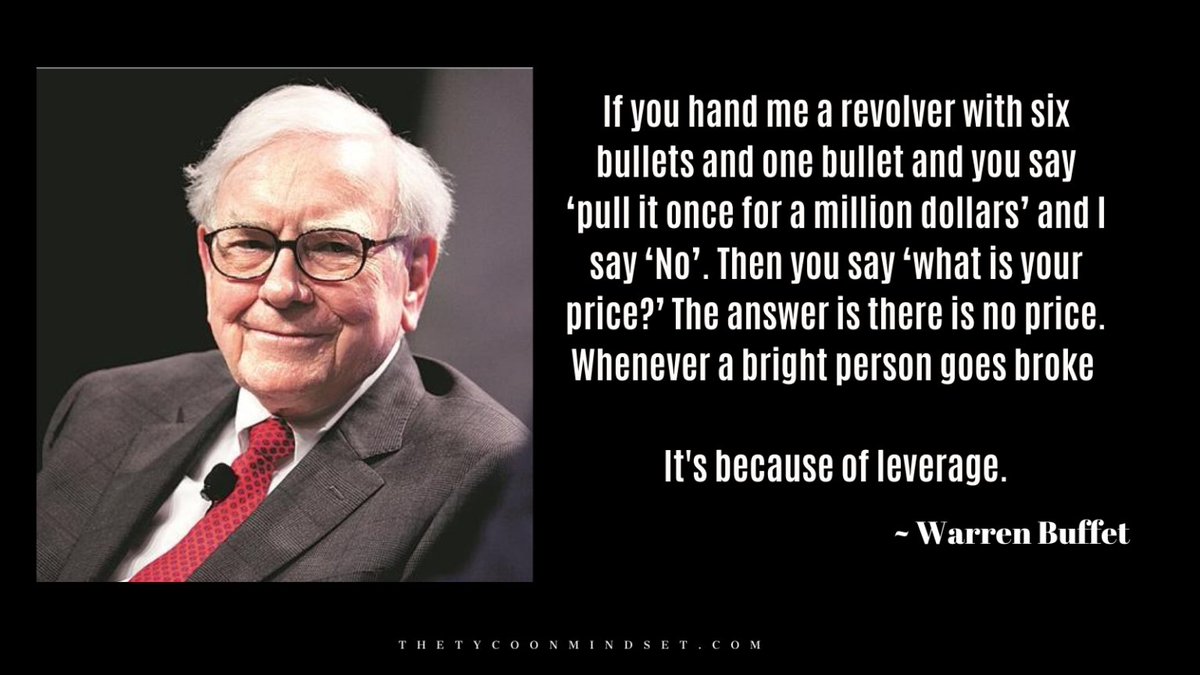

1). On LTCM:

Munger: What was interesting was how talented they were and then also got in so much trouble. It also demonstrates general system of finance involving derivatives is irresponsible.

Warren: Here you had extremely experienced people operating with their own money.

• They went broke. Why do people risk losing something very important to gain something that’s totally unimportant? The added money has no utility whatsoever.

If almost impossible to go broke without borrowed money being in the equation. No gain is good enough when there is no gain to offset the risk of loss.

2. Estimating Company’s IV

Warren: Investment is process of putting money today to get more money back in the future. The question is how far in the future, how much money and what is the appropriate discount rate to take it back to the present day and determine how much to pay?

• One important element in Berkshire is because we retain all earnings and we have a growth of float over time. We have a considerable amount of money to invest. The success with which we invest those will be an important factor in estimating how fast our intrinsic value grows.

• The investment of new money depends, to a big extent, on external factors. If we run into favourable external circumstances then your calculation of intrinsic value would result in a higher number.

3. Circle of competence

Warren: It is much easier to predict the relative strength that Coke will enjoy in the soft drink world than it is to predict the strength of a technology company.

Now somebody that has a lot of familiarity with software may very well be able to act on the superior knowledge and make more money on it. There is nothing wrong with it. I don’t have that kind of knowledge.

4. Question from

@MohnishPabrai on Leveraging Circle of Competence

Que- I have a notion that both Mr. Munger and Mr. Buffett understand the Kleiner Perkins model of early- stage venture capital investing and currently their focus in the internet space, extremely well.

If Kleiner Perkins approached you for starting a early stage or later stage internet investment fund, would that investment be under your circle of competence?

Ans:

Warren: Charlie and I both understand the process of early-stage investment probably as well as anyone

We haven’t participated in it. There are certain things we don’t even like about it. And I would say that no, we would not have an interest in investing in the fund.

In terms of picking up businesses that are going to do wonderfully as business, not as a stock for a while.

The Internet will have a huge impact on the world. But I am not sure that makes it an easy investment decision.

5. Advise for young people

Warren: Start young. The nature of compound interest behaves like a snowball of sticky snow. I would probably focus on smaller companies because that would be working with smaller sums and there is more chance that something is overlooked in that arena

• You have to buy businesses or a little piece of business, you have to buy them at attractive prices and you have to buy into good businesses.

6. Asking question before investing

Warren: question yourself, “what do I not know that I need to know?”. I would talk to employees of the company and ask those kinds of questions. Essentially you are a reporter. It is just like journalism.

•You talk to competitors and ask “If you had a silver bullet and you could put it through the head of 1 of your competitors, which one would it be and why?”

“If you were to go away for 10 years and you had to put all your money into one of the competitors which one would that be

You will learn a lot from these kinds of questions. The biggest thing is to find out how the businesses operate.

Munger: if you want to get smart you have to keep asking, Why? Why? Why? And then relate the answer to a structure of deep theory. You have to know the main theories.

7. Learning through magazines

Munger: We learned more from the great business magazines than we do anywhere else. It’s such an easy shorthand way of getting a vast variety of business experiences just to riffle through issue after issue covering a great variety of businesses.

• If you get a mental habit of relating what you are reading to the basic structure of the underlying ideas being demonstrated, you gradually accumulate some wisdom about investing.

8. Priority to Acquire Business

Warren: We have always wanted to acquire entire businesses. We have found that much of the time we could get far for our money, in terms of wonderful businesses, by buying pieces in the stock market than by negotiated purchase.

9. Buy and hold

Warren: People think they would sell and buy it back cheaper. It’s pretty tough to do. You have to make 2 decisions right. You have to sell it right first and then then buy it right later on and pay some taxes in between.

• If you get into a wonderful business, the best thing to do usually is to stick to it.

Munger: Trying to dance in and out of the companies you really love has not been a good idea for most investors.

To read more key takeaways on Berkshire Hathaway AGM: 1999, refer to this link.

https://t.co/4bNJ26pRHB