Here’s my thoughts with BTC lending as this cycle heats up. During the previous cycle we saw BTC prices jump from 10,000 to 20,000 in 16 days. This means that if the borrower overcollateralized with an LTV of 50%, their escrow will be liquidated (unless margin is met)...1/

More from Bitcoin

1/9 Bitcoin has performed remarkably these past few weeks despite:

-Most of DeFi falling 50-80%

-CFTC charging BitMEX

-POTUS contracting Covid

-Delayed stimulus talks

-FCA announcing a derivative ban for retail

Why? Let’s see what we can find on-chain

2/9 Bitcoin’s Realized Cap has been steadily increasing just as it did before the 2017 bull market took off. If it continues as it did in 2017, 2021 should be an interesting year.

https://t.co/nqgX7vTMDV

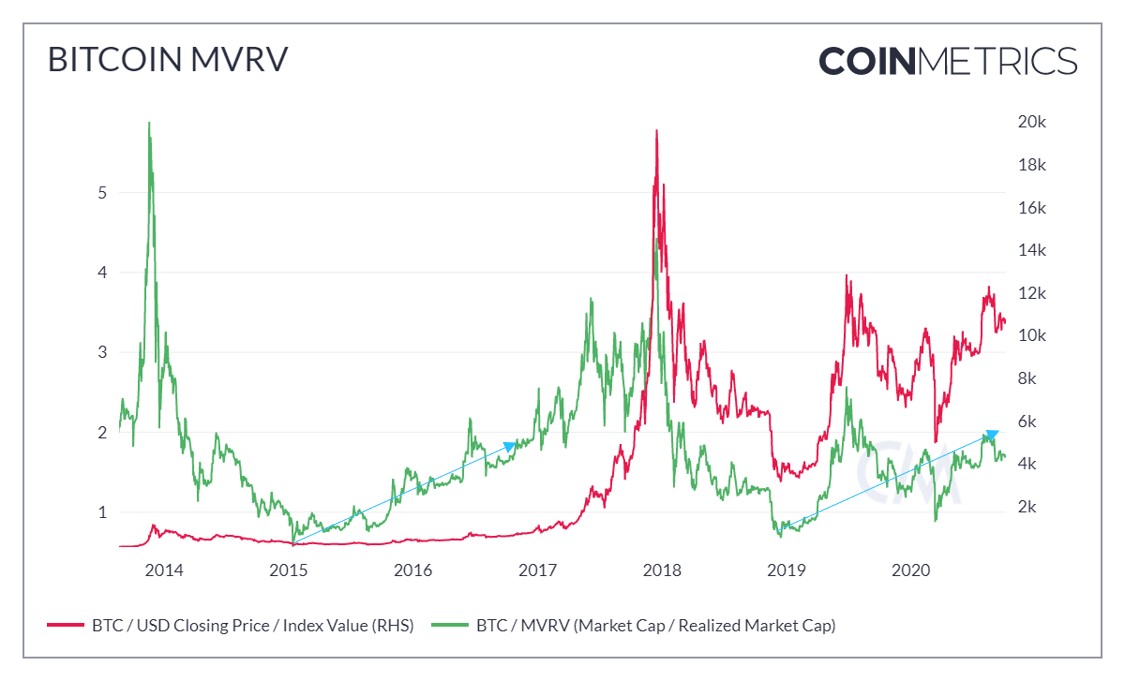

3/9 Bitcoin MVRV, whilst more volatile this market cycle, is also is holding the same trajectory it did during the 2016/17 bull market

