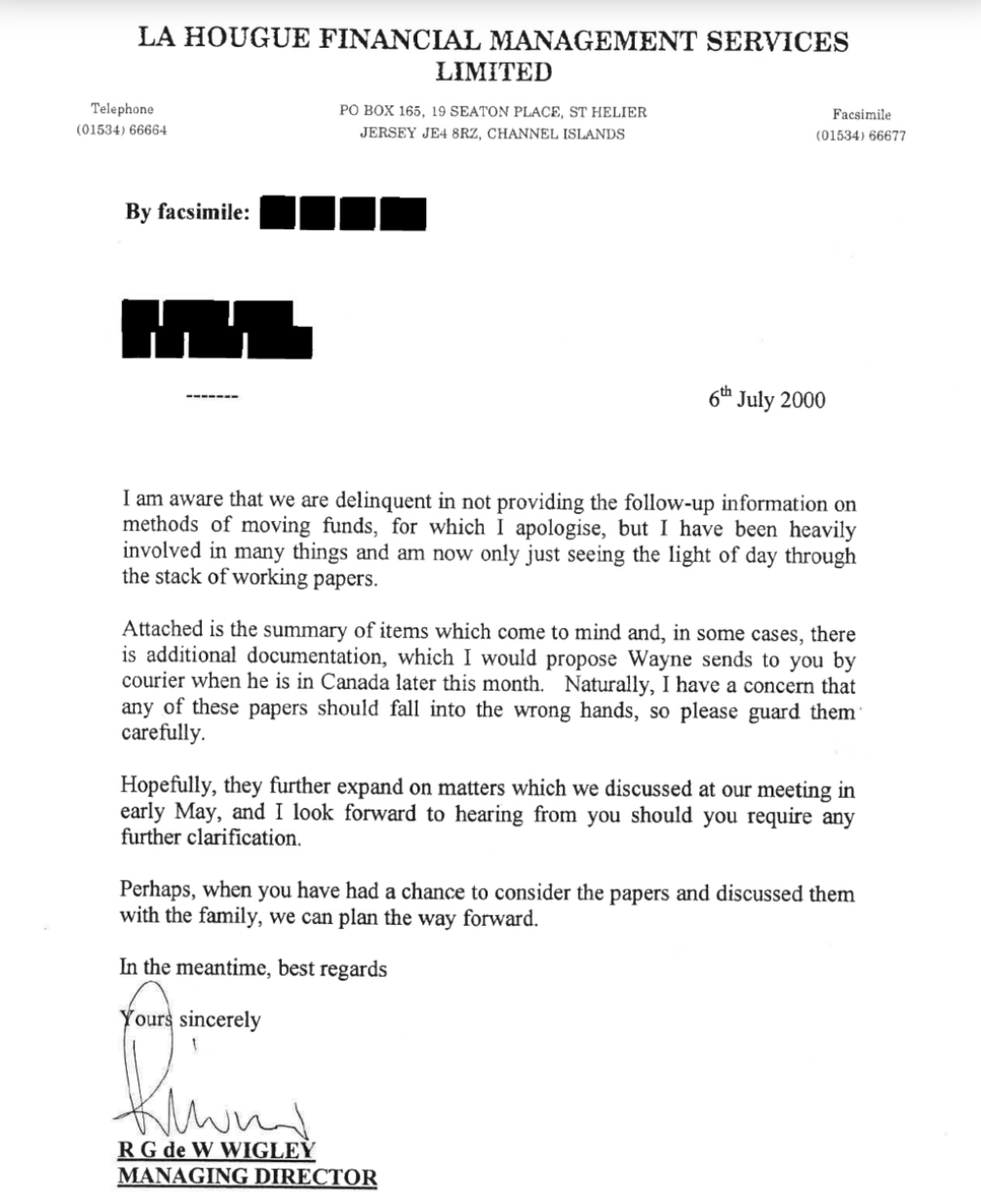

Amid the data, this memo stood out for its candor.

1/ This is a memo outlining 11 ways to hide your money offshore.

It was not supposed to “fall into the wrong hands.”

Well, it did. https://t.co/N6RUDqHVfR

Amid the data, this memo stood out for its candor.

