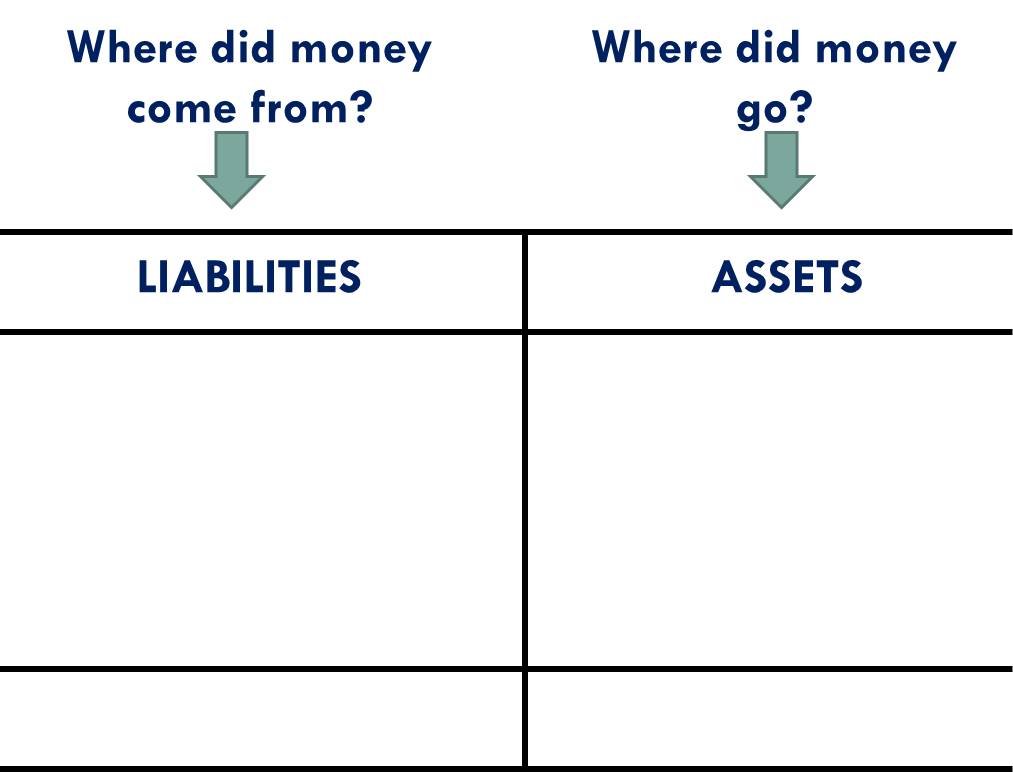

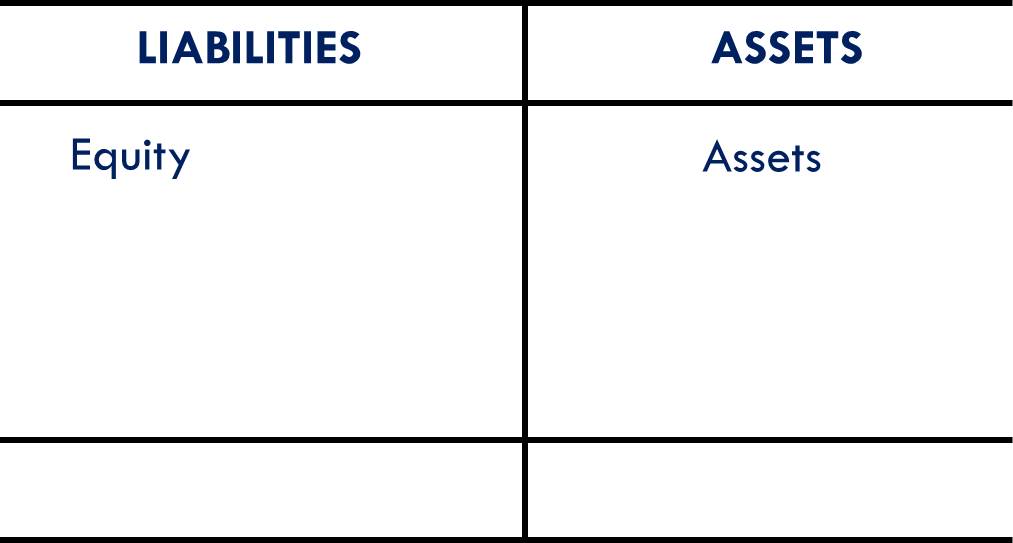

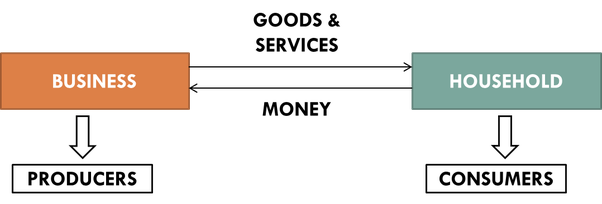

Let us first understand how to interpret a Balance Sheet. (2/n)

While learning accountancy a student is taught to

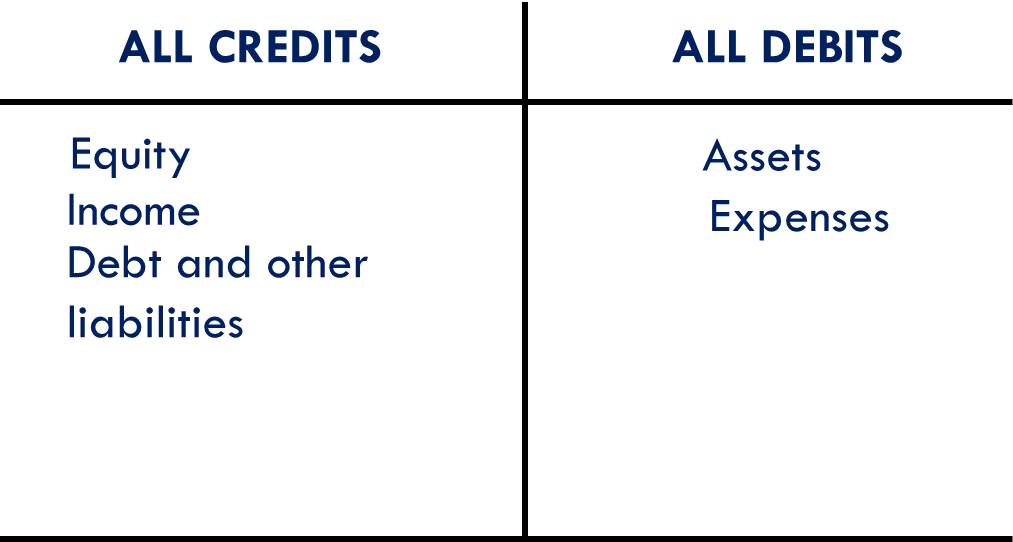

👉Debit all expenses, credit all income.

👉Debit all assets, credit all liabilities.

👉Debit the receiver, credit the giver.

Why is it so?

Let us find out the rationale behind three golden rules of accounts. 👇🧵 (1/n)

Let us first understand how to interpret a Balance Sheet. (2/n)

