1/ In the Indian healthcare delivery market; the pharmaceuticals market is 20% of the pie. While Hospitals market is 3x that of theirs.

Big opportunity size, however, is it investment-worthy? Let's see.

2/ Before we get into the details:

Do brush up on the different abbreviations associated with the Hospitals & the Pharmaceuticals industry in General, for example ALOS, ARPOB, NABH, etc.

Inpatient (IPD): Need to get hospitalized

Outpatient (OPD): No need to get hospitalized

3/ The hospitals are of basically 3 types:

Primary: For OPD only (no beds), sends to below hospitals for further treatment

Secondary: IPD & OPD in medium-sized general hospitals

Tertiary: Can treat all complex ailments & huge in size, Major listed companies are focused here.

4/ Hospitals can also be classified based on Ownership & management:

Here, the listed companies either are in private or manage hospitals owned by others (Asset light business, due to the very high land prices in metro cities)

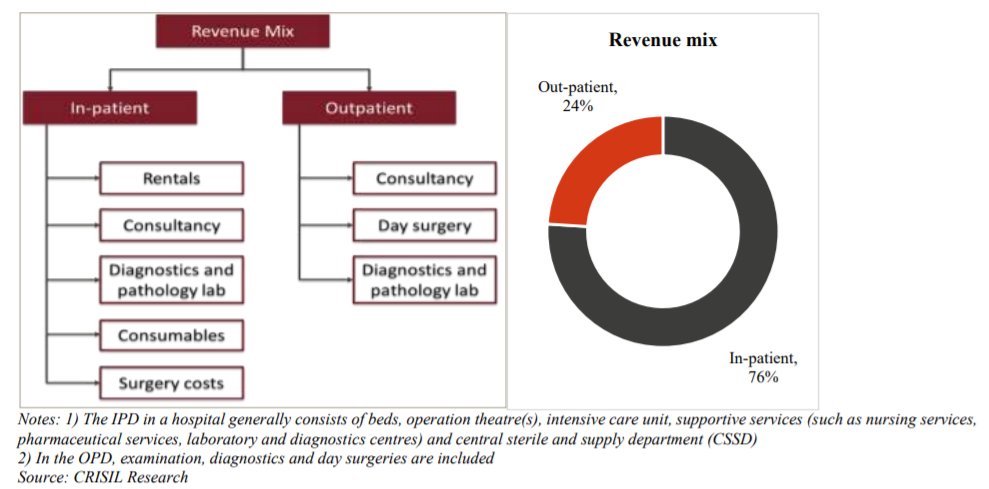

5/ In a normal hospital, The IPD accounts for only 25% of the total volume, however, in value terms is near 76% of rev (Getting hospitalized is expensive!)

This ratio can vary b/w different hospitals depending on the therapies they cater to.

6/ Capital costs: Huge (Gestation period: 7-10 years)

A single bed in a metro city for most listed cos. costs 50 lakhs-1crore/bed

Note that 65-75% of these costs are one-time (Land & Equipment) & expansions in already established hospitals are cheaper at 25-30 lakhs/bed.

7/ Operational costs: Humongous.

Hospitals are open 24x7 no matter if they have patients on not; they should be there staffed & ready to go in case somebody needs them: An accident or a pandemic.

This leads to Huge Fixed costs: does not matter how many patients they have.

8/ Thus, Hospitals are a play on Operating leverage due to such high fixed costs.

All about more patients, more so from higher value therapies like Neuro, renal & IPD (getting more hospitalized)

Keeping a hospital profitable is tough: One has to be a brand in its locality.

9/ Technology continues to be a major disruptor in healthcare services today.

Are Equipment Investments a constant? Mostly yes. leading to consistent maintenance capex

Da Vinci robotic surgical system

128 Slice CT scanner

Digital LINAC Accelerator...

10/ What's the differentiating factor?

Intellectual Capital: Full-time Doctors, Consultants, Student doctors & the support staff

Big Shortage of Specialists in India (seats are much less than required in medical colleges); most prefer to stay in cities.

11/ Even though beds are nowhere near what 🇮🇳 requires, affordability is the issue.

Over 60% of the expenses are from out of pocket, even for others government & private insurers: they continue to squeeze hospitals for lower costs.

Even health insurance premiums are very high.

12/ Additionally, most tertiary hospitals are only present in top cities.

People travel Intra & inter-state; putting a huge burden on these assets.

One of the big reasons most lost money in FY21: due to COVID travelling restrictions.

13/ There are approximately 15 lakh beds in India.

The largest player (Apollo) is not even 1% of the industry; Huge competition.

High fragmentation & very low profitability (max 12-14% ROCEs) indicates Industry needs massive consolidation before it gets attractive.

14/ Another big risk is Government intervention

By way of an active regulatory regime, be it in terms of price control or capping of margins on medicines and implants has been stepped up.

State and Central Healthcare coverage schemes are also impacting industry margins.

15/ Positives:

Pricing power to some extent due to the granularity of the customers & loyalty/Trust that they too most doctors.

However, can get affected by hyper-competition locally. Even Narayana Health had to close one of its hospitals in Bangalore.

https://t.co/fbJvO825wr

16/ Larger hospital brands typically have the

Stronger financial discipline

Negotiating power with suppliers

Better ability to attract medical talent

Greater capital and administrative resources

Vs standalone hospitals

Inorganic way is expected to be the next leg of growth.

17/ What to look for in Hospitals?

ALOS is decreasing (efficiency)

ARPOB is increasing (complex therapies⏫)

Majority of greenfield capex over; more of brownfield going forward & potential higher utilization

Low competition; location check

Adjacencies like diagnostics & Pharmacy

18/ Game of Economies of Scale as the demand is perpetual & still much of India's demand is unmet

“I left England in 1989 and the first patient I did the bypass grafting in Calcutta paid 1.5lk Rs

30 yrs later, we are doing the same operation for less than 1lk.” ~Dr. Devi Shetty

19/ Current scenario:

Hospitals' non-covid sales are just back to pre-covid levels & it looks amazing optically due to the subdued FY21 sales.

Most of the people who deferred elective surgeries due to COVID risk are back; not much has changed on the structural front.

20/ Also, Inter-State travel & Foreign travel (aka. Medical Tourism) will give a boost to sales of most hospitals as they start again gradually.

All of this will be a temporary jump & FY23 might show a more normal year as growth will slow down.

21/ Finally, If a healthcare solution is not affordable, it’s not a solution.

It's a long way to go for this to become a sustainable business; 6-8cr people go below the poverty line every year while paying their healthcare bills. Even after decades of independence, It's sad.

22/ We continue to believe in the entrepreneurs & doctors (current & future) of 🇮🇳

Nevertheless, The logic stops us from allocating a lot into this industry due to the multiple challenges mentioned above.

Don't overpay: Most private deals happen at 10-15x EV/EBITDA.

End.

If you found the thread to be of help, please retweet the 1st tweet 👇 to help us educate more investors.

Also, please give me ideas on what pharmaceutical industry's segment or company do you want me to make my next thread on, in the comments section 😇

https://t.co/o0P4m1VES9

The competitive scenario is not going to fizzle out anytime soon.

3 Hospital IPOs are in line to raise up to 6300crs in the upcoming months:

Cloud Nine

Medanta

Park Group

With moderation in capex, the time is ripe for them to show good ROI and get high valuations. Be careful.