Am sharing my journey on how I started trading 15 years before when there was very limited resource. If you are a beginner who is looking to get started with Stock Market, this thread would be helpful.\U0001f9f5

— Kirubakaran Rajendran (@kirubaakaran) April 26, 2022

I have shared multiple information related to trading and investing through my historical data analysis by writing various articles, here's the master thread that contains all my work in one place.🧵

Many of my friends who work at Corporate culture are fed up with their work life, one question they keep asking me is how much money do I need to retire and live comfortably? Here\u2019s a short thread \U0001f9f5 pic.twitter.com/gNEOFOChlh

— Kirubakaran Rajendran (@kirubaakaran) May 24, 2022

Year 2022 has been disastrous for many asset classes, the world economy is at 40 year high inflation. Are we headed for another stock market crash? Here's a detailed analysis. \U0001f9f5 pic.twitter.com/ZYch9yBHEq

— Kirubakaran Rajendran (@kirubaakaran) May 19, 2022

I have closely observed FinNifty for couple of weeks and then started trading live since last 4 expiry. If you are looking to start trading with FinNifty weekly option then this thread might be of great help to you. \U0001f9f5

— Kirubakaran Rajendran (@kirubaakaran) July 12, 2022

Here's a detailed analysis of 920 Straddle with 25% SL using @stockmock_in platform. This analysis would show which days are max profitable, how it behaves on gap days and how it behaves on different VIX days. \U0001f9f5

— Kirubakaran Rajendran (@kirubaakaran) May 8, 2022

Every time after I make a SIP investment, market tends to go down in next couple of days. I always wondered I would have made higher returns with my SIP if I waited for market correction. Does making SIP during market correction generates higher returns. Here\u2019s the details \U0001f9f5 pic.twitter.com/bsnz9ySi96

— Kirubakaran Rajendran (@kirubaakaran) June 29, 2022

What is Rakesh Jhunjhunwala's Investing Strategy, is there a way where we retail investors can follow his strategy and generate similar returns like him? We did an extensive research and this is what we found. A short thread pic.twitter.com/2gq9vNqv22

— Kirubakaran Rajendran (@kirubaakaran) September 29, 2021

A small thread on Mindset of a successful trader. What differentiates best traders from the bad ones? Why 95% of the traders don\u2019t make money? Trading is an unpredictable game, how could one win in that? 1/n pic.twitter.com/ZHMZ2wZXxK

— Kirubakaran Rajendran (@kirubaakaran) March 25, 2021

A short thread on The 80/20 rule for Trading and Investing. If you really want to improve your trading result, follow this one simple approach which can immediately show you the reason why you weren\u2019t able to make profits in the stock market. pic.twitter.com/2clnYVzahE

— Kirubakaran Rajendran (@kirubaakaran) May 4, 2021

In general, making money from trading is real hard than any other business. And I believe discretionary trading is even more harder. Why do many beginners go bust within 90 days of their trading career? Here's a short thread on why discretionary trading is hard? pic.twitter.com/4av9E0YSkm

— Kirubakaran Rajendran (@kirubaakaran) November 18, 2021

Most beginners when building a trading strategy simply use current info and test with it, they don't know How to Get Historical Stock Futures lot size, list of stocks that are part of index like Nifty 50, Nifty 500 historically, I will share all such info in this thread

— Kirubakaran Rajendran (@kirubaakaran) September 9, 2021

Russian stock market crashed more than 70%, many investors are worried on what would happen if such things happen to Indian markets? Here's couple of important lesson you need to keep in mind before you start your SIP journey. A short thread pic.twitter.com/m0QQ1aGnsN

— Kirubakaran Rajendran (@kirubaakaran) March 8, 2022

Are you a trader who did an extensive backtest of your trading strategy only to witness a worst performance when you traded live? Wondering why your real live results are not matching with your backtest results? Then this short thread is for you. pic.twitter.com/sx8WsGeejJ

