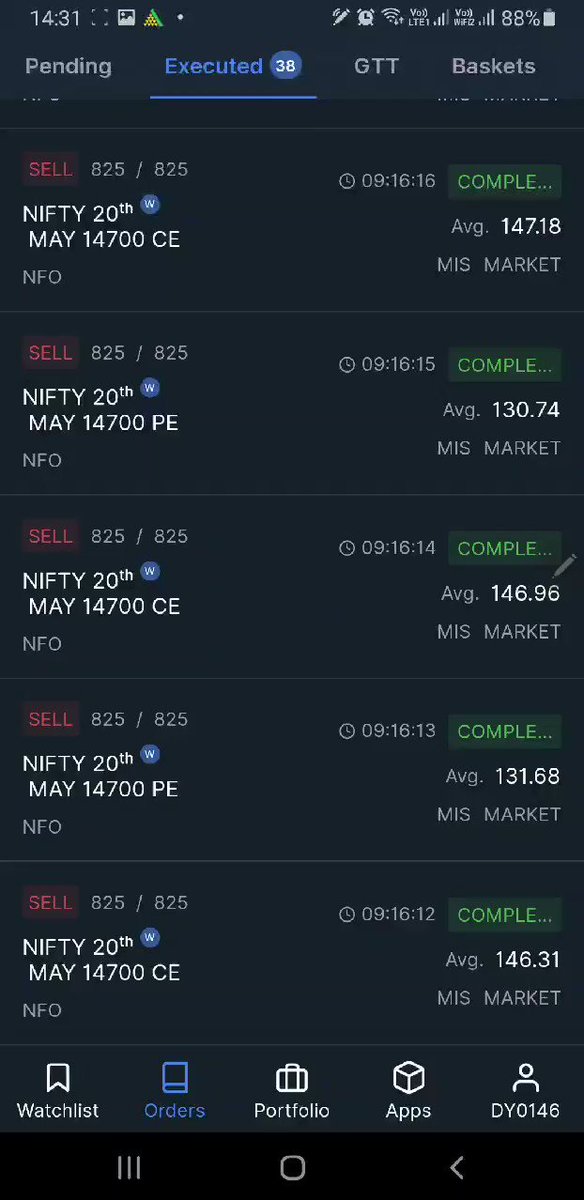

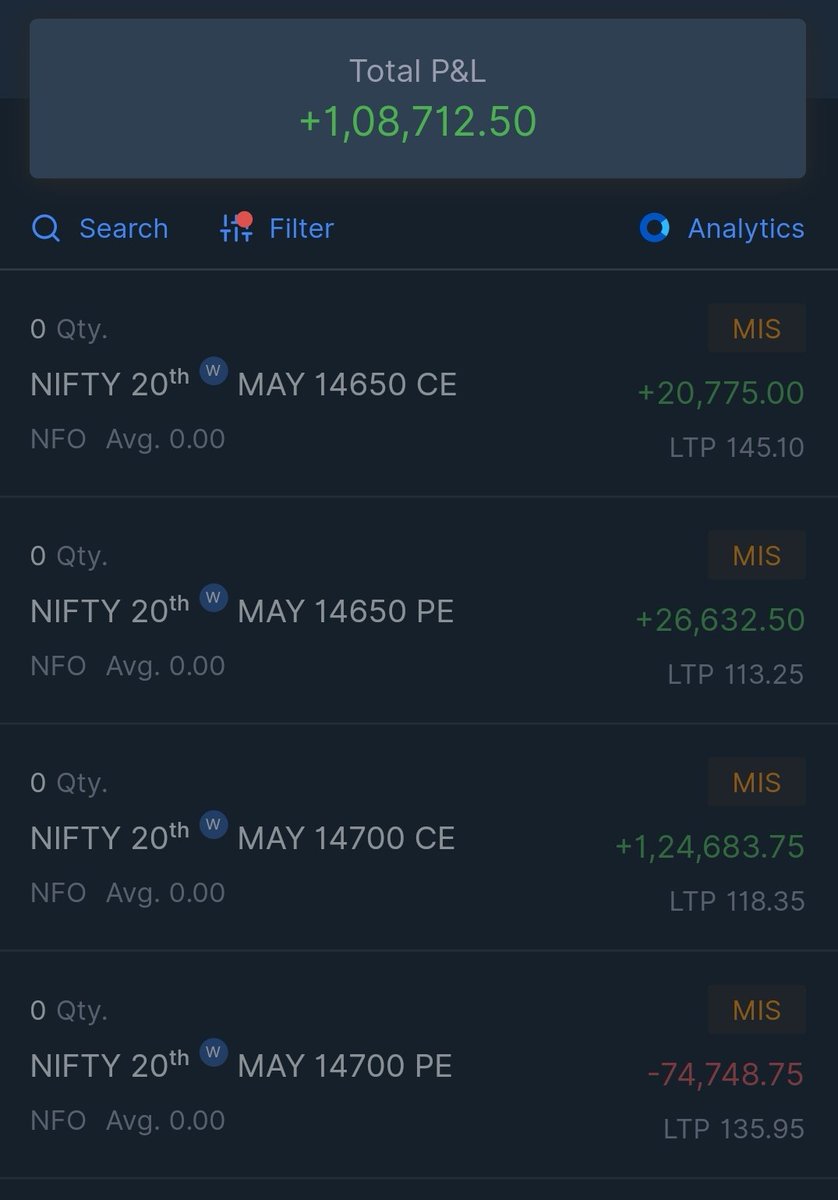

Another Good Friday. Got good decay.

Got 1 lakh.

Traded quantity 4500

1. Entered 14700 short straddle and got 50k.

2. Moved to 14650 short straddle and got 46k.

3. One error trade in execution gave 11k. Exited it immediately.

Closed all positons before 2:30 as premiums are low.

More from yashstocks

(1/4)

12 to 15% is easily achievable nowadays without taking much risk even though the capital is 10 crores due to leverage :)

Invest 10 crore in liquid, debt, gilt, T-bills, 10-20% equity that will give 6 to 7% average returns every year.

(2/4)

Rest can be made by selling far otm penny options only on expiries. They are trading at good premiums due to leverage and can be easily manageable if goes wrong. Thus targeting only 0.15% returns in a week

0.15% x 52 weeks = 7.8%

6% in MFs + 7.8% in trading = 14% returns

(3/4)

Now comes the hard part, doing this every week without getting bored and without affecting one's psychology is the most difficult part. And since we start making money, we take higher risks which can eventually wipe out profits.

(4/4)

And those who think about blackswan event all the time can do it only call side. And it's purely intraday & only will be done on expiry days, so chance of Black Swan, that too on upper side is mostly impossible. If there is any case as such before, do let know in comments

12 to 15% is easily achievable nowadays without taking much risk even though the capital is 10 crores due to leverage :)

Invest 10 crore in liquid, debt, gilt, T-bills, 10-20% equity that will give 6 to 7% average returns every year.

What kind of % return in a year is considered very best with capital more than 10 cr?

— Mitesh Patel (@Mitesh_Engr) October 12, 2021

(2/4)

Rest can be made by selling far otm penny options only on expiries. They are trading at good premiums due to leverage and can be easily manageable if goes wrong. Thus targeting only 0.15% returns in a week

0.15% x 52 weeks = 7.8%

6% in MFs + 7.8% in trading = 14% returns

(3/4)

Now comes the hard part, doing this every week without getting bored and without affecting one's psychology is the most difficult part. And since we start making money, we take higher risks which can eventually wipe out profits.

