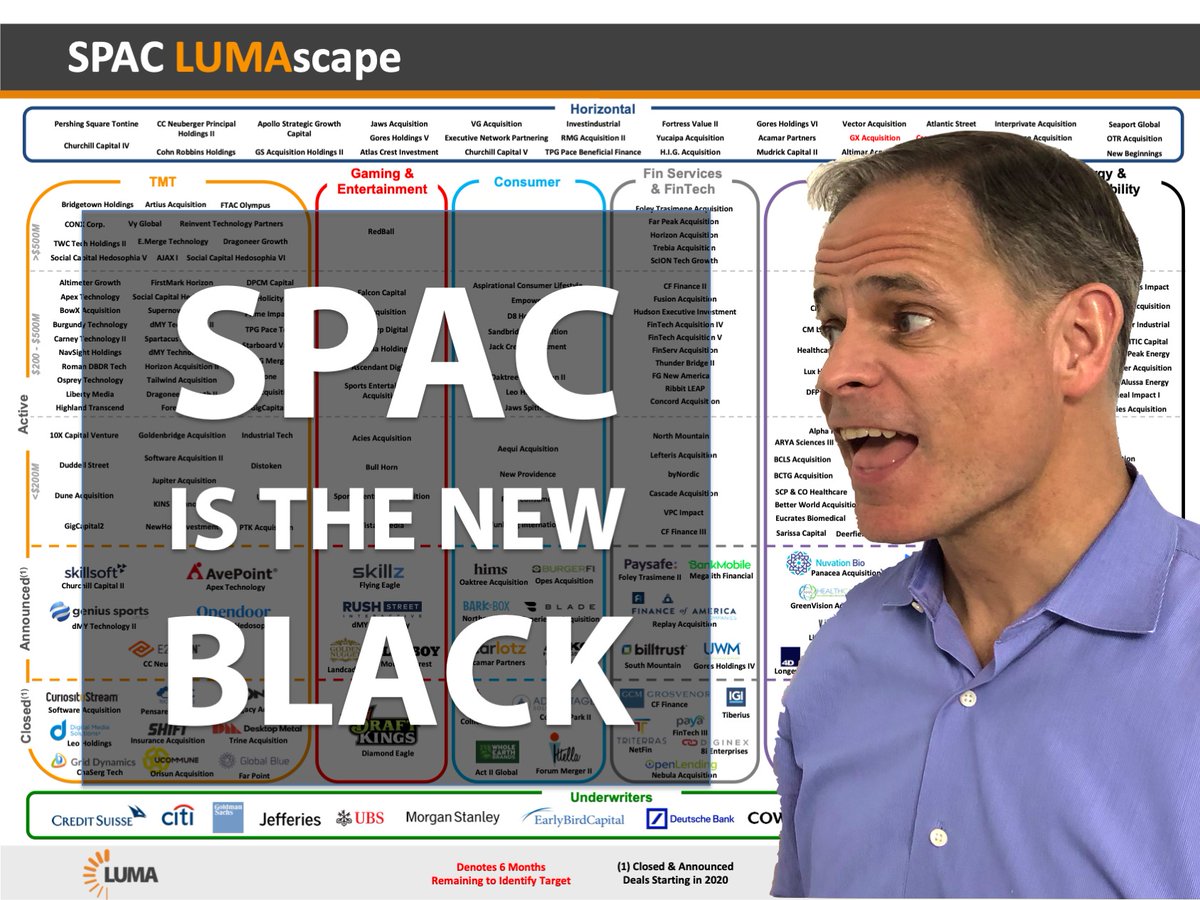

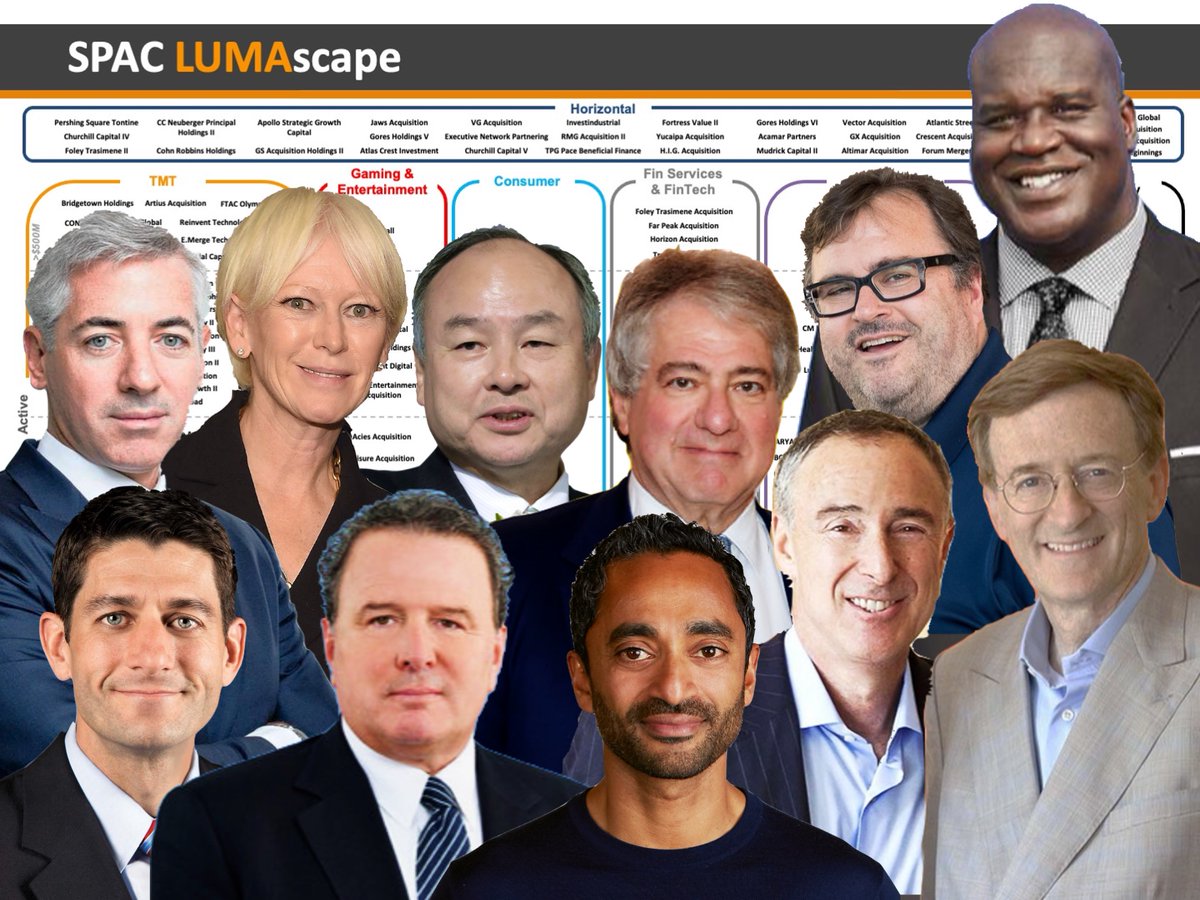

SPAC IS THE NEW BLACK: SPACs (Special Purpose Acquisition Companies) are all the rage these days. In this thread, I want to say a few things about SPACs that I learned in my research of the market. 1/15

More from Business

Facebook originally a CIA program called "LifeLog".

LifeLog, via DARPA, terminated on Feb 4th, 2004.

Facebook was launched on Feb 4th, 2004.

Many of the LifeLog team became execs at FB.

Zuckerberg is a figurehead.

CIA allowed Cambridge to help Trump win

https://t.co/enzOXDCogV

Pentagon Kills LifeLog

LifeLog, via DARPA, terminated on Feb 4th, 2004.

Facebook was launched on Feb 4th, 2004.

Many of the LifeLog team became execs at FB.

Zuckerberg is a figurehead.

CIA allowed Cambridge to help Trump win

https://t.co/enzOXDCogV

Project: Lifelog

— Robert Horan (@Robby12692) December 13, 2018

Started by DARPA in 1999, the goal of Lifelog was to create a database on civilians without their knowledge, and track everything they do.

The project "ended" on Feb 4th, 2004.

Facebook began the exact same day.

The CIA funneled tens of millions into Facebook. pic.twitter.com/r7hwF0v9kh

Pentagon Kills LifeLog

You May Also Like

Funny, before the election I recall lefties muttering the caravan must have been a Trump setup because it made the open borders crowd look so bad. Why would the pro-migrant crowd engineer a crisis that played into Trump's hands? THIS is why. THESE are the "optics" they wanted.

This media manipulation effort was inspired by the success of the "kids in cages" freakout, a 100% Stalinist propaganda drive that required people to forget about Obama putting migrant children in cells. It worked, so now they want pics of Trump "gassing children on the border."

There's a heavy air of Pallywood around the whole thing as well. If the Palestinians can stage huge theatrical performances of victimhood with the willing cooperation of Western media, why shouldn't the migrant caravan organizers expect the same?