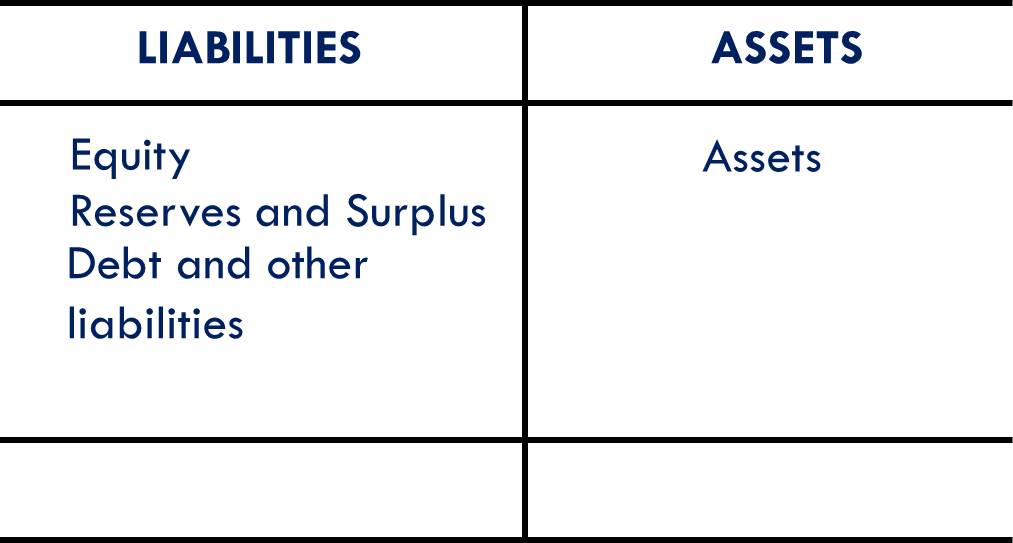

Example: The customer from whom the amount was receivable (Debtor) will get converted into Cash the moment he pays money. (4/n)

Also, the businessman decides to take loan (Outsider’s money) to expand his business. So, the Balance Sheet will look something like this, (6/n)

Profit is calculated as ‘Income – Expenses’.

So, we now have,

Equity + Income – Expenses + Other liabilities = Assets

(8/n)

Equity + Income + Other liabilities = Assets + Expenses

This is a beautiful equation.

LHS shows us all the sources of money and RHS shows us its application. (9/n)

👉Debit all expenses, credit all income.

👉Debit all assets, credit all liabilities.

👉Debit the receiver, credit the giver. (11/n)

Tagging @FincademyIn, @FI_InvestIndia, @abhiandniyu, @VidyaG88 for better reach 🙏

More from swapnilkabra

You May Also Like

Tip from the Monkey

Pangolins, September 2019 and PLA are the key to this mystery

Stay Tuned!

1. Yang

2. A jacobin capuchin dangling a flagellin pangolin on a javelin while playing a mandolin and strangling a mannequin on a paladin's palanquin, said Saladin

More to come tomorrow!

3. Yigang Tong

https://t.co/CYtqYorhzH

Archived: https://t.co/ncz5ruwE2W

4. YT Interview

Some bats & pangolins carry viruses related with SARS-CoV-2, found in SE Asia and in Yunnan, & the pangolins carrying SARS-CoV-2 related viruses were smuggled from SE Asia, so there is a possibility that SARS-CoV-2 were coming from

Pangolins, September 2019 and PLA are the key to this mystery

Stay Tuned!

1. Yang

Meet Yang Ruifu, CCP's biological weapons expert https://t.co/JjB9TLEO95 via @Gnews202064

— Billy Bostickson \U0001f3f4\U0001f441&\U0001f441 \U0001f193 (@BillyBostickson) October 11, 2020

Interesting expose of China's top bioweapons expert who oversaw fake pangolin research

Paper 1: https://t.co/TrXESKLYmJ

Paper 2:https://t.co/9LSJTNCn3l

Pangolinhttps://t.co/2FUAzWyOcv pic.twitter.com/I2QMXgnkBJ

2. A jacobin capuchin dangling a flagellin pangolin on a javelin while playing a mandolin and strangling a mannequin on a paladin's palanquin, said Saladin

More to come tomorrow!

3. Yigang Tong

https://t.co/CYtqYorhzH

Archived: https://t.co/ncz5ruwE2W

4. YT Interview

Some bats & pangolins carry viruses related with SARS-CoV-2, found in SE Asia and in Yunnan, & the pangolins carrying SARS-CoV-2 related viruses were smuggled from SE Asia, so there is a possibility that SARS-CoV-2 were coming from