(4/4)

And those who think about blackswan event all the time can do it only call side. And it's purely intraday & only will be done on expiry days, so chance of Black Swan, that too on upper side is mostly impossible. If there is any case as such before, do let know in comments

1/5

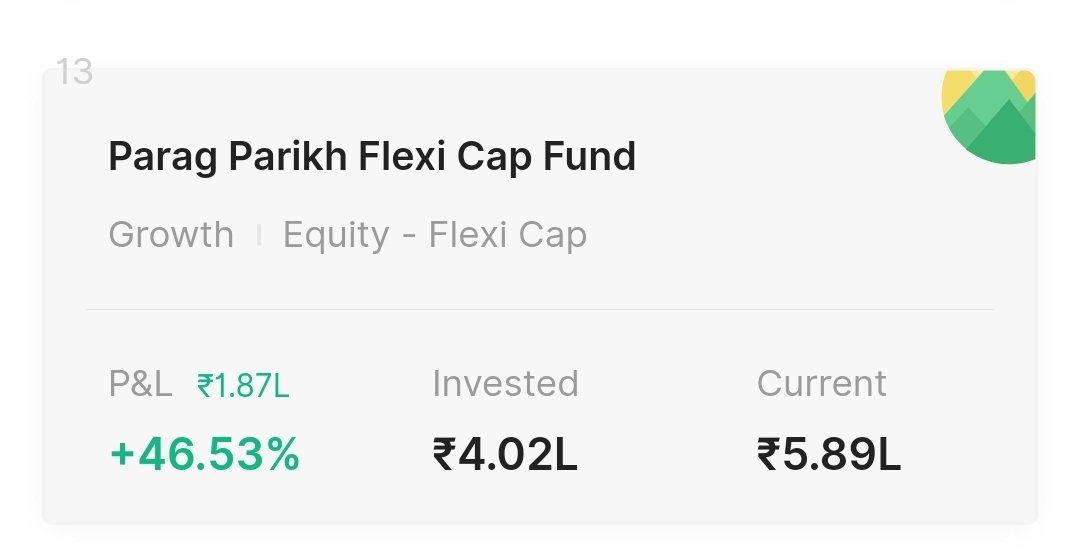

In equity funds, parag parikh flexi cap fund and mirae asset emerging bluechip funds are best. They have given superb returns in last 5 years.

Parag parikh flexi cap fund is diversified as it will invest in US stocks like Google, Facebook, Microsoft, Amazon along with Indian. https://t.co/RmoDMgXoRM

2/5

But one issue with this is if you exit before 2 years, there is an exit load of 2% in 1st year and 1% in 2nd year.

Mirae asset emerging bluechip funds stopped taking lump sum amounts and only can do SIP of Rs. 2500 currently.

3/5

But there is catch, you can do multiple SIPs in it, you can SIP on every day and still invest 75k in a month. I am doing this way only.

Coming to debt funds, ICICI prudential all seasons bond fund and hdfc corporate bond fund are good if consider 5 years performance.

4/5

In zerodha, all above 4 MFs can be pledged and haircut also very less just 7.5%. But you can use only 50% for positional margin, other 50% should come in cash or equivalent funds like gilt, liquid etc. For intraday, 100% can be used.

5/5

Nippon india gilt fund is also good, considering it will be cash component and only 10% haircut.

