First, what is this number and where does it come from?

This number fluctuates daily, and shows up on Starbucks balance sheet as a Deferred Revenue liability.

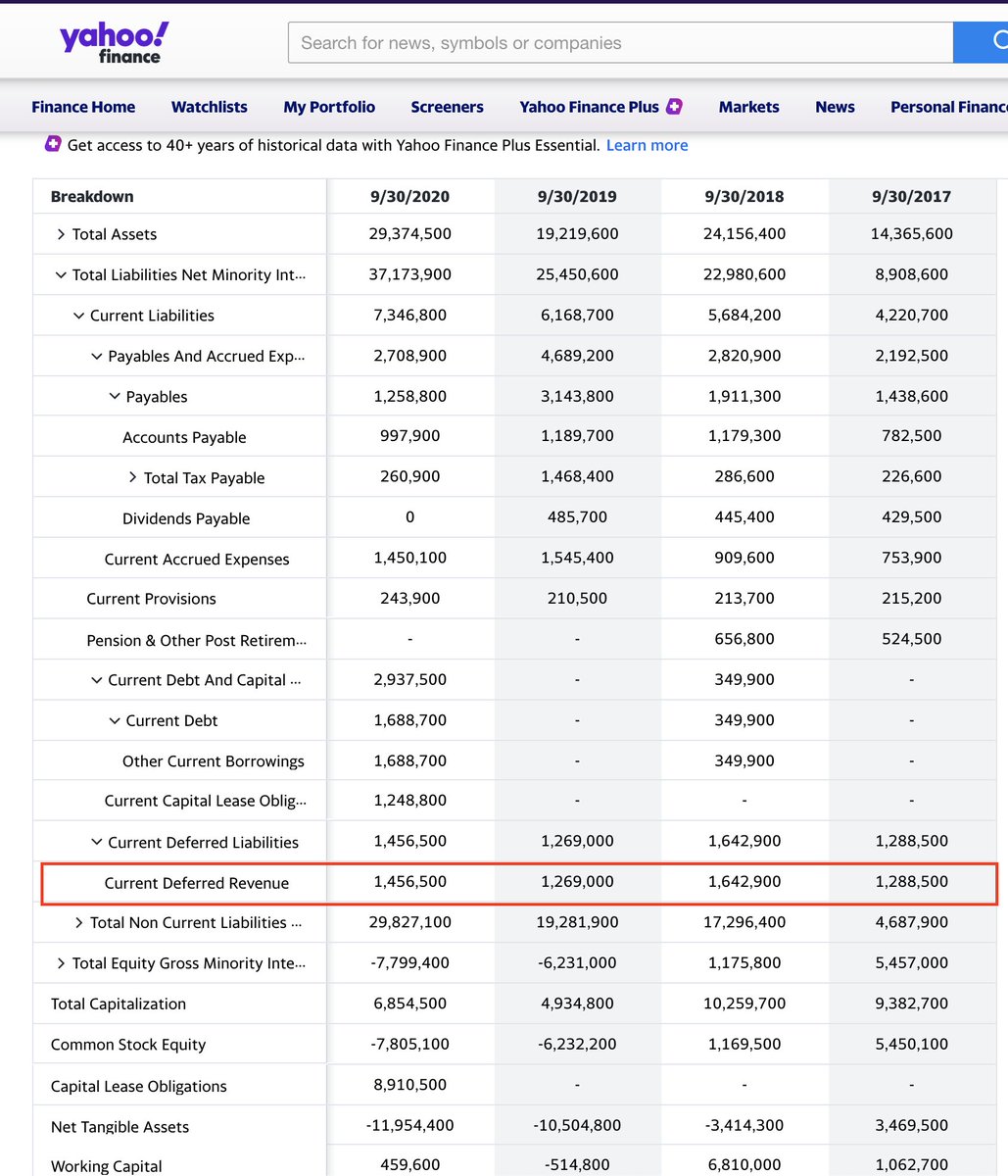

Here are the actual balances the last 4 years:

2020: $1,288,500

2019: $1,642,900

2018: $1,269,000

2017: $1,456,500

This Deferred Revenue number includes 2 things:

- Unused Gift cards

- Unused app deposits

Everyone is familiar with gift cards, but the majority of this # is a relatively fluid flow of deposits/spending through their mobile app.

