2/

A THREAD

Topic: HOW TO TRADE IN RISING PREMIUMS SCENARIO

Option sellers specially Straddle sellers feel that rising premiums give them excellent opportunity to make easy money. So what they are seeing is the theta aspect of options & ignoring the delta/gamma/vega forces.

1/

2/

3/

4/

There will also be very few instances when premiums don't fall till expiry day. So with each delta move the cost of holding a straddle gets accumulated & pressure keeps mounting for the stubborn option sellers.

5/

Compulsive straddle sellers can keep a close SL & do quick scalping. But such profits don't give you much satisfaction, as speculation element is high in such trades.

6/

There are many option strategies like Ratios, Ladder, even far OTM naked/spread selling which can give good opportunity to take advantage.

7/

8/

9/

If one can find a way to forsee how volatility or direction is going to play out, then it's a different ball game altogether.

10/

Patience is the key & being ready to let go of some premium decay. Don't get caught up in FOMO.

11/

In this scenario, we could have sold inflated OTM calls, which were not falling.

12/

When market bounced back calls also fell at first. If market starts rising, we can start neutralizing our position.

13/

• If IVs are falling then sell otm puts

• If IVs are increasing then buy higher delta calls to make Call ratios

The above example is when we want to trade directional & take advantage of rising premiums.

14/

More from Sarang Sood

Since IRONFLY is the flavour these days, sharing my own thread. It has GREEKS incorporated which automatically reduces wing size & risk.

P.S. No one specifically invented ironfly & it's adjustments. A good trader can figure it out on his own. I've been doing it on & off for yrs.

P.S. No one specifically invented ironfly & it's adjustments. A good trader can figure it out on his own. I've been doing it on & off for yrs.

THREAD ON IRONFLY

— Sarang Sood (@SarangSood) December 12, 2020

These days the most preferred strategy for option sellers due to improved margins is IRONFLY. It's essentially a short straddle with long strangle. Long strangle acting as 'WINGS', which help in capping the unlimited risk associated with a short straddle.(1/n)

Low VIX doesn't necessarily mean ideal time for option buyers. If premiums aren't falling consistently during the day in low VIX, it usually gives those small delta & IV spikes, just enough to irritate both option buyers & sellers. Same happens when VIX is ultra high.

@SarangSood Sarang bhai according to you what number of vix is ideal for option buyers and what is that for option sellers? And is there any common number which is ideal for both?

— Dhaval bhatt (@Dhavalb55011726) July 14, 2021

More from Optionslearnings

A THREAD ON @SarangSood

Decoded his way of analysis/logics for everyone to easily understand.

Have covered:

1. Analysis of volatility, how to foresee/signs.

2. Workbook

3. When to sell options

4. Diff category of days

5. How movement of option prices tell us what will happen

1. Keeps following volatility super closely.

Makes 7-8 different strategies to give him a sense of what's going on.

Whichever gives highest profit he trades in.

2. Theta falls when market moves.

Falls where market is headed towards not on our original position.

3. If you're an options seller then sell only when volatility is dropping, there is a high probability of you making the right trade and getting profit as a result

He believes in a market operator, if market mover sells volatility Sarang Sir joins him.

4. Theta decay vs Fall in vega

Sell when Vega is falling rather than for theta decay. You won't be trapped and higher probability of making profit.

Decoded his way of analysis/logics for everyone to easily understand.

Have covered:

1. Analysis of volatility, how to foresee/signs.

2. Workbook

3. When to sell options

4. Diff category of days

5. How movement of option prices tell us what will happen

1. Keeps following volatility super closely.

Makes 7-8 different strategies to give him a sense of what's going on.

Whichever gives highest profit he trades in.

I am quite different from your style. I follow the market's volatility very closely. I have mock positions in 7-8 different strategies which allows me to stay connected. Whichever gives best profit is usually the one i trade in.

— Sarang Sood (@SarangSood) August 13, 2019

2. Theta falls when market moves.

Falls where market is headed towards not on our original position.

Anilji most of the time these days Theta only falls when market moves. So the Theta actually falls where market has moved to, not where our position was in the first place. By shifting we can come close to capturing the Theta fall but not always.

