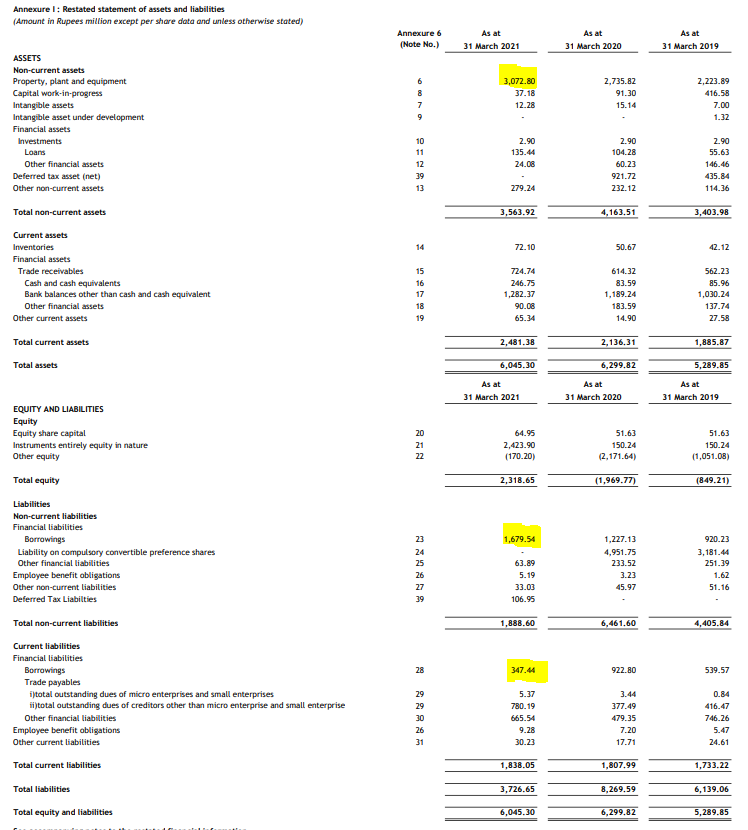

Issue Dates: 4 - 6 August

Issue Size: ₹ 1,211 Crore (400crs Fresh Issue & 811crs OFS)

Mcap at the upper band: 2994crs

Price Band: ₹ 933 - 954

Retail Quota: 10%

Promoter stake to go from 32% to 27% post IPO.

As a dean of a major academic institution, I could not have said this. But I will now. Requiring such statements in applications for appointments and promotions is an affront to academic freedom, and diminishes the true value of diversity, equity of inclusion by trivializing it. https://t.co/NfcI5VLODi

— Jeffrey Flier (@jflier) November 10, 2018