Deposit, spend, repeat.

In other industries like insurance, this is called "Float". Profit aside, the providers are touching a huge amount of cash as they collect premiums and occasionally cut a claim check.

Same w/ the balances lingering in your Venmo.

You get free transfers, they touch billions.

In addition to providing a huge float, spending on the app and cards are responsible for 40%+ of their rev.

Far and away the biggest retail loyalty program on the planet it is 3x the size of the next biggest.

GameStop and AMC, prior to being meme stocks, are the runners up. LOL

The scale and success of Starbucks loyalty programs is an ode to the convenience and customer experience they deliver to millions.

My original tweet about this had some negative reactions - they're misplaced.

There’s also nothing for bitcoin to solve here!

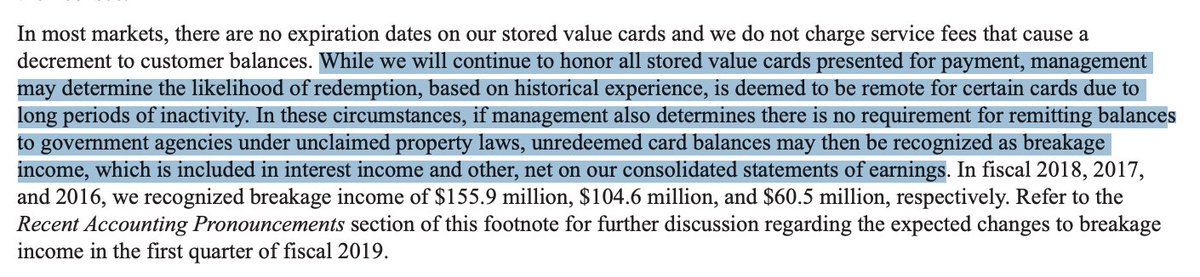

Anyway, the gift card industry is built on the fact that a shockingly high percentage of gift cards are never redeemed.

It's called "breakage" and the rates vary drastically by brand and industry, but are always noticeable.

Yearly, Starbucks claims roughly 10% of that Deferred Revenue number as good old fashion Revenue.

That means historically 10% of it is never used, and it can't just sit around on the books forever.

Even though the aggregate is written off as breakage, the balances never expire.

The best part of all this is that this massive cash float and resulting free revenue is just a byproduct of providing value to consumers at a massive scale.

The data and loyalty they reap from these programs is orders of magnitude more valuable than those side effects.

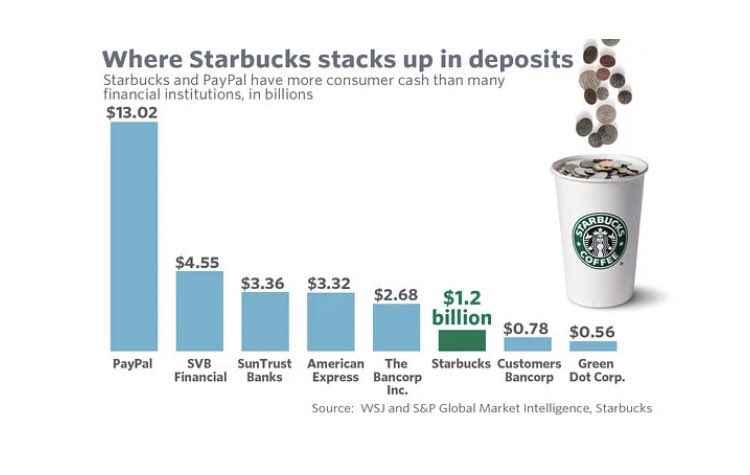

So, how does Starbucks stack up against other banks?

1 - They hold the 6th most consumer cash at any given time

2 - The coffee isn't free

(Get it this is a joke that they’re a bank)

Since they are a public company all this info is available in their financials:

https://t.co/RKs599GR5b And with more context from management in their yearly 10Ks:

https://t.co/2DNni8e4Lx

If you're new here, I tweet about building businesses and cannabis consumer goods. My wife rarely likes any of my tweets but lots of other people do.

Smash that follow

@landforce And sub here to get an email anytime I drop a thread:

https://t.co/NQSnRENCrV

TL;DR

40% of Starbucks revenue is through their app/cards

That creates $1B+ of float at any given time

10% of it is never used by consumers

Side effect of providing massive value