— Sarang Sood (@SarangSood) June 24, 2019

3. If you're an options seller then sell only when volatility is dropping, there is a high probability of you making the right trade and getting profit as a result

He believes in a market operator, if market mover sells volatility Sarang Sir joins him.

This week has been great so far. The main aim is to be in the right side of the volatility, rest the market will reward.

— Sarang Sood (@SarangSood) July 3, 2019

4. Theta decay vs Fall in vega

Sell when Vega is falling rather than for theta decay. You won't be trapped and higher probability of making profit.

There is a difference between theta decay & fall in vega. Decay is certain but there is no guaranteed profit as delta moves can increase cost. Fall in vega on the other hand is backed by a powerful force that sells options and gives handsome returns. Our job is to identify them.

— Sarang Sood (@SarangSood) February 12, 2020

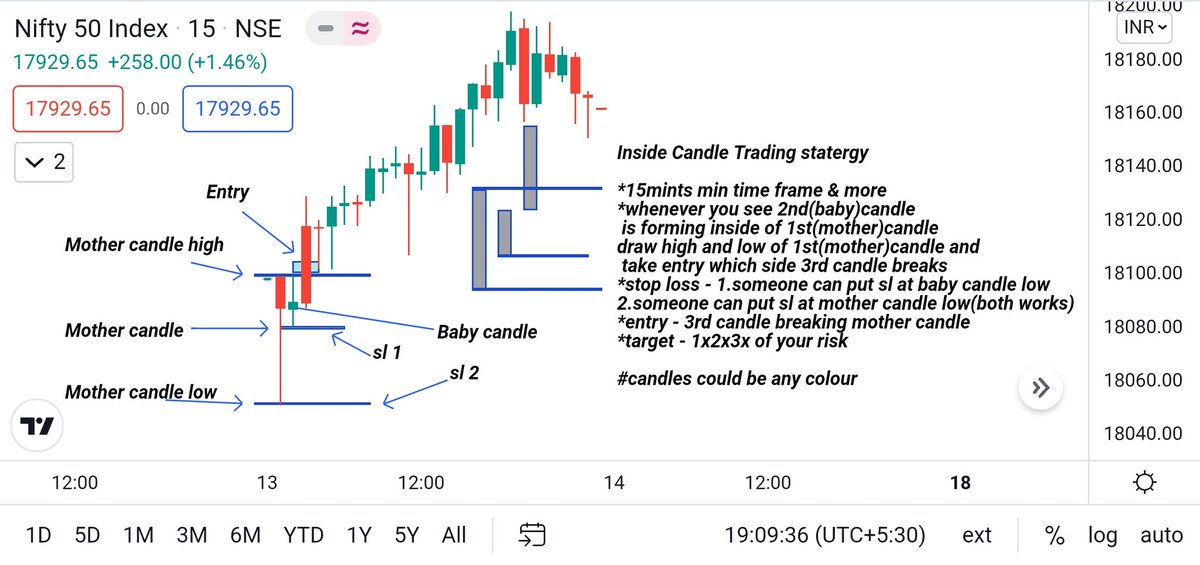

As committed here goes the 2nd "Inside Candle" strategy:-

Queries can be posted on comments, video will take some time to come.

Want market influence to circulate it to reach max audiences.

@DillikiBiili @AnilSinghvi_ @anilbalaji11 @bankniftydoctor @brahmesh https://t.co/SmCZMMkBzV

Inside Candle Trading statergy

*15mints min time frame & more

*whenever you see 2nd(baby)candle

is forming inside of 1st(mother)candle

draw high and low of 1st(mother)candle and

take entry which side 3rd candle breaks

*stop loss - 1.someone can put sl at baby candle low

2.someone can put sl at mother candle low(both works)

*entry - 3rd candle breaking mother candle

*target - 1x2x3x of your risk

#candles could be any colour

Queries can be posted on comments, video will take some time to come.

Want market influence to circulate it to reach max audiences.

@DillikiBiili @AnilSinghvi_ @anilbalaji11 @bankniftydoctor @brahmesh https://t.co/SmCZMMkBzV

I will give free 40 point #banknifty and 20 point # nifty strategy .