— Kirubakaran Rajendran (@kirubaakaran) February 24, 2022

Should you buy stocks that gets added to #Nifty50. A short thread with detailed analysis from 25+ years of Historical data. Nifty 50 is widely tracked index, all stocks that are being included/excluded with Nifty 50 will have an impact towards the stock returns for next one year pic.twitter.com/XUtYSUl0mm

— Kirubakaran Rajendran (@kirubaakaran) June 13, 2021

Investing for long term is always projected as a complex task, reading about the nature of company business, balance sheets, Profit and loss statements etc. Is there any easy way to find the best stocks to invest for long term? That's what this thread is all about. pic.twitter.com/DJw06FMfw2

— Kirubakaran Rajendran (@kirubaakaran) March 21, 2022

Many beginners give utmost importance to trading strategy but least bothered about position sizing. Knowing how much is too much in a trade? This information is very crucial which determines the long term success of a trader. In this thread will explain what is position sizing pic.twitter.com/tkuOJ3JQ6L

— Kirubakaran Rajendran (@kirubaakaran) March 1, 2022

Here's a thread on complete data analysis of #NSE500 stocks, to start with, first checked the momentum factor, what was the last 12 months returns of all sectors of NSE 500. IT sector stocks top the list with average returns of 90% in last one year. 1/n pic.twitter.com/3VwS5XY11Z

— Kirubakaran Rajendran (@kirubaakaran) March 2, 2021

A thread on Position Sizing #Trading is the only profession where you can see Doctors, Engineers, and many other successful professionals try their luck with stock market, these people excel in their own respective field but struggle a lot when it comes to trading.1/n

— Kirubakaran Rajendran (@kirubaakaran) February 16, 2021

Nifty 14500 CE trade which made day low price of 0.15 and day high price of 2139, due to erroneous order by a broker who lost 250 crores. Some ppl claim few others brokers made 50 to 75 crores profits. But what really happened? Here's the tick data analysis that shows true info\U0001f9f5

— Kirubakaran Rajendran (@kirubaakaran) June 3, 2022

Whenever #Nifty & #BankNifty closes less than -1% on Fridays, what happens on Monday and what happens on next 30 days. Interesting analysis, will be sharing the details shortly.

— Kirubakaran Rajendran (@kirubaakaran) November 27, 2021

What happens if we buy a stock in cash segment that gets added to F&O ban list and sell that stock once it comes of F&O ban list. Tested this #TradingStrategy with last 5 years of historical data, here's the details. pic.twitter.com/dcFLkX49jY

— Kirubakaran Rajendran (@kirubaakaran) October 20, 2021

When it comes to investing, most beginners who want to get started with stock market investing opt for mutual funds. But do you know how many mutual funds there are in India? There are more than 2,500\xa0mutual fund schemes.

— Kirubakaran Rajendran (@kirubaakaran) June 8, 2022

How do we decide which one to invest?Here\u2019s a short \U0001f9f5 pic.twitter.com/tIp14488hE

Monthly SIP is one most underrated investment option many people tend to ignore during their early stage of professional career. You really don\u2019t need to invest lot of money, in fact just investing Rs.5000 every month at the Age of 25 can you fetch you almost 2 Crores corpus. \U0001f9f5

— Kirubakaran Rajendran (@kirubaakaran) June 20, 2022

\u201cWhenever I enter into a trade, I end up losing money. Should I stop trading and start investing?\u201d This is a common question that comes in our mind very often during our early phase. Here\u2019s a short thread that explains what we are doing wrong and how to correct it?