https://t.co/jadbn6nCOB

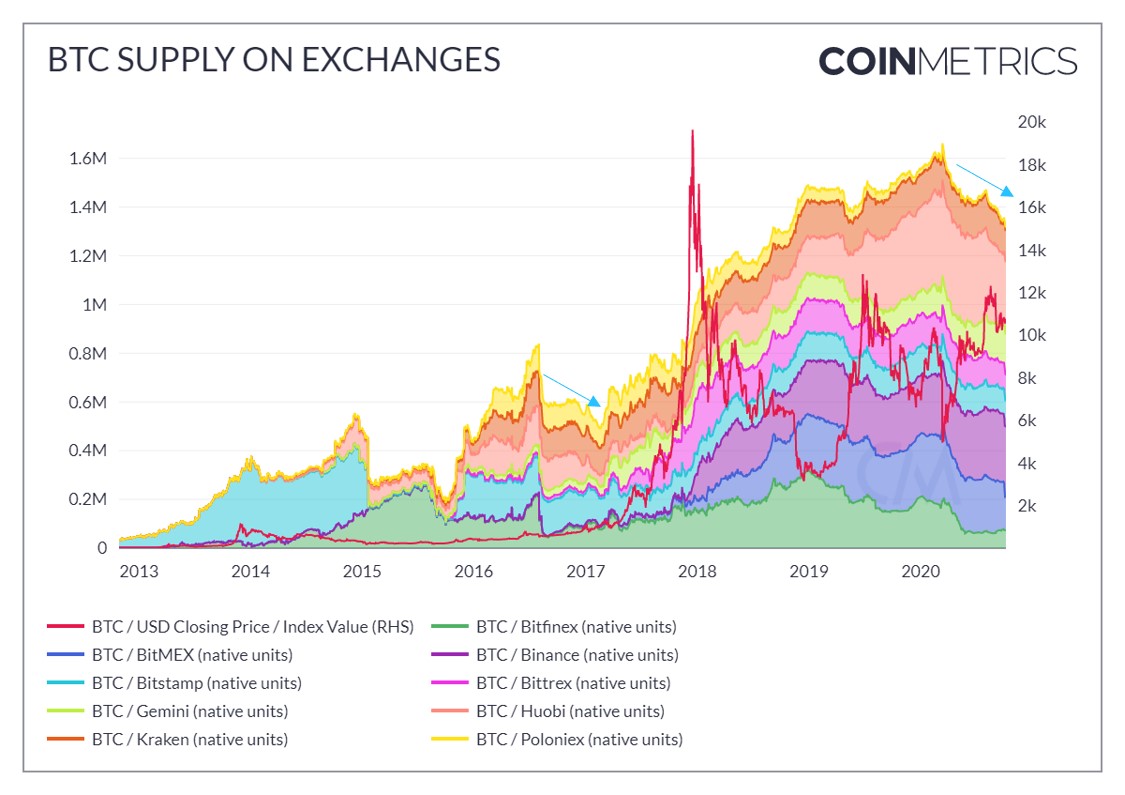

4/9 Looking at the supply of Bitcoin on exchanges is a good indication as to whether or not users are increasing trading activity, or increasing hodl activity. With supply reducing it looks like the tendency recently has been driven by hodlers

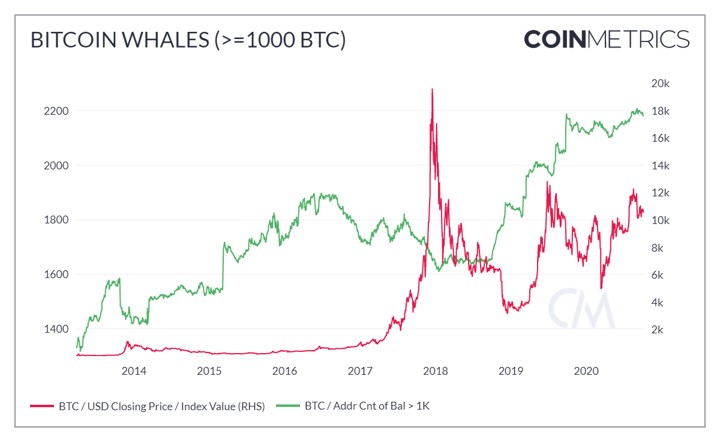

5/9 Despite the recent volatility, the number of Bitcoin whales continues to increase, indicating the growing number of large holders that have positive expectations for the future of Bitcoin

-Most of DeFi falling 50-80%

-CFTC charging BitMEX

-POTUS contracting Covid

-Delayed stimulus talks

-FCA announcing a derivative ban for retail

Why? Let’s see what we can find on-chain

2/9 Bitcoin’s Realized Cap has been steadily increasing just as it did before the 2017 bull market took off. If it continues as it did in 2017, 2021 should be an interesting year.

https://t.co/nqgX7vTMDV

3/9 Bitcoin MVRV, whilst more volatile this market cycle, is also is holding the same trajectory it did during the 2016/17 bull market

https://t.co/jadbn6nCOB

4/9 Looking at the supply of Bitcoin on exchanges is a good indication as to whether or not users are increasing trading activity, or increasing hodl activity. With supply reducing it looks like the tendency recently has been driven by hodlers

5/9 Despite the recent volatility, the number of Bitcoin whales continues to increase, indicating the growing number of large holders that have positive expectations for the future of Bitcoin

1/ #Bitcoin FUD-busting time!

claim: bitcoin ownership is heavily concentrated.

@business published an article claiming "2% of accounts control 95% of all Bitcoin" 🤣

truth: the facts, my friends, simple don't line up. let's dive in!

2/ interrogating on-chain addresses is tricky.

address =/ account.

one person can control multiple addresses.

one address can hold bitcoin belonging to multiple ppl.

exchanges and trading firms will have addresses with large balances that represent client funds.

