It's a beautiful Saturday on this Corona riddled planet. It's a good day to do the following:

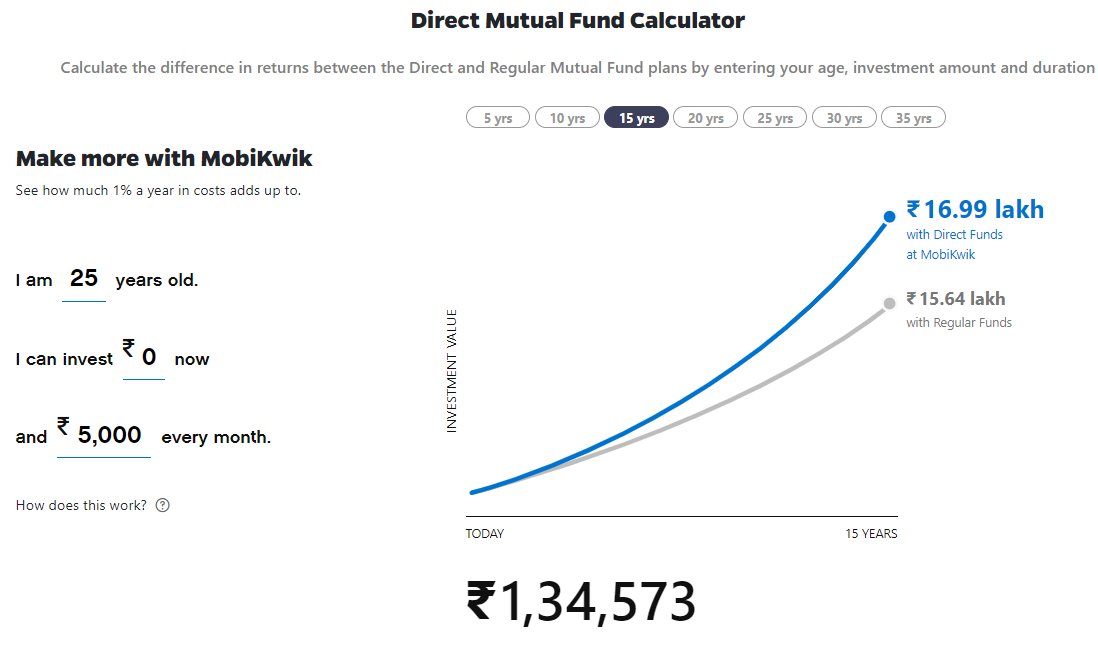

1. Open your account statement and find out how much commissions you are paying. You'd be paying anywhere between 0.7% to 1.3% extra over direct plans.

AND DON"T FUCKING WATCH CNBC, Zee Biz and listen to those gurus. They're on for one reason - to make money

https://t.co/JRsxckZKOJ

This is pretty wild and quite funny.

— Artificially intelligent fool \U0001f9e0 (@passivefool) January 13, 2021

A TV anchor was buying the stocks before he recommended them on TV the next day and got caught. https://t.co/DlBgykUh3t pic.twitter.com/8X1Cu0BfB0

If it's worth stick with your adviser. the better adviser would be someone who charges a flat fee but there are 7 of those in India. Look for one.

https://t.co/WgYK5P1at1

https://t.co/hRYFBGxy3O

More from Artificially intelligent fool 🧠

More from Finance

The Dutch regulator and DNB as financial supervisor are a tough cookie to deal with. In essence they hyperregulate EU-rules into goldplated Dutch rules which go beyond what is prescribed in Europe.

All NL-customers at British banks may thus be kicked out on brexit.

Thread

/1

If we start with the capital requirements directive, it says attracting deposits is forbidden. In article 9.

https://t.co/RYl7SXligC

Now the translation of that rule into Dutch law is slightly expanded to not only prohibit attracting deposits, but to also prohibit, having those deposits under custody ('ter beschikking hebben').

That's not in EU law, but it is in our Dutch law.

https://t.co/PsbWfNY3PA

So if you wonder how this would work out for UK banks and Payment institutions servicing Dutch customers. Have a read at the technical explanation of DNB, the financial supervisor and their summarising table.

https://t.co/LL0fAnYkRJ

Passive servicing of Dutch is not allowed!

