Windlas Biotech IPO notes 💊

'What's in a name? that which we call a rose by any other name would smell as sweet' ~Shakespeare

Hit the 'retweet' & help us educate more investors

A thread 🧵👇

#IPOwithJST

1/ Basics about the IPO 👇

Incorporated in 2001

Fresh Issue of 165crs (50 for capex | 48 for Working capital | 20 for debt payment) + OFS of 237crs (Partially by promoter & PE Tano selling out as the fund tenure is up)

~ Total raise of 402crs

2/ About the company (Not a Biotech company)

A Contract manufacturer for formulation cos. (204 in total) for Indian markets & a small domestic OTC biz

3279 products, 4 plants with 700cr tablets/capsules capacity

Emphasis on chronic (60% of rev) & complex generics (70% of rev)

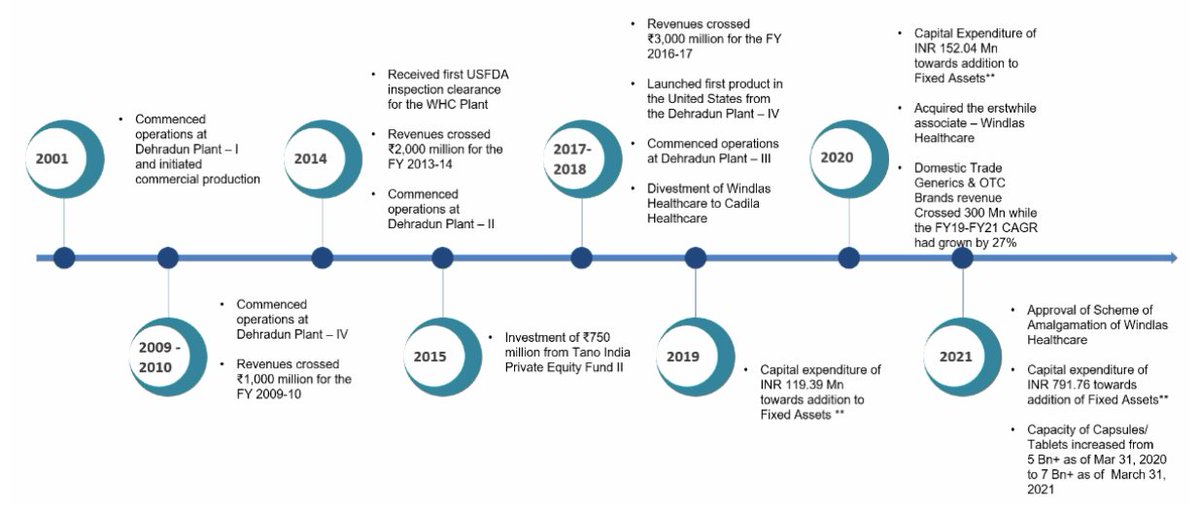

3/ History

Revenues:

FY11 - 100cr 👉 FY14 - 200cr 👉 FY21 - 400cr

Growth is similar to the Indian pharmaceutical sector, not gaining any market share even after increasing products.

Customers include Pfizer, Sanofi India, Eris, Cadila, etc.

4/ Competition: No Moat

400+ organized & 15000 unorganized players in the same space: 2% market share

Some of the things that can drive consolidation: Customers preferring better compliance

However, a single customer usually has 35-40 contract manufacturers for products.