How Does Zero Cost EMI work?

What is the catch here? How do Companies involved make money here?

A Thread🧵👇

Please "RT" if you like the thread.

The catch is - it is more to do with marketing and sales than finance.

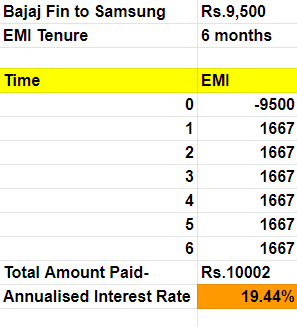

Samsung will cut out a deal with Bajaj Finance. It will provide a 5% discount to Bajaj Fin. So Bajaj Fin will pay Samsung Rs.9500 while it will receive 10k from the customer

Here comes the Cash Flow Wizardry:

As months pass by, Bajaj receives EMIs, the outstanding amount decreases and so does the interest on it. It deploys these EMIs to give another loan and so on. On annualized basis, it earns 19.44% !!

More from Finance

Buffett's letters taught me more about investing than any business school ever could.

Even after investing for 14 years, I uncover new insights every time I reread his letters.

Recently, I reread his letters from 1977 to 2020 for a third time.

Here are my key insights:

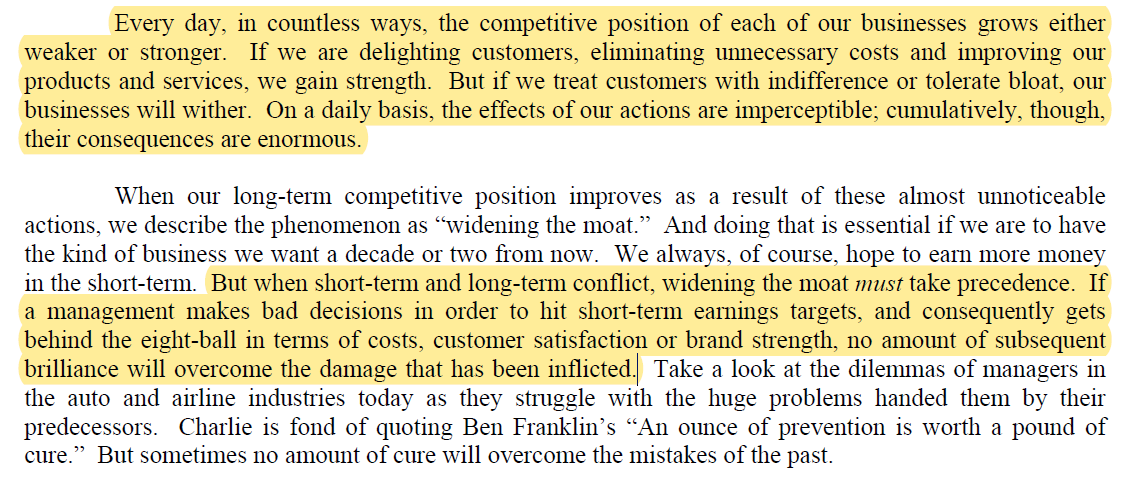

1. Moat is NEVER stagnant

A company's competitive position either grows stronger or weaker each day.

Widening the moat must always take precedence over short-term targets.

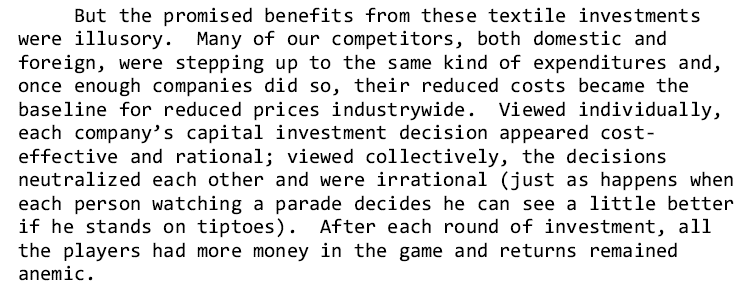

2. Commodity businesses

A business without moat will have its returns competed away.

Regardless of improvement, your competitors will quickly copy your advantage away.

Where returns on capital is dismal, reinvestment will only destroy value.

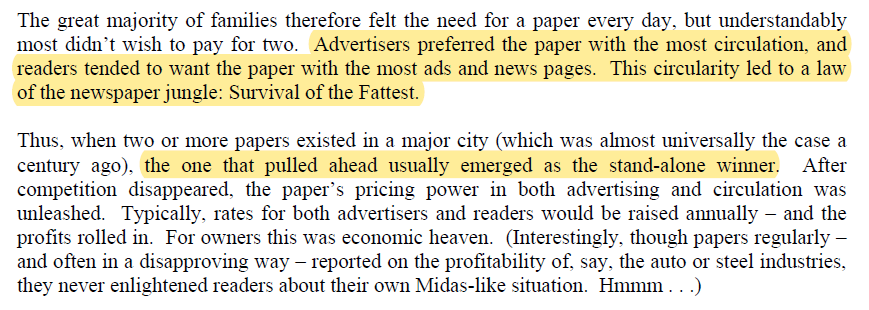

3. The flywheel effect

Buffett was preaching about the flywheel effect before it became cool.

Back then, newspapers were similar to today's platform businesses like Amazon, Meta, and App Store.

More readers beget more advertisers beget more readers.

4. Operating leverage

Companies with high fixed costs and low variable costs will see earnings rise faster than revenue.

However, it cuts both ways.

It becomes a disaster when revenue is declining.

Check out my article on how operating leverage works: https://t.co/Nv747oBAK0

Even after investing for 14 years, I uncover new insights every time I reread his letters.

Recently, I reread his letters from 1977 to 2020 for a third time.

Here are my key insights:

1. Moat is NEVER stagnant

A company's competitive position either grows stronger or weaker each day.

Widening the moat must always take precedence over short-term targets.

2. Commodity businesses

A business without moat will have its returns competed away.

Regardless of improvement, your competitors will quickly copy your advantage away.

Where returns on capital is dismal, reinvestment will only destroy value.

3. The flywheel effect

Buffett was preaching about the flywheel effect before it became cool.

Back then, newspapers were similar to today's platform businesses like Amazon, Meta, and App Store.

More readers beget more advertisers beget more readers.

4. Operating leverage

Companies with high fixed costs and low variable costs will see earnings rise faster than revenue.

However, it cuts both ways.

It becomes a disaster when revenue is declining.

Check out my article on how operating leverage works: https://t.co/Nv747oBAK0