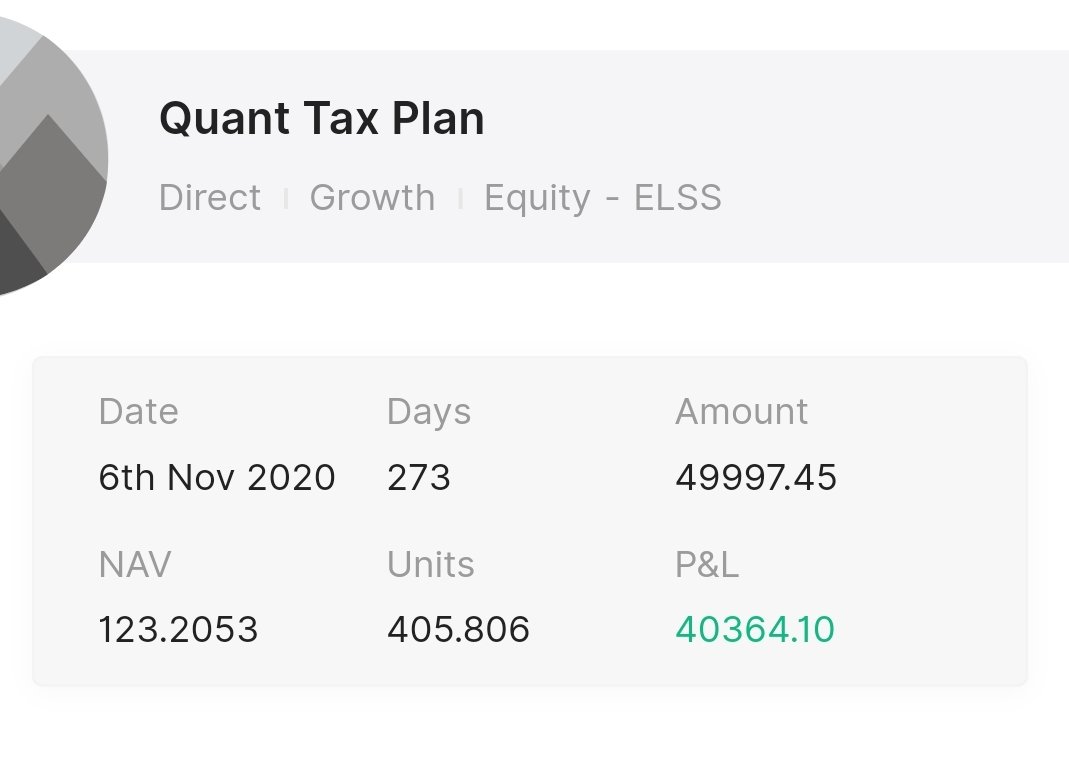

For tax saving, you need to invest in ELSS funds.

I invested in Quant Tax Plan and it gave 80% returns in just 273 days.

In equity funds, parag parikh flexi cap fund and mirae asset emerging bluechip funds are best. They have given superb returns in last 5 years.

Parag parikh flexi cap fund is diversified as it will invest in US stocks like Google, Facebook, Microsoft, Amazon along with Indian. https://t.co/RmoDMgXoRM

If I'm a layman in mutual fund territory N I wana invest Lumpsum of 1-2L N followed by SIP of 20k per month

— PythonTrader (Not a Python Coder) (@pythontrader999) August 6, 2021

1)Wat r the things I should look while scrutinising a MF

2)If I wana pledge it to broker so which kind of MF I should select @yashstocks@vishalmehta29@yogeshnanda1

2/5

But one issue with this is if you exit before 2 years, there is an exit load of 2% in 1st year and 1% in 2nd year.

Mirae asset emerging bluechip funds stopped taking lump sum amounts and only can do SIP of Rs. 2500 currently.

3/5

But there is catch, you can do multiple SIPs in it, you can SIP on every day and still invest 75k in a month. I am doing this way only.

Coming to debt funds, ICICI prudential all seasons bond fund and hdfc corporate bond fund are good if consider 5 years performance.

4/5

In zerodha, all above 4 MFs can be pledged and haircut also very less just 7.5%. But you can use only 50% for positional margin, other 50% should come in cash or equivalent funds like gilt, liquid etc. For intraday, 100% can be used.

5/5

Nippon india gilt fund is also good, considering it will be cash component and only 10% haircut.

For tax saving, you need to invest in ELSS funds.

I invested in Quant Tax Plan and it gave 80% returns in just 273 days.

