Later came a stage where I realized Benjamin style was not working.

A thread: How to value? 🏦💰❓

Sharing my learnings from my journey so far.

Later came a stage where I realized Benjamin style was not working.

If you have been following me for the past 1 year you would have noticed how my valuation method has changed.

“Take help of someone to learn it” is the crucial line there.

read bruce greenwald book on value investing. he has taught valuation. just learn how to compute company sales and profit on average and value that. many get wrong by looking at just trailing pe/pb. take help of someone to learn it.

— ContrarianEPS (@contrarianEPS) February 9, 2021

Again if you have been following me for more than a year, I used to be the “CCL Product guy”. I was so bullish on the company that I had my 70% portfolio in it.

After we connected we discussed various businesses, especially CCL Products because we both were tracking it very carefully. Soon, he offered me to write blogs for @soicfinance and the learning started.

@badola_arjun Hi keep up the good work, and keep putting out content. Really liked your work on CCL and the Buffett letters \U0001f4af\U0001f601

— ishmohit (@ishmohit1) November 20, 2020

1. Good business available at extremely cheap valuation

2. Great-Good business with reasonable valuation

3. Good business but can’t compromise on valuation

In this situation the business analysis provides you insights that you understand such a business should not be trading at current valuation.

The example for this situation would be companies like ICICI Securities and Manappuram Finance.

Manappuram Finance: This gold lending business is another one which falls under this category...

In this situation you would be able to identify that there is a Great-Good business which on the face of it looks expensive but actually available at reasonable valuations.

In this category falls the music streaming business Saregama.

Disclosure: my buying price is around Rs.2400 with the highest allocation.

The stock was already 10-11x from its March 2020 lows and trading around 40 PE.

My first reaction was, “Dammit! I missed the bus.” I saw the chart and looked at the 1999-2000 peak and thought “Aur kitna upar jaayega”…

He said absolute valuation matters. New facts of the business were emerging as their Caravan sales went to zero, the hidden gem came into the limelight.

1. Their music streaming was growing above 20% (rather they have increased the guidance to 25-30% now)

3. no threat from new entrant (except foreign players)

4. Top player was losing out focus on the music business

5. visibility of growth for next 2-3 years

Over here, one identifies a good business but the entry valuation is very important here. As with these businesses the cycle could change suddenly, their raw material prices could fluctuate, or they do not have moat, etc.

I was a little late to read this business and missed the opportunity. I couldn’t buy a small player at 40 PE, 3.5 Price to Sales, and with lowest return ratios in the hope that management would perform. The risk to reward was not in favor.

The mistake in the first situation would be opportunity cost. In second, it would be the risk in identifying the wrong business and in third it is overpaying for the business.

More from Valuation

When we put a high multiple to sales, the most important thing to worry about is - what could disrupt those cash flows. A lower multiple to sales (like a 1x or 2x) justifies Yo-Yo cyclicality and 10x sales implies relatively stable gross margins, cash flow and business economics.