— SG (@GhoshSubhag) October 30, 2021

Don't pay me anything, just 1 like or retweet is sufficient \U0001f64f https://t.co/3R1PZZSK84

Inside Candle Trading statergy

*15mints min time frame & more

*whenever you see 2nd(baby)candle

is forming inside of 1st(mother)candle

draw high and low of 1st(mother)candle and

take entry which side 3rd candle breaks

*stop loss - 1.someone can put sl at baby candle low

2.someone can put sl at mother candle low(both works)

*entry - 3rd candle breaking mother candle

*target - 1x2x3x of your risk

#candles could be any colour

You May Also Like

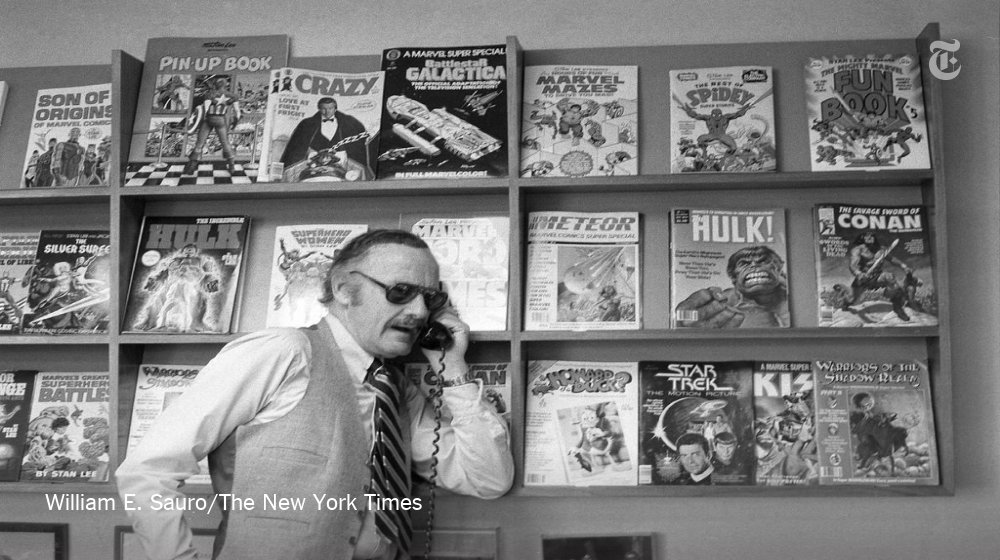

Stan Lee’s fictional superheroes lived in the real New York. Here’s where they lived, and why. https://t.co/oV1IGGN8R6

Stan Lee, who died Monday at 95, was born in Manhattan and graduated from DeWitt Clinton High School in the Bronx. His pulp-fiction heroes have come to define much of popular culture in the early 21st century.

Tying Marvel’s stable of pulp-fiction heroes to a real place — New York — served a counterbalance to the sometimes gravity-challenged action and the improbability of the stories. That was just what Stan Lee wanted. https://t.co/rDosqzpP8i

The New York universe hooked readers. And the artists drew what they were familiar with, which made the Marvel universe authentic-looking, down to the water towers atop many of the buildings. https://t.co/rDosqzpP8i

The Avengers Mansion was a Beaux-Arts palace. Fans know it as 890 Fifth Avenue. The Frick Collection, which now occupies the place, uses the address of the front door: 1 East 70th Street.

Stan Lee, who died Monday at 95, was born in Manhattan and graduated from DeWitt Clinton High School in the Bronx. His pulp-fiction heroes have come to define much of popular culture in the early 21st century.

Tying Marvel’s stable of pulp-fiction heroes to a real place — New York — served a counterbalance to the sometimes gravity-challenged action and the improbability of the stories. That was just what Stan Lee wanted. https://t.co/rDosqzpP8i

The New York universe hooked readers. And the artists drew what they were familiar with, which made the Marvel universe authentic-looking, down to the water towers atop many of the buildings. https://t.co/rDosqzpP8i

The Avengers Mansion was a Beaux-Arts palace. Fans know it as 890 Fifth Avenue. The Frick Collection, which now occupies the place, uses the address of the front door: 1 East 70th Street.