0001d667\U0001d656\U0001d65c\U0001d65a"

Like\U0001f44d & Retweet\U0001f504 for wider reach and more such learning thread.

1/10

2/ RSI is one of the momentum indicator for traders.

In this thread, I have shared different ways of using RSI. Also, an investing strategy is shared, which can help you to pick stocks that can give you good

#RSI is a common indicator which most of us use in the stock market.

— Yash Mehta (@YMehta_) October 22, 2021

This learning thread would be on

"\U0001d650\U0001d668\U0001d65a\U0001d668 \U0001d664\U0001d65b \U0001d64d\U0001d64e\U0001d644"

Like\U0001f44d & Retweet\U0001f504 for wider reach and for more such learning thread in the future.

Also, an investment strategy is shared using RSI in the end.

1/16

3/ CCI is another amazing indicator that is used by momentum traders.

Shared few strategies with CCI which a trader and investor both can

#CCI is an indicator which is used in the #stockmarket

— Yash Mehta (@YMehta_) February 26, 2022

This learning thread would be on

"\U0001d650\U0001d668\U0001d65a\U0001d668 \U0001d664\U0001d65b \U0001d63e\U0001d63e\U0001d644"

Also, an investment strategy and trading strategy is shared

If you appreciate this, a Like & Retweet will go a long way in maximizing the reach of this tweet\u2665\ufe0f

1/19

4/ CPR is one of the most popular indicator in the trading community.

This thread covers everything about the CPR indicator and how to use this indicator in

#CPR is an indicator which is used for #Intraday in Stock Market.

— Yash Mehta (@YMehta_) November 19, 2021

This learning thread would be on

"\U0001d650\U0001d668\U0001d65a\U0001d668 \U0001d664\U0001d65b \U0001d63e\U0001d64b\U0001d64d"

Like\u2764\ufe0f& Retweet\U0001f501for wider reach and for more such learning thread in the future.

Also, an investment strategy is shared using CPR in the end.

1/24

Stock Screeners is an integral part of doing homework post market hours.

Most of us use screeners to filter buzzing stocks out of 1000+ stock and it saves lot of times.

Here is the list of top screeners:

Also, last screener is one of my favourite to pick early momentum stocks.

1/ Volume Buzzer:

This can be used on daily time frame and it identifies all the stocks where volume action was very

2/ Bullish Divergence:

This screener will help you find all the stocks that has given bullish divergence. Traders who like to trade reversal stocks that are in downtrend can use this screener. This can be used at the end of the

3/ Bearish Divergence:

This screener will help you find all the stocks that has given bearish divergence. Traders who like to trade reversal stocks that are in uptrend can use this screener. This can be used at the end of the

4/ Nimblr F2F:

This screener was designed from @Deishma F2F video:

https://t.co/apaQYVbAlq

This screener helps in identifying momentum and indecisive candles on daily time

Most of us use screeners to filter buzzing stocks out of 1000+ stock and it saves lot of times.

Here is the list of top screeners:

Also, last screener is one of my favourite to pick early momentum stocks.

1/ Volume Buzzer:

This can be used on daily time frame and it identifies all the stocks where volume action was very

2/ Bullish Divergence:

This screener will help you find all the stocks that has given bullish divergence. Traders who like to trade reversal stocks that are in downtrend can use this screener. This can be used at the end of the

3/ Bearish Divergence:

This screener will help you find all the stocks that has given bearish divergence. Traders who like to trade reversal stocks that are in uptrend can use this screener. This can be used at the end of the

4/ Nimblr F2F:

This screener was designed from @Deishma F2F video:

https://t.co/apaQYVbAlq

This screener helps in identifying momentum and indecisive candles on daily time