Any bank or PSP in the UK that continues to serve Dutch customers (as in retail customers, professional players are excepted) can thus be subject to fines and policing under Dutch law.

Meaning we not only have Accidental American issues in payments, but also Accidental Dutchies

All NL-customers at British banks may thus be kicked out on brexit.

Thread

/1

If we start with the capital requirements directive, it says attracting deposits is forbidden. In article 9.

https://t.co/RYl7SXligC

Now the translation of that rule into Dutch law is slightly expanded to not only prohibit attracting deposits, but to also prohibit, having those deposits under custody ('ter beschikking hebben').

That's not in EU law, but it is in our Dutch law.

https://t.co/PsbWfNY3PA

So if you wonder how this would work out for UK banks and Payment institutions servicing Dutch customers. Have a read at the technical explanation of DNB, the financial supervisor and their summarising table.

https://t.co/LL0fAnYkRJ

Passive servicing of Dutch is not allowed!

Any bank or PSP in the UK that continues to serve Dutch customers (as in retail customers, professional players are excepted) can thus be subject to fines and policing under Dutch law.

Meaning we not only have Accidental American issues in payments, but also Accidental Dutchies

You May Also Like

MASTER THREAD on Short Strangles.

Curated the best tweets from the best traders who are exceptional at managing strangles.

• Positional Strangles

• Intraday Strangles

• Position Sizing

• How to do Adjustments

• Plenty of Examples

• When to avoid

• Exit Criteria

How to sell Strangles in weekly expiry as explained by boss himself. @Mitesh_Engr

• When to sell

• How to do Adjustments

• Exit

Beautiful explanation on positional option selling by @Mitesh_Engr

Sir on how to sell low premium strangles yourself without paying anyone. This is a free mini course in

1st Live example of managing a strangle by Mitesh Sir. @Mitesh_Engr

• Sold Strangles 20% cap used

• Added 20% cap more when in profit

• Booked profitable leg and rolled up

• Kept rolling up profitable leg

• Booked loss in calls

• Sold only

2nd example by @Mitesh_Engr Sir on converting a directional trade into strangles. Option Sellers can use this for consistent profit.

• Identified a reversal and sold puts

• Puts decayed a lot

• When achieved 2% profit through puts then sold

Curated the best tweets from the best traders who are exceptional at managing strangles.

• Positional Strangles

• Intraday Strangles

• Position Sizing

• How to do Adjustments

• Plenty of Examples

• When to avoid

• Exit Criteria

How to sell Strangles in weekly expiry as explained by boss himself. @Mitesh_Engr

• When to sell

• How to do Adjustments

• Exit

1. Let's start option selling learning.

— Mitesh Patel (@Mitesh_Engr) February 10, 2019

Strangle selling. ( I am doing mostly in weekly Bank Nifty)

When to sell? When VIX is below 15

Assume spot is at 27500

Sell 27100 PE & 27900 CE

say premium for both 50-50

If bank nifty will move in narrow range u will get profit from both.

Beautiful explanation on positional option selling by @Mitesh_Engr

Sir on how to sell low premium strangles yourself without paying anyone. This is a free mini course in

Few are selling 20-25 Rs positional option selling course.

— Mitesh Patel (@Mitesh_Engr) November 3, 2019

Nothing big deal in that.

For selling weekly option just identify last week low and high.

Now from that low and high keep 1-1.5% distance from strike.

And sell option on both side.

1/n

1st Live example of managing a strangle by Mitesh Sir. @Mitesh_Engr

• Sold Strangles 20% cap used

• Added 20% cap more when in profit

• Booked profitable leg and rolled up

• Kept rolling up profitable leg

• Booked loss in calls

• Sold only

Sold 29200 put and 30500 call

— Mitesh Patel (@Mitesh_Engr) April 12, 2019

Used 20% capital@44 each

2nd example by @Mitesh_Engr Sir on converting a directional trade into strangles. Option Sellers can use this for consistent profit.

• Identified a reversal and sold puts

• Puts decayed a lot

• When achieved 2% profit through puts then sold

Already giving more than 2% return in a week. Now I will prefer to sell 32500 call at 74 to make it strangle in equal ratio.

— Mitesh Patel (@Mitesh_Engr) February 7, 2020

To all. This is free learning for you. How to play option to make consistent return.

Stay tuned and learn it here free of cost. https://t.co/7J7LC86oW0