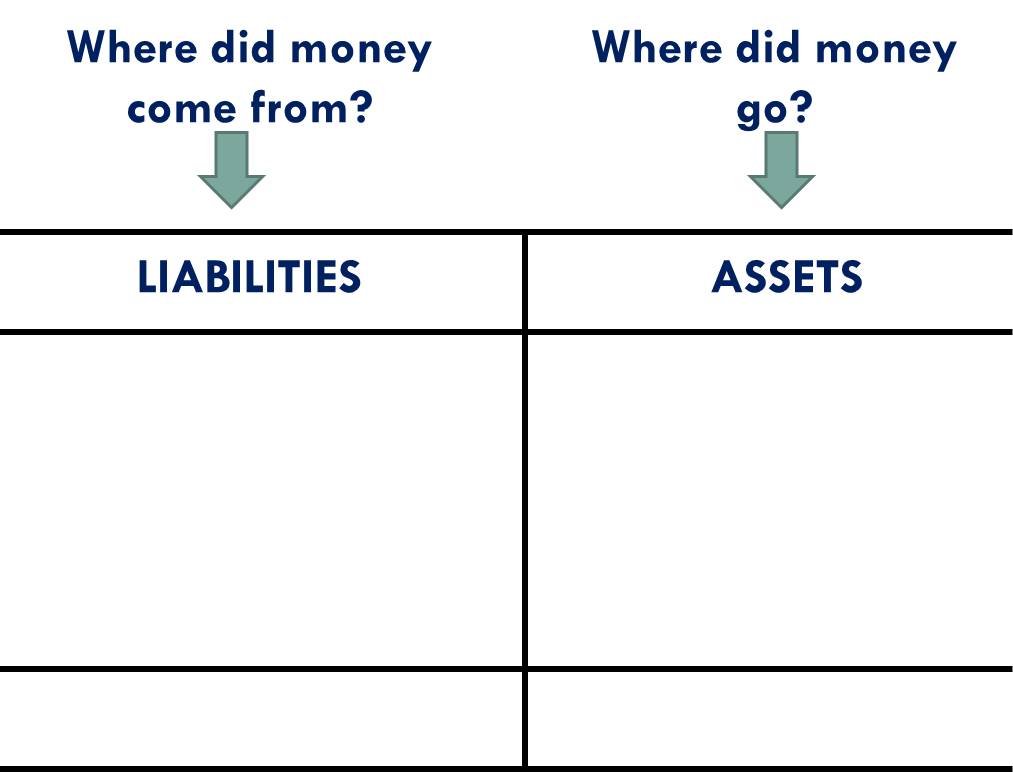

Let us first understand how to interpret a Balance Sheet. (2/n)

While learning accountancy a student is taught to

👉Debit all expenses, credit all income.

👉Debit all assets, credit all liabilities.

👉Debit the receiver, credit the giver.

Why is it so?

Let us find out the rationale behind three golden rules of accounts. 👇🧵 (1/n)

Let us first understand how to interpret a Balance Sheet. (2/n)

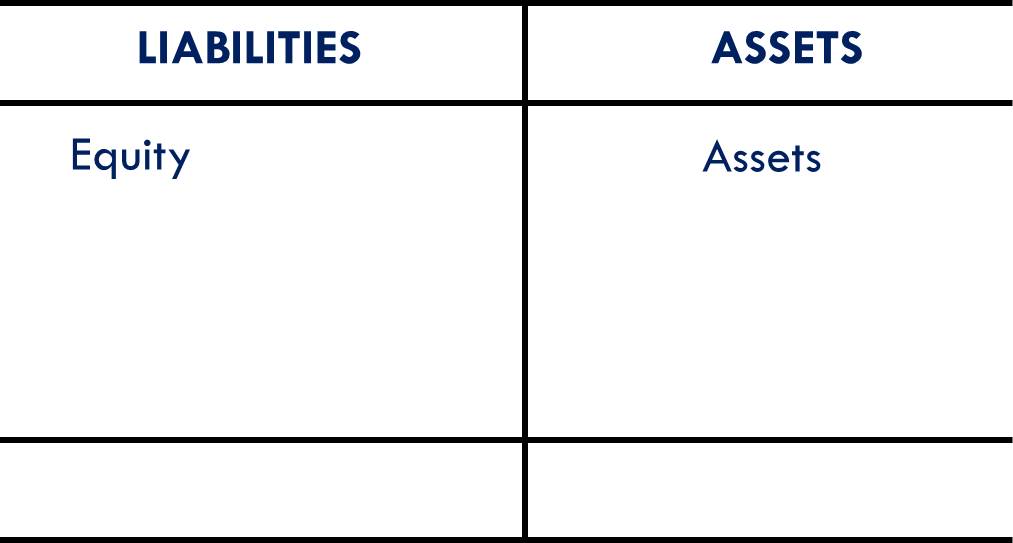

Example: The customer from whom the amount was receivable (Debtor) will get converted into Cash the moment he pays money. (4/n)