It's business as usual for Anarchy, Inc. - the worldwide shredding of national sovereignty to increase the power of transnational organizations and left-wing ideology. Many in the media are true believers. Others just cannot resist the narrative of "change" and "social justice."

The product sold by Anarchy, Inc. is victimhood. It always boils down to the same formula: once the existing order can be painted as oppressors and children as their victims, chaos wins and order loses. Look at the lefties shrieking in unison about "Trump gassing children" today.

Funny there are those who think these migrant caravans were a FANTASTIC idea that's going to take the immigration issue away from you.

— Brian Cates (@drawandstrike) November 26, 2018

Like several weeks watching a rampaging horde storm the fences & throw rocks at our border patrol agents & getting gassed = great optics!

This media manipulation effort was inspired by the success of the "kids in cages" freakout, a 100% Stalinist propaganda drive that required people to forget about Obama putting migrant children in cells. It worked, so now they want pics of Trump "gassing children on the border."

There's a heavy air of Pallywood around the whole thing as well. If the Palestinians can stage huge theatrical performances of victimhood with the willing cooperation of Western media, why shouldn't the migrant caravan organizers expect the same?

It's business as usual for Anarchy, Inc. - the worldwide shredding of national sovereignty to increase the power of transnational organizations and left-wing ideology. Many in the media are true believers. Others just cannot resist the narrative of "change" and "social justice."

The product sold by Anarchy, Inc. is victimhood. It always boils down to the same formula: once the existing order can be painted as oppressors and children as their victims, chaos wins and order loses. Look at the lefties shrieking in unison about "Trump gassing children" today.