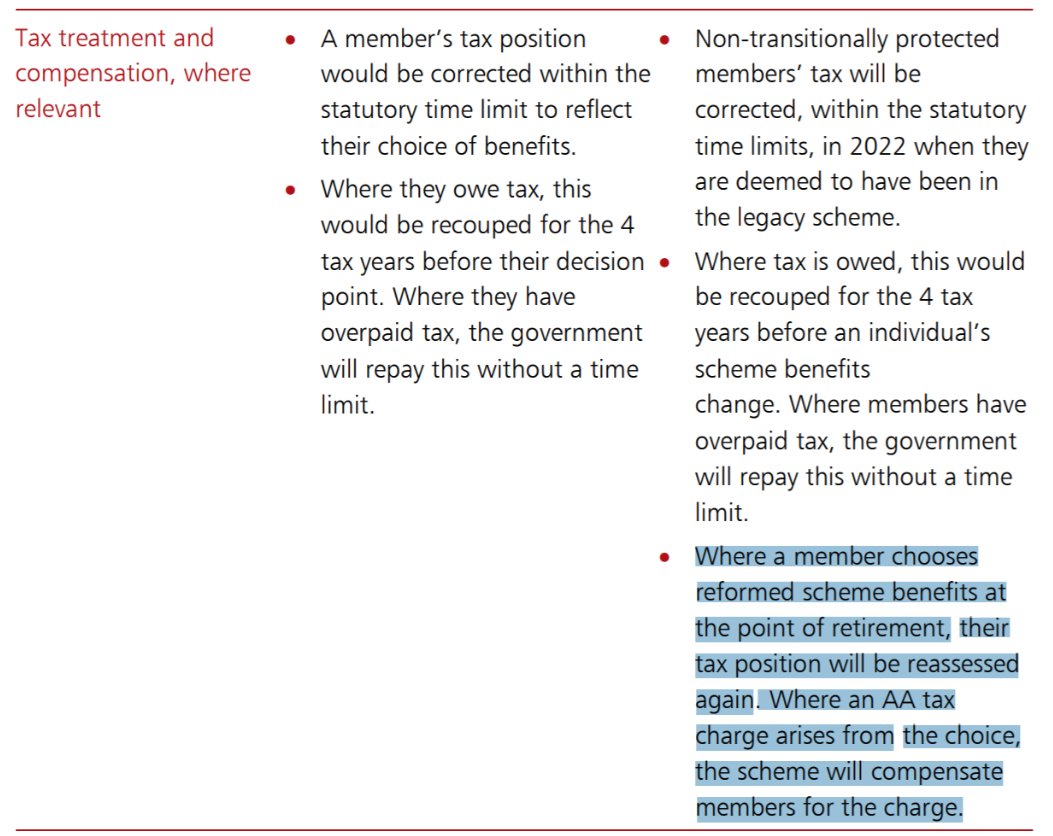

TSMC $TSM projecting capital expenses of 25-28B USD in 2021. 80% allocated for advanced process tech, 3, 5, 7nm. 10% advanced packaging and mask making, 10% other. 2020 capex, originally slated at $15B, was over $17B. For context $AMD's entire revenue for 2020 estimated at $9.5B

All this, especially the capex, in line with suggestions Intel will be increasing their use of TSMC fabs, or else AMD making really large increases (or both), but they also project a lot of growth in phones

I expect some inflation for autos and appliances as production is limited by the silicon shortage. Not like these fabs want to build more capacity at these nodes.

They still plan on continuing to expand in China, but a reset on the leading edge.