— Kirubakaran Rajendran (@kirubaakaran) May 11, 2022

More from Kirubakaran Rajendran

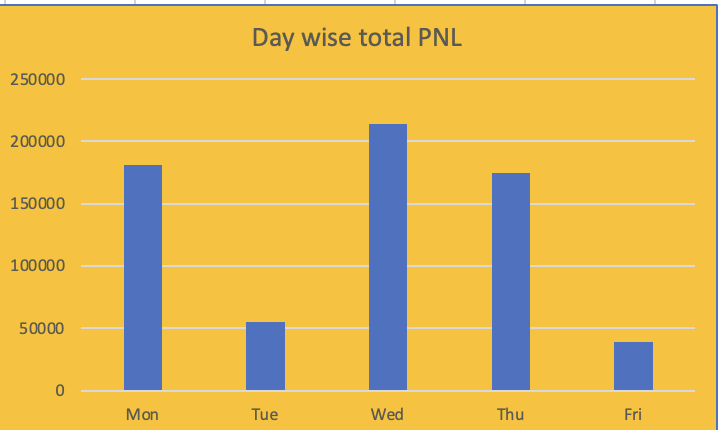

Here's a detailed analysis of 920 Straddle with 25% SL using @stockmock_in platform. This analysis would show which days are max profitable, how it behaves on gap days and how it behaves on different VIX days. 🧵

Here's day wise total profits, Wednesday are the days it has generated highest profits compared to all other days and Friday being the least profitable day.

Here's day wise average profits, obviously Wednesday are the days it has generated highest average profits compared to all other days and Friday being the least profitable day.

Even the live profits after all charges generated through 920 straddle trading bots at https://t.co/AKj4vqky6X also reflected Fridays are not profitable when you incur all charges. Wednesday being the most profitable day. Live profits are shown here https://t.co/3hgti23lRB

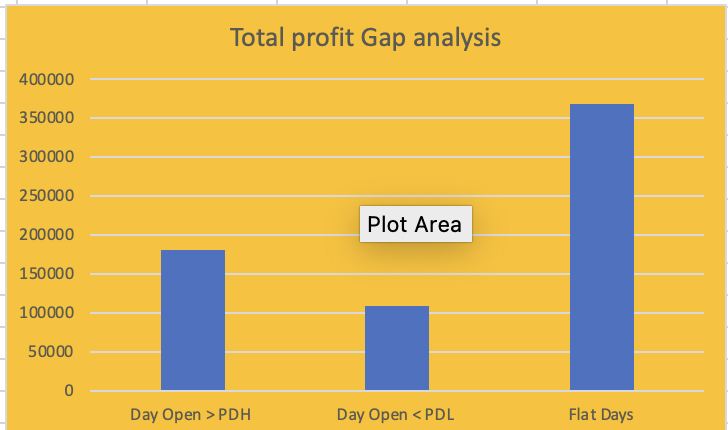

Here's total profits made during gaps, when day open is greater than previous day high, Day open < Prev day low and flat days. Irrespective of gaps, its able to generate profits over all. Even the avg profits denotes the same

Here's day wise total profits, Wednesday are the days it has generated highest profits compared to all other days and Friday being the least profitable day.

Here's day wise average profits, obviously Wednesday are the days it has generated highest average profits compared to all other days and Friday being the least profitable day.

Even the live profits after all charges generated through 920 straddle trading bots at https://t.co/AKj4vqky6X also reflected Fridays are not profitable when you incur all charges. Wednesday being the most profitable day. Live profits are shown here https://t.co/3hgti23lRB

Here's total profits made during gaps, when day open is greater than previous day high, Day open < Prev day low and flat days. Irrespective of gaps, its able to generate profits over all. Even the avg profits denotes the same

More from Thread

You May Also Like

My top 10 tweets of the year

A thread 👇

https://t.co/xj4js6shhy

https://t.co/b81zoW6u1d

https://t.co/1147it02zs

https://t.co/A7XCU5fC2m

A thread 👇

https://t.co/xj4js6shhy

Entrepreneur\u2019s mind.

— James Clear (@JamesClear) August 22, 2020

Athlete\u2019s body.

Artist\u2019s soul.

https://t.co/b81zoW6u1d

When you choose who to follow on Twitter, you are choosing your future thoughts.

— James Clear (@JamesClear) October 3, 2020

https://t.co/1147it02zs

Working on a problem reduces the fear of it.

— James Clear (@JamesClear) August 30, 2020

It\u2019s hard to fear a problem when you are making progress on it\u2014even if progress is imperfect and slow.

Action relieves anxiety.

https://t.co/A7XCU5fC2m

We often avoid taking action because we think "I need to learn more," but the best way to learn is often by taking action.

— James Clear (@JamesClear) September 23, 2020