Let's first understand how a sugar factory works:

Sugarcane is crushed in a sugar factory that primarily extracts sugar syrup and fiber which is called bagasse. Bagasse is used to generate electricity, the excess power generates is then sold to the electricity companies.

Sugar syrup is then boiled to extract sugar, the syrup can be boiled up to three times to extract maximum sugar, and the residue left is known as molasses

Molasses can be further processed to generate ethanol and alcohol

The sugar syrup if being boiled twice generate B heavy molasses which has more sugar content hence can generate higher ethanol, the syrup boiled three times leaves C heavy molasses which has very low sugar content having lower ethanol yield

Ethanol can also be extracted directly from sugar syrup without making sugar, this leads to the highest ethanol yield and also fetches higher ethanol prices in the market.

Industry operation

The sugar industry is heavily regulated by the government as there are only 550 sugar factories that support the livelihood of around 11 crore people directly or indirectly.

The sugar industry has always been cyclical, impacted by the overproduction of sugar..

.. high government regulations, overcapacity issues, lower international sugar prices, etc

The cyclical nature of the industry is poised to change due to the ethanol opportunity, the government has announced an ethanol blending target of 20% to be achieved by 2025

Govt fixes the FRP (Fair remunerative price) i.e. the price sugar factories have to pay farmers for sugarcane, currently the price is fixed at Rs 2850 per tonne while some states also fix SAP (State advised price), currently SAP of Rs 3150 per tonne has been fixed by the UP govt

The government also fixes the selling price of sugar known as MSP (Minimum selling price) at which the sugar is sold in the market by the sugar companies, currently the price is fixed at Rs 31 per kg.

Price trend of ERP, SAP, and MSP over the years:

The increasing FRP and SAP prices have hurt the sugar companies as MSP has remained unchanged during the period, this in turn increases the arrears which the sugar companies are liable to pay to sugarcane farmers

Cane arrears trend:

Demand supply dynamics:

Indian sugar companies have been struggling primarily due to more supply than demand in the local market and they are unable to export as international sugar prices are lower than their cost of production, this makes export uneconomical.

There has been excess supply to the tone of 4 -5 million tonnes per year which sugar companies have to export at prices below their cost even after government subsidy.

This dynamic has been changing slowly due to lower sugar production in Brazil as cane supplies are tight due to a severe drought that’s been ravaging yields in Brazil. Cane-crushing dropped 31% in the first half of April compared to a year ago, according to industry group Unica.

The white sugar prices have gained over the past year amid supply and logistic constraints:

This has led to higher export price realization for sugar, which has now become economical for the Indian sugar industry to export its produce

Exports also have become remunerative despite cut in export subsidy by 44%

Unit Economics:

Sugar companies have three options to utilize sugar syrup:

•Option 1: Heating the syrup thrice generating C heavy molasses, yielding 11%-11.5% sugar

•Option 2: Heating the syrup twice generating B heavy molasses, yielding 9%-9.5% sugar

•Option 3: Directly producing ethanol from syrup without producing sugar

This leads to the following yield and revenue generation per tonne of sugarcane:

Ethanol prices have been fixed by the govt according to different grades of extraction. The clear choice for sugar companies is ethanol production directly from sugar syrup but ethanol production requires distillery capacity which the companies have already started to expand.

Changing dynamics:

Indian sugar industry’s rough business split is 60%-65% sugar, 20%-25% ethanol, and 10%-15% electricity generation. This is bound to change due to the higher cyclicality of sugar prices with large working capital requirements as compared to ethanol production..

..which generates higher revenue combined with low working capital requirement (OMCs payment cycle for ethanol is 1 to 2 months)

This sugar industry in Brazil (which is most advanced) diverts sugarcane production in the following manner:

The strategic shift of sugar companies to ethanol manufacturing will lead to higher realizations per tonne. The overall industry is poised well to follow the Brazil sugar industry model as bio-fuels gain more ground and acceptance in India.

Brazil produced 30 Mn tonnes of sugar, on the same lines India produced 27 Mn tonnes of sugar during the sugar season but Brazil’s ethanol production was 10 times more than India. A lot of auto companies there manufacture flex-fuel vehicles, which run on up to 100% ethanol.

The minimum ethanol blending in Brazil is 26%. These blends are called E-100 and E-26. That is, the first category consists completely of ethanol while the second has 26% ethanol blended in petrol.

The reason behind this is the policy of sugar mills in Brazil of making ethanol directly from 65% of cane juice. We have only now started making ethanol directly from cane juice.

India should implement a more “ambitious” biofuel program that will help its sugar mills to increase production of ethanol and “balance the world sugar market”, according to Eduardo Leão de Sousa, executive director of UNICA

Ethanol capacity of 1000 Cr Liters will be required to meet the 20% blending requirement which will be added by B heavy molasses capacity expansion and grain-based capacity expansion

283 crore ltr of ethanol worth about Rs 15,800 cr will be bought by petroleum marketing companies from the sugar mills during the current season. Thus, the earnings from ethanol are turning into a big source of revenue for the sugar industry for payments to be made to the farmers

The government’s policy has been welcomed by the industry and various key players have initiated capital expenditure to expand ethanol capacity.

https://t.co/ADtGvps5qN

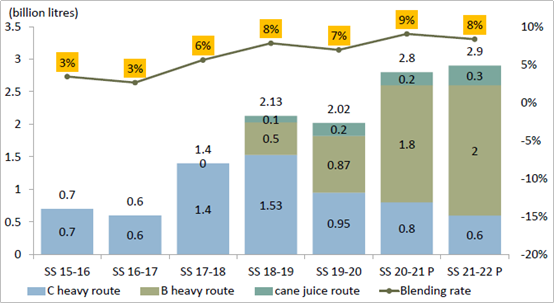

Ethanol blending has increased from 3% in 2015 to 9% currently largely contributed by the increase in B heavy molasses ethanol processing

This thread was inspired by

@varinder_bansal's excellent coverage on the sugar sector with Narendra Murkumbi

You can still watch:

https://t.co/BmHKxtl5O5

The various data points have been taken from Crisil's report on the sugar industry and various news articles.