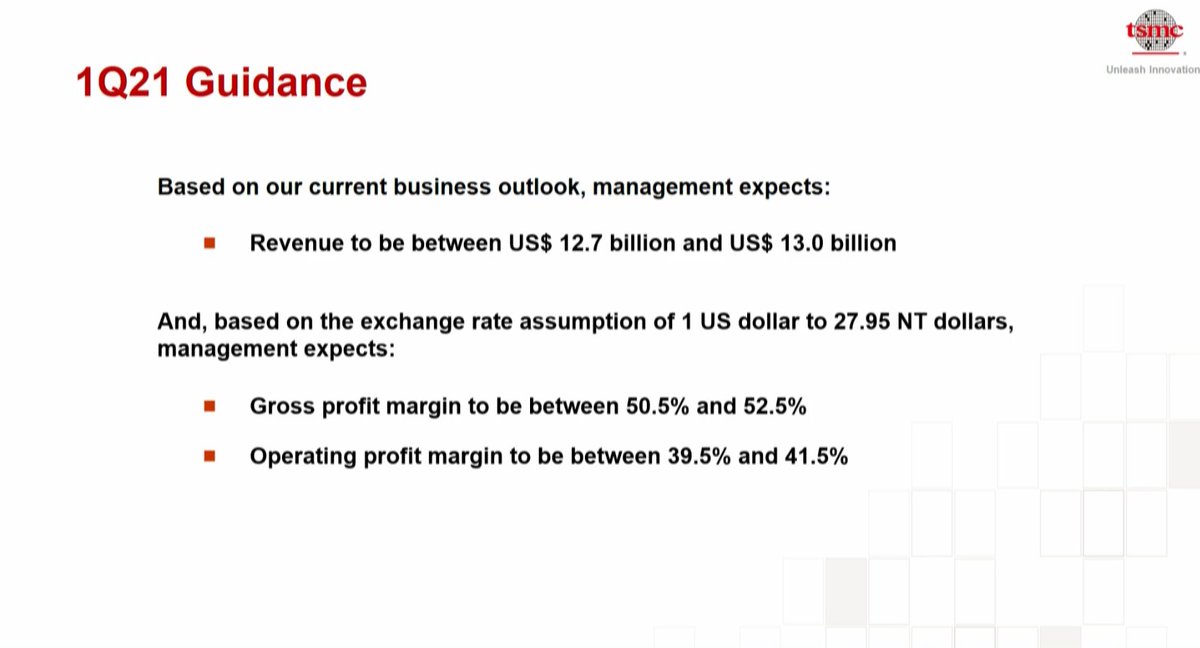

TSMC 4Q earnings remained strong on \u201cextremely high\u201d UTR and some shipments will land 1Q. 1Q21 guided +1% QoQ midpoint, 2021 growing mid-teens USD. Capex up huge $17.2bn to 25-28bn in \u201921, and now expect LT growth of 10-15% CAGR in \u201820-25 vs before 5-10% CAGR....

— cyw60 (@cyw60) January 14, 2021

More from Finance

Thread Best books recommendation by one of best investor I knew @insharebazaar (Virtually)

He grab many multibagger stocks and His style also unique(1st Seen interview in @TraderHarneet's YT Channel)

He follow Simple process

Young Intelligent Investor who also appeared in ET

1. One Up On Wall Street

2. Rich Dad Poor Dad

Access here : https://t.co/UWOCF732z6

3. The Unusual Billionaires

4. Trading in the Zone

https://t.co/G7mqVPtEM0

5. Market Wizards

6. The Intelligent Investor

https://t.co/yPKBzYyPAl

7. The Five Rules for Successful Stock Investing

8. Reminiscences of a Stock Operator

https://t.co/PiioB3hdHP

He grab many multibagger stocks and His style also unique(1st Seen interview in @TraderHarneet's YT Channel)