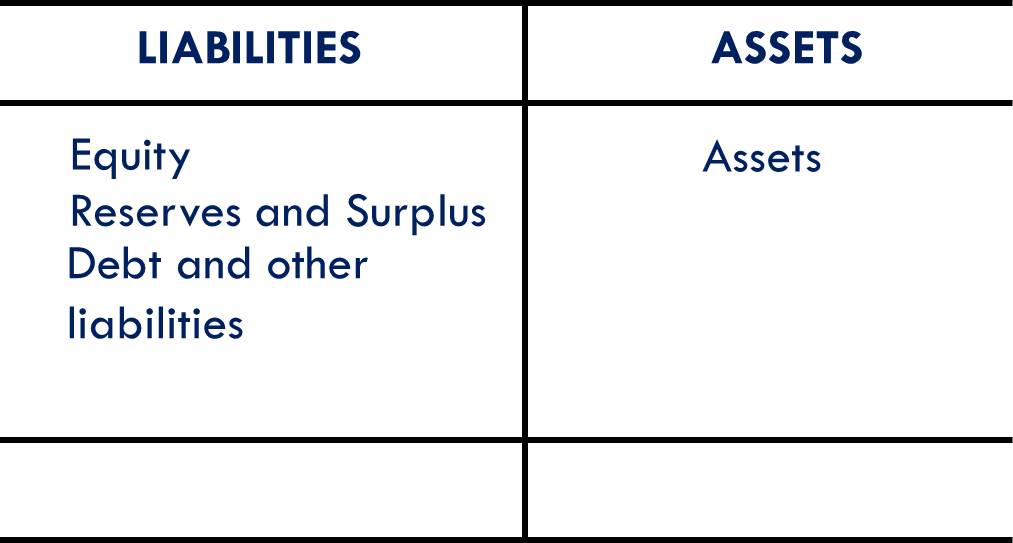

Also, the businessman decides to take loan (Outsider’s money) to expand his business. So, the Balance Sheet will look something like this, (6/n)

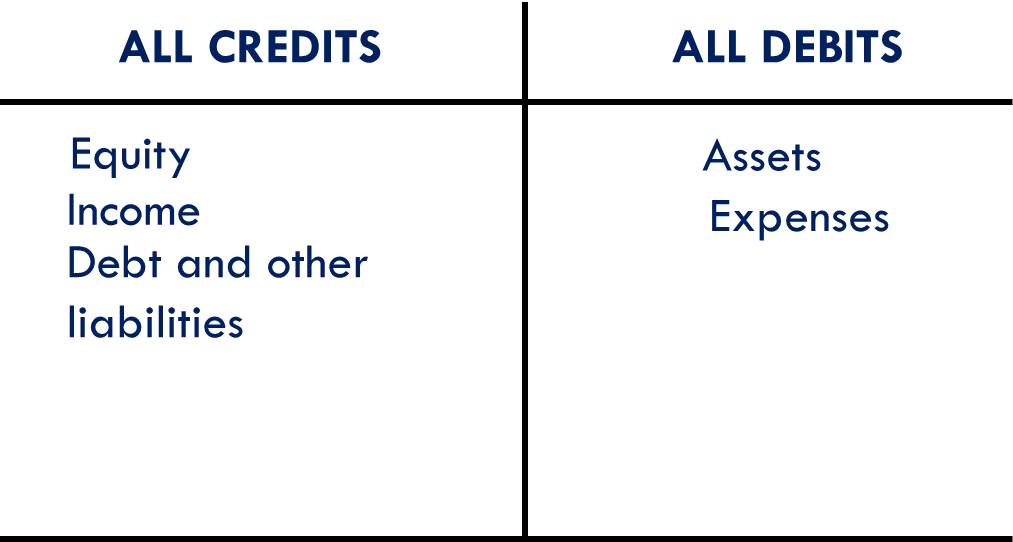

Profit is calculated as ‘Income – Expenses’.

So, we now have,

Equity + Income – Expenses + Other liabilities = Assets

(8/n)

Equity + Income + Other liabilities = Assets + Expenses

This is a beautiful equation.

LHS shows us all the sources of money and RHS shows us its application. (9/n)

👉Debit all expenses, credit all income.

👉Debit all assets, credit all liabilities.

👉Debit the receiver, credit the giver. (11/n)

Tagging @FincademyIn, @FI_InvestIndia, @abhiandniyu, @VidyaG88 for better reach 🙏

More from swapnilkabra

You May Also Like

1/Politics thread time.

To me, the most important aspect of the 2018 midterms wasn't even about partisan control, but about democracy and voting rights. That's the real battle.

2/The good news: It's now an issue that everyone's talking about, and that everyone cares about.

3/More good news: Florida's proposition to give felons voting rights won. But it didn't just win - it won with substantial support from Republican voters.

That suggests there is still SOME grassroots support for democracy that transcends

4/Yet more good news: Michigan made it easier to vote. Again, by plebiscite, showing broad support for voting rights as an

5/OK, now the bad news.

We seem to have accepted electoral dysfunction in Florida as a permanent thing. The 2000 election has never really

To me, the most important aspect of the 2018 midterms wasn't even about partisan control, but about democracy and voting rights. That's the real battle.

2/The good news: It's now an issue that everyone's talking about, and that everyone cares about.

3/More good news: Florida's proposition to give felons voting rights won. But it didn't just win - it won with substantial support from Republican voters.

That suggests there is still SOME grassroots support for democracy that transcends

4/Yet more good news: Michigan made it easier to vote. Again, by plebiscite, showing broad support for voting rights as an

5/OK, now the bad news.

We seem to have accepted electoral dysfunction in Florida as a permanent thing. The 2000 election has never really

Bad ballot design led to a lot of undervotes for Bill Nelson in Broward Co., possibly even enough to cost him his Senate seat. They do appear to be real undervotes, though, instead of tabulation errors. He doesn't really seem to have a path to victory. https://t.co/utUhY2KTaR

— Nate Silver (@NateSilver538) November 16, 2018