3/ the fine folks @glassnode published an excellent analysis of on-chain address balances in January

the ownership distribution of bitcoin among wallets is actually much more diverse than one might expect.

full piece here:

https://t.co/n5IdIQdNoA

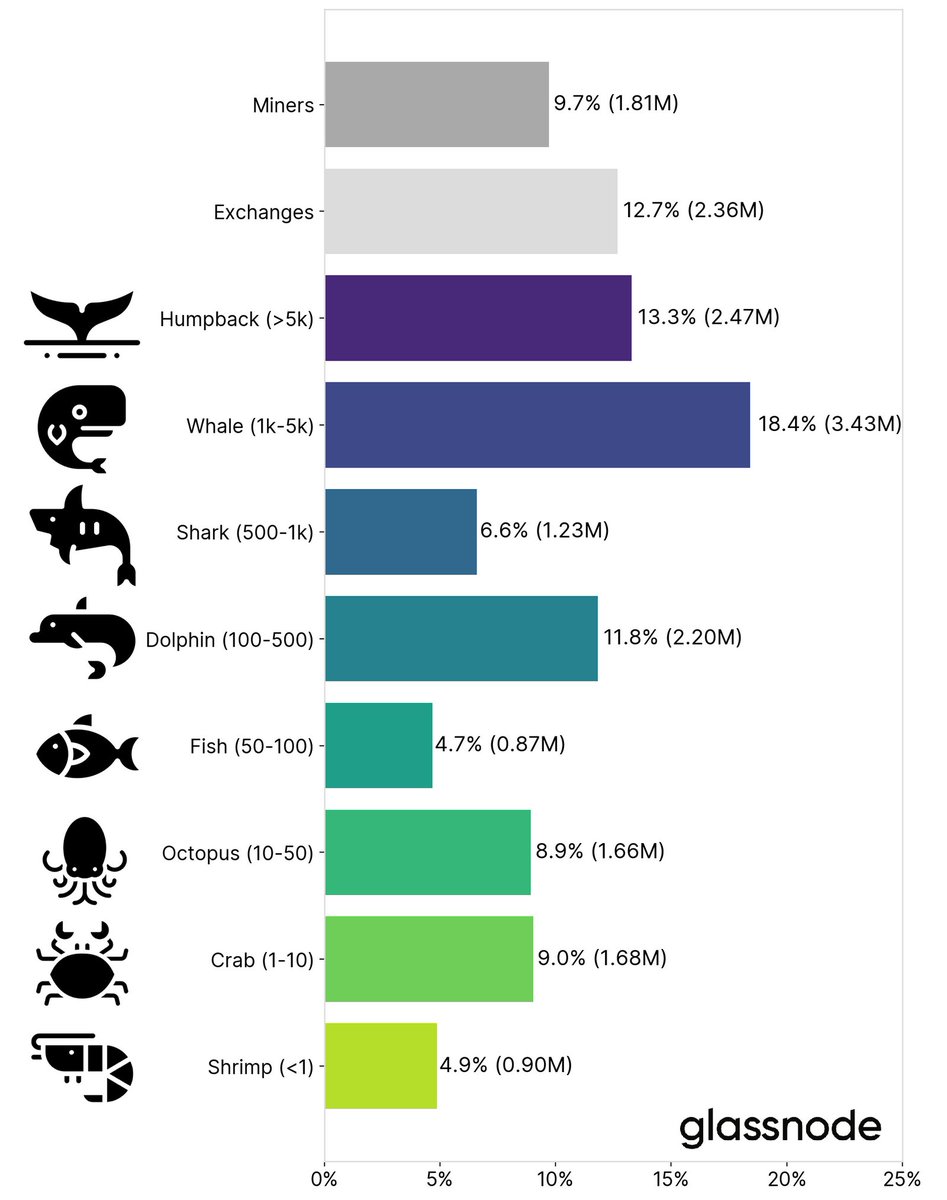

4/ 31% of BTC is held in addresses not identified as exchange wallets.

these are likely institutions, funds, custodians, and OTC desks.

our analysis at @CoinSharesCo indicates >15% of all bitcoin is held in third party custody, including @coinbase and our own @KomainuCustody

5/ in fact, between asset managers @Grayscale ($36B in BTC) and our @xbtprovider ($4B in BTC), 4% of bitcoin is locked up by fund providers and asset managers!

our @CoinSharesCo research team publishes an EXCELLENT weekly report on fund flows and AUMs -

claim: bitcoin ownership is heavily concentrated.

@business published an article claiming "2% of accounts control 95% of all Bitcoin" 🤣

truth: the facts, my friends, simple don't line up. let's dive in!

2/ interrogating on-chain addresses is tricky.

address =/ account.

one person can control multiple addresses.

one address can hold bitcoin belonging to multiple ppl.

exchanges and trading firms will have addresses with large balances that represent client funds.

3/ the fine folks @glassnode published an excellent analysis of on-chain address balances in January

the ownership distribution of bitcoin among wallets is actually much more diverse than one might expect.

full piece here:

https://t.co/n5IdIQdNoA

4/ 31% of BTC is held in addresses not identified as exchange wallets.

these are likely institutions, funds, custodians, and OTC desks.

our analysis at @CoinSharesCo indicates >15% of all bitcoin is held in third party custody, including @coinbase and our own @KomainuCustody

5/ in fact, between asset managers @Grayscale ($36B in BTC) and our @xbtprovider ($4B in BTC), 4% of bitcoin is locked up by fund providers and asset managers!

our @CoinSharesCo research team publishes an EXCELLENT weekly report on fund flows and AUMs -