He follow Simple process

Young Intelligent Investor who also appeared in ET

1. One Up On Wall Street

2. Rich Dad Poor Dad

Access here : https://t.co/UWOCF732z6

3. The Unusual Billionaires

4. Trading in the Zone

https://t.co/G7mqVPtEM0

5. Market Wizards

6. The Intelligent Investor

https://t.co/yPKBzYyPAl

7. The Five Rules for Successful Stock Investing

8. Reminiscences of a Stock Operator

https://t.co/PiioB3hdHP

You May Also Like

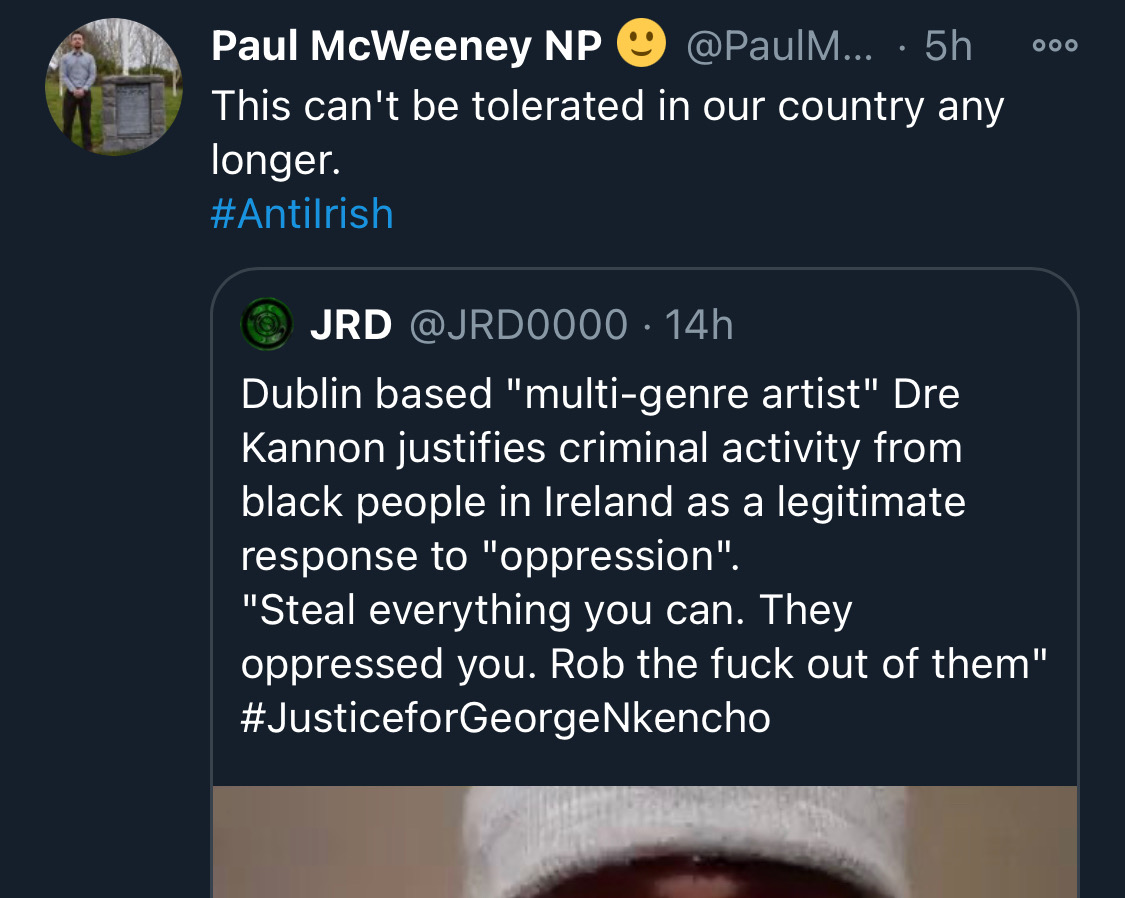

Fake chats claiming to be from the Irish African community are being disseminated by the far right in order to suggest that violence is imminent from #BLM supporters. This is straight out of the QAnon and Proud Boys playbook. Spread the word. Protest safely. #georgenkencho

There is co-ordination across the far right in Ireland now to stir both left and right in the hopes of creating a race war. Think critically! Fascists see the tragic killing of #georgenkencho, the grief of his community and pending investigation as a flashpoint for action.

Across Telegram, Twitter and Facebook disinformation is being peddled on the back of these tragic events. From false photographs to the tactics ofwhite supremacy, the far right is clumsily trying to drive hate against minority groups and figureheads.

Declan Ganley’s Burkean group and the incel wing of National Party (Gearóid Murphy, Mick O’Keeffe & Co.) as well as all the usuals are concerted in their efforts to demonstrate their white supremacist cred. The quiet parts are today being said out loud.

The best thing you can do is challenge disinformation and report posts where engagement isn’t appropriate. Many of these are blatantly racist posts designed to drive recruitment to NP and other Nationalist groups. By all means protest but stay safe.

There is co-ordination across the far right in Ireland now to stir both left and right in the hopes of creating a race war. Think critically! Fascists see the tragic killing of #georgenkencho, the grief of his community and pending investigation as a flashpoint for action.

Across Telegram, Twitter and Facebook disinformation is being peddled on the back of these tragic events. From false photographs to the tactics ofwhite supremacy, the far right is clumsily trying to drive hate against minority groups and figureheads.

Be aware, the images the #farright are sharing in the hopes of starting a race war, are not of the SPAR employee that was punched. They\u2019re older photos of a Everton fan. Be aware of the information you\u2019re sharing and that it may be false. Always #factcheck #GeorgeNkencho pic.twitter.com/4c9w4CMk5h

— antifa.drone (@antifa_drone) December 31, 2020

Declan Ganley’s Burkean group and the incel wing of National Party (Gearóid Murphy, Mick O’Keeffe & Co.) as well as all the usuals are concerted in their efforts to demonstrate their white supremacist cred. The quiet parts are today being said out loud.

There is a concerted effort in far-right Telegram groups to try and incite violence on street by targetting people for racist online abuse following the killing of George Nkencho

— Mark Malone (@soundmigration) January 1, 2021

This follows on and is part of a misinformation campaign to polarise communities at this time.

The best thing you can do is challenge disinformation and report posts where engagement isn’t appropriate. Many of these are blatantly racist posts designed to drive recruitment to NP and other Nationalist groups. By all means protest but stay safe.