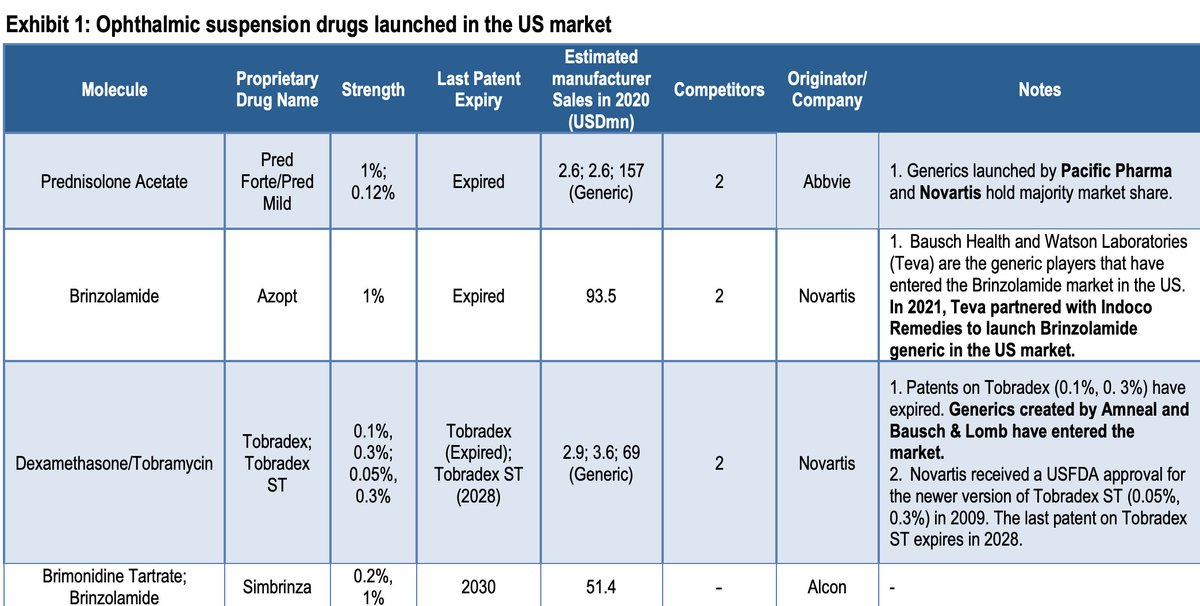

Looking at the incremental opportunity in Ophthalmics:-

Market size is not attractive for the Large Generic companies but for someone like Indoco which has a smalll base in exports business

As per the USFDA’s orange book, for Ophthalmic suspension drugs, only 3 out of 17 molecules have an active patent. Among the 14 molecules that are patent expired, 8 molecules are yet to see generic

competition.

Even for the one’s which have seen generic competition, the competitive intensity is very low and there is space for an additional entrant.. Entrenched players like Novartis, Bausch & Lomb and Abbvie have dominated this market with legacy products for decades.

Indoco Remedies and Sun Pharma are the only Indian generic manufacturers to have successfully won approvals for generic version of Ophthalmic suspensions in the US market. Indoco Remedies has recently launched generic version of Azopt (brinozolamide)

while Sun Pharma also only recently received approval for gLotemax (loteprednol suspension). A break up of the ophthalmic Products launched in the market:

As you can see there are very few generic players in the market due to complexity of manufacturing and small size of the industry

Thesis entails:

1. Strong recovery in Domestic Heavy Acute Portfolio.

2. Hiring a Chief Marketing officer which indicates to something+Changing the logo (signalling)

3. UK & US exports will show disproportionate growth this year due to regulatory issues being solved

4. MR productivity is horribly low, 2.7 lakhs. This can easily go above 3-3.5 Lakhs.

5. Indoco is the fastest growing domestic pharma business this year and they are targeting Sub-Chronic therapy launches.

6. Un-utlised gross block as the company

did capex but couldn't utilize it due to regulatory issues b/w 2017-2019.

7. Co is sitting on substantial operating leverage, and has the potential to do 24%+ ebitda margins in my view. First Q this year they already did 22%.

8. Management guiding to double the Ebitda in next 3