And you can also join our Telegram channel for regular updates – https://t.co/Ekz6I8pDGt (2/n)

Personal Finance 101 – My learning’s about investing

This topic is for everyone, whether you manage your money yourself or through your advisor, it will go a long way in managing your finances.

Do re-tweet & help us educate retail investors (1/n)

And you can also join our Telegram channel for regular updates – https://t.co/Ekz6I8pDGt (2/n)

Term Insurance is the best way to take an insurance cover & probably the only product to buy in life insurance. Make sure u disclose all the necessary information before taking the insurance. Smoking, Alcohol, any pre-existing deceases etc(3/n)

But there are variants of term insurance that you should avoid (4/n)

For a non-smoker born on the 1st Jan 1985 & policy term 39 years (till age 75), the regular premium for a 1-cr term insurance is 22,157 (inclusive of GST) but with returns of premium is 42670 (inclusive of GST). An increase of 20,513 (5/n)

(i) Without GST premium = 42670/118% = 36161

(ii) Premium returned at policy end if nothing happens = 36161*39 = 14,10,280 (7/n)

(iv) In other terms, the policy is only paying u 2.77% on the additional premium u r paying over the regular premium(8/n)

They will advertise it saying instead of paying 22,157 for 39 years (total 8,64,123), pay 48,830 for 10 years (Total 4,88,300 and save 43% premium, but, the trick here is time value of money. (9/n)

(i) If u calculate the present value of both stream of cash flows @ same rate of 6%, Present Value of regular pay (39 years) is 3,51,100 & 4 limited pay (10 years) is 3,80,957. In today’s term, u r paying 29,857 more in limited premium plans(10/n)

Which is why, in most cases you can ignore ULIP’s as well. (20/n)

- Make sure you mention all the necessary information while applying for the cover and not hide any material fact. Smoking, Alcohol, Pre-existing deceases etc. This is a major reason why most claims get rejected. (21/n)

- In case of a claim, Mediclaim will nt settle 100% of the bill amount; there may be items, which the insurance is nt covering, & the same needs 2b paid by u. Have some medical fund in place 4 such contingencies (22/n)

- Make sure you have atleast 6-12 months of your monthly expenses, including you EMIs, kept aside in an liquid fund for any unforeseen eventuality (23/n)

- Always have a goal in mind and define it in money terms, only then you can plan for it. Ex. Buying a house worth 2cr. in March 2030.

- Having a goal also brings in discipline in your investing (24/n)

- Keep you goals realistic (25/n)

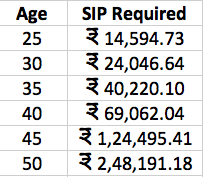

-If u want to accumulate 5 cr. at retirement at 60, below is the SIP u will have 2do depending on when u start, assuming 10% returns

-Starting 10 years later will require u to do 40,000 instead of 14,500 to reach the same goal (26/n)

-Investing golden rule 30:30:30:10. Maximum 30% of ur income as EMI, 30% household expense, 30% Savings & 10% liquid

-Always maintain an Asset Allocation. Don’t invest most of what u have in 1 asset (27/n)

-There is no get rich over night investing strategy. You will have to give it time

-Avoid looking at your portfolio value daily

-Save more (28/n)

- If you don’t understand stock picking, stick to MFs

- Equity is a long-term asset, invest for long term

- Avoid F&O if you don’t understand it

- Investing creates wealth not trading (29/n)

-Debt mutual funds are better over FD’s if you can avoid looking at the daily NAV and give it the 3-5 years you normally give your FDs

-Higher the interest rate offered, higher is the risk

-Fixed income is risk free is a misconception (30/n)

Fixed Income investment strategies (Thread)

— Kirtan A Shah (@KirtanShahCFP) November 20, 2020

Do 're-tweet' & help us reach & benefit investors

It\u2019s a misconception that FD, RBI Bond, PPF etc have no risk. The reason we don\u2019t see the risk in them is because for us, risk ONLY means loss of capital. (1/n)

-Don’t consider the real estate u stay in as a portfolio investment, u will rarely b able 2 use it 2 convert 2 cash when u want it

-RE investments r extremely illiquid

-Rent you receive on housing RE investment is 2% vs 6-7% on commercial real estate (32/n)

-Interesting way to invest in RE - https://t.co/7doPyKWe7D (33/n)

(Thread) With Kotak launching its International REIT Fund of Fund NFO, it is worth revisiting our old thread on Real Estate Investment Trust (#REIT). The Idea is to educate readers on REIT & share our view on the Kotak #NFO

— Kirtan A Shah (@KirtanShahCFP) December 12, 2020

Do \u2018re-tweet\u2019 & help us educate more investors (1/n)

-Don’t consider the Gold jewellery at home as investment if you are not going to sell it when the price increases. Its your emergency fund

-Investments in gold should be in bars and not jewellery. Why spend on making charges? (34/n)

-Best way to invest in Gold is through Gold ETFs & SGB

-More about gold investing - https://t.co/HubxI58OMZ (35/n)

What better day to discuss Gold, isn\u2019t it?

— Kirtan A Shah (@KirtanShahCFP) November 13, 2020

Topic - Physical Gold v/s Digital Gold v/s Gold ETF v/s Sovereign Gold Bond (SGB)

(Thread) \u2013 DO RE-TWEET FOR A LARGER REACH :)

(1/n)

- Always try and utilize your 80C limits to the fullest. If you are in the 30% tax bracket, you directly save 1,50,000 * 30% = 45,000 of tax.

- 80C is no reason to invest in Insurance & 5 years bank FDs.

PPF, ELSS are much better options (36/n)

- Cash that u generate by avoiding tax gets spent & does nt help u grow ur wealth. Its better 2 pay tax & invest the rest. Calculations show that in 3 years of investing, u recover the tax u paid & the investment can then keep growing(37/n)

A thread on National Pension Scheme (NPS)

— Kirtan A Shah (@KirtanShahCFP) November 25, 2020

This is the simplest yet the most comprehensive piece around. Do \u2018re-tweet\u2019 and help us reach more investors \u263a

(1/n)

- It’s a blessing to be debt free

- Home loan, working capital loan kind of loans are okay but strictly avoid personal & credit card loans

- Don’t take loans & invest

& finally, have a will! (39/n)

Link - https://t.co/sr86RDqq0N (40/n)

- Sector Analysis

- Macro Economics

- Debt Markets

- Real Estate

- Equity Markets etc.

You can find them all in the link below. Do hit the re-tweet & help us reach a larger audience

https://t.co/UrRt87xaU7 (**END**)

Here\u2019s a compilation of Personal Finance threads I have written so far. Thank you for motivating me to do it.

— Kirtan A Shah (@KirtanShahCFP) December 13, 2020

Hit the 're-tweet' and help us educated more investors