I will try to avoid redundancy from my earlier post in this thread. So, you may want to take a look at this one as well.

https://t.co/4tsBB8JOuI

1. Wide Manufacturing Base effect

Prince has a strong & growing manufacturing plants presence in the country which leads to one of the lowest freight cost in the industry. Finolex has the lowest cost most likely because of their backward integration into PVC resin.

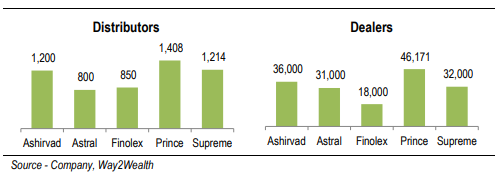

2 Distribution Network: Prince has highest no. of Dist. and Dealers among its peers.

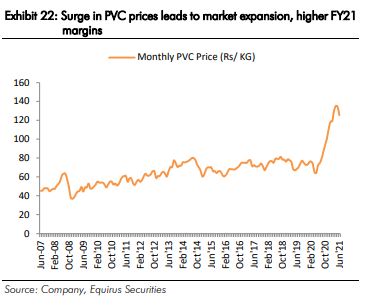

3. Continuing on the high distributors reach, the industry has never seen such a surge in the PVC prices which has led to industry consolidation with organized players gaining market share. And the player with greater reach/product availability is likely benefit more.

4. Prince also has one of the highest no. of SKU’s at 7,200 only next to Supreme (8,774).

5. Prince tie-up with Lubrizol is a huge differentiator for the brand and CPVC sales and is among the first choice among builders. The FlowGuard Plus brand enjoys good recall and acceptability leading to some pricing power

6. (Note: Currently Ashirvad & Prince have license to manufacture Lubrizol’s “Flowguard” brand)

7. Since raw material i.e., PVC resin has a high volatility it is imperative to ensure stable supply (note: India majorly depends on imports). Prince has a stable supply of good quality PVC resin from Lubrizol which they produce domestically. Lubrizol in a JV with Grasim

8. is increasing its capacity to become the largest producer in the country and with this Lubrizol becomes the only company in India with end-to-end CPVC capability. Whereas other players may be depended on imports and face supply disruptions.

9. Prince also differentiates itself by collaborating with “Tooling Holland”, a global leader in the Intl. plastic injection molding based in Netherlands for its technical knowhow which helps the co. offer high quality products along with greater productivity and cost efficiency.

10. Prince and Apollo has been growing at industry leading pace along with Astral and Ashirvad (Low base)

11. Here is the graph showing the Ad spend as a % of sales. Prince has been getting more aggressive and the management says that they see it as an investment and not expense.

12. Looking at the realization/kg - Even here it is only behind Ashirvad & Astral

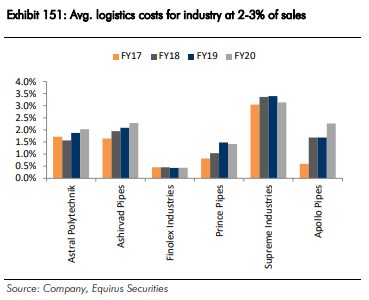

13. This comparative analysis of Key players provides concise and great information. Prince has 100% rev. from pipes & fittings. Overall its very competitive against Top Leaders.

14. After qualitative & quantitative analysis last comes valuations. Since its established that the pipes market is growing at 11-12% CAGR FY21-25E.

The idea was to look for a company offering value and faster growth prospects.

15. And here I found Prince Pipes and Apollo Pipes giving better value against the no brainer Astral.

And given the aggressive growth intent, management execution along with improving corporate governance, manufacturing capabilities and also considering the strong OCF post

16. Telangana plant (52K TPA with Asset TO 2.5x-3x) I find Prince Pipes more appealing which ticks all the boxes as noticed in above facts. Additionally, it is introducing premium products and increasing higher margin products capacity.

17. Prince is now the 5th largest organized player and I can see it breaking into Top 4. However, displacing Ashirvad Pipes or Astral is not the intention nor its even in the equation. And one doesn’t even need to aim for that given the overall expected industry growth.

18. P.S – Others may find the Apollo brand more appealing and there is no right or wrong here. Even I admire and respect the management.

Few other things to note:

- Supreme Ind: I find it too diversified

- Finolex: Backward integration into commodity impacts margins adversely

19. Prince is trying to expand in East region with a unique asset light strategy via outsourcing mainly for non-pressure PVC pipes. However, in Mid-Long term it will look to have its own capabilities in the region.

20. I find all key attributes for success tick for

#PrincePipes👑

- Pricing Power☑️

- Differentiated products☑️

- Decentralized Manufacturing☑️

- Stable Good quality RM (PVC) supply☑️

- Strong Distribution Network☑️

Disclosure: I am invested into Prince Pipes from lower levels and may have a biased view.