More from All

Took me 5 years to get the best Chartink scanners for Stock Market, but you’ll get it in 5 mminutes here ⏰

Do Share the above tweet 👆

These are going to be very simple yet effective pure price action based scanners, no fancy indicators nothing - hope you liked it.

https://t.co/JU0MJIbpRV

52 Week High

One of the classic scanners very you will get strong stocks to Bet on.

https://t.co/V69th0jwBr

Hourly Breakout

This scanner will give you short term bet breakouts like hourly or 2Hr breakout

Volume shocker

Volume spurt in a stock with massive X times

Do Share the above tweet 👆

These are going to be very simple yet effective pure price action based scanners, no fancy indicators nothing - hope you liked it.

https://t.co/JU0MJIbpRV

52 Week High

One of the classic scanners very you will get strong stocks to Bet on.

https://t.co/V69th0jwBr

Hourly Breakout

This scanner will give you short term bet breakouts like hourly or 2Hr breakout

Volume shocker

Volume spurt in a stock with massive X times

You May Also Like

Master Thread of all my threads!

Hello!! 👋

• I have curated some of the best tweets from the best traders we know of.

• Making one master thread and will keep posting all my threads under this.

• Go through this for super learning/value totally free of cost! 😃

1. 7 FREE OPTION TRADING COURSES FOR

2. THE ABSOLUTE BEST 15 SCANNERS EXPERTS ARE USING

Got these scanners from the following accounts:

1. @Pathik_Trader

2. @sanjufunda

3. @sanstocktrader

4. @SouravSenguptaI

5. @Rishikesh_ADX

3. 12 TRADING SETUPS which experts are using.

These setups I found from the following 4 accounts:

1. @Pathik_Trader

2. @sourabhsiso19

3. @ITRADE191

4.

4. Curated tweets on HOW TO SELL STRADDLES.

Everything covered in this thread.

1. Management

2. How to initiate

3. When to exit straddles

4. Examples

5. Videos on

Hello!! 👋

• I have curated some of the best tweets from the best traders we know of.

• Making one master thread and will keep posting all my threads under this.

• Go through this for super learning/value totally free of cost! 😃

1. 7 FREE OPTION TRADING COURSES FOR

A THREAD:

— Aditya Todmal (@AdityaTodmal) November 28, 2020

7 FREE OPTION TRADING COURSES FOR BEGINNERS.

Been getting lot of dm's from people telling me they want to learn option trading and need some recommendations.

Here I'm listing the resources every beginner should go through to shorten their learning curve.

(1/10)

2. THE ABSOLUTE BEST 15 SCANNERS EXPERTS ARE USING

Got these scanners from the following accounts:

1. @Pathik_Trader

2. @sanjufunda

3. @sanstocktrader

4. @SouravSenguptaI

5. @Rishikesh_ADX

The absolute best 15 scanners which experts are using.

— Aditya Todmal (@AdityaTodmal) January 29, 2021

Got these scanners from the following accounts:

1. @Pathik_Trader

2. @sanjufunda

3. @sanstocktrader

4. @SouravSenguptaI

5. @Rishikesh_ADX

Share for the benefit of everyone.

3. 12 TRADING SETUPS which experts are using.

These setups I found from the following 4 accounts:

1. @Pathik_Trader

2. @sourabhsiso19

3. @ITRADE191

4.

12 TRADING SETUPS which experts are using.

— Aditya Todmal (@AdityaTodmal) February 7, 2021

These setups I found from the following 4 accounts:

1. @Pathik_Trader

2. @sourabhsiso19

3. @ITRADE191

4. @DillikiBiili

Share for the benefit of everyone.

4. Curated tweets on HOW TO SELL STRADDLES.

Everything covered in this thread.

1. Management

2. How to initiate

3. When to exit straddles

4. Examples

5. Videos on

Curated tweets on How to Sell Straddles

— Aditya Todmal (@AdityaTodmal) February 21, 2021

Everything covered in this thread.

1. Management

2. How to initiate

3. When to exit straddles

4. Examples

5. Videos on Straddles

Share if you find this knowledgeable for the benefit of others.