It's amazing \U0001f60a 25% NP

— Avinash (@Aviral_Bharat) February 17, 2022

$8b revenue

$2b Profit

$92b MCap

At 11 times revenue, it seems to be cheap compared to\U0001f609

You May Also Like

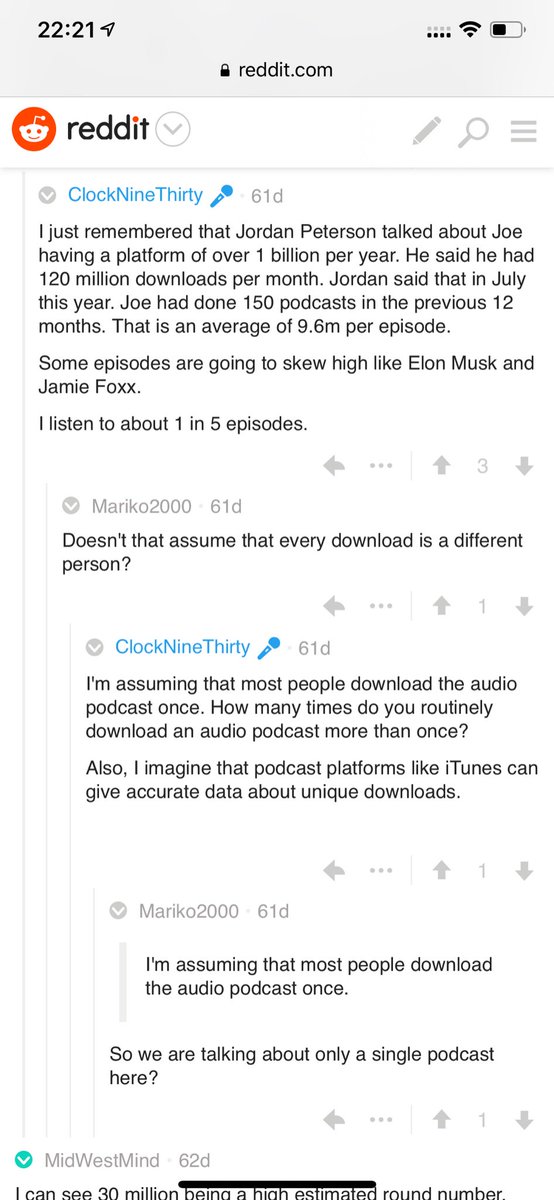

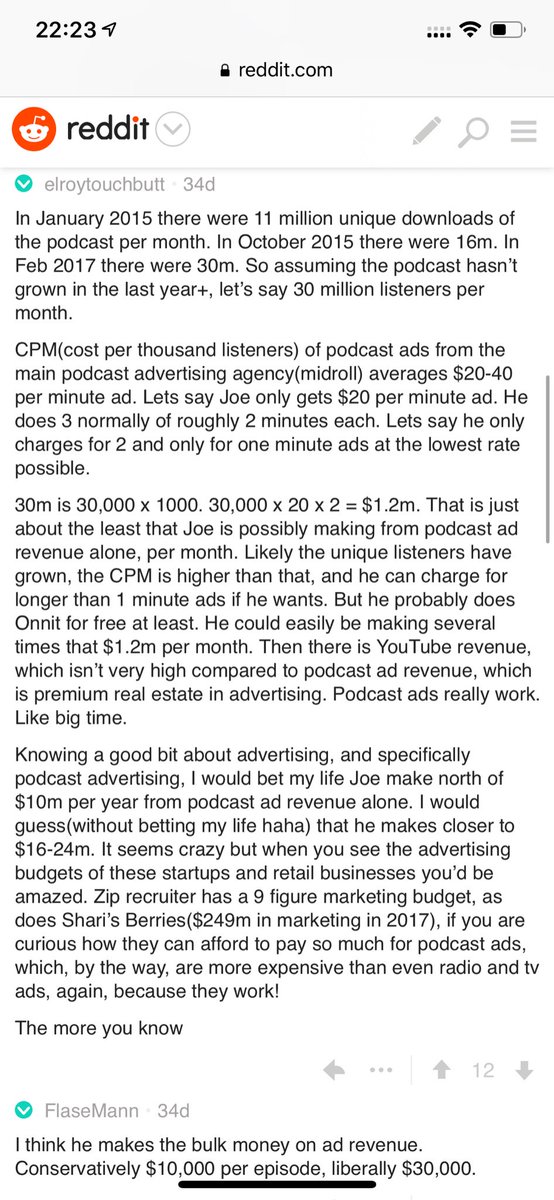

Joe Rogan's podcast is now is listened to 1.5+ billion times per year at around $50-100M/year revenue.

Independent and 100% owned by Joe, no networks, no middle men and a 100M+ people audience.

👏

https://t.co/RywAiBxA3s

Joe is the #1 / #2 podcast (depends per week) of all podcasts

120 million plays per month source https://t.co/k7L1LfDdcM

https://t.co/aGcYnVDpMu

Independent and 100% owned by Joe, no networks, no middle men and a 100M+ people audience.

👏

https://t.co/RywAiBxA3s

Joe is the #1 / #2 podcast (depends per week) of all podcasts

120 million plays per month source https://t.co/k7L1LfDdcM

https://t.co/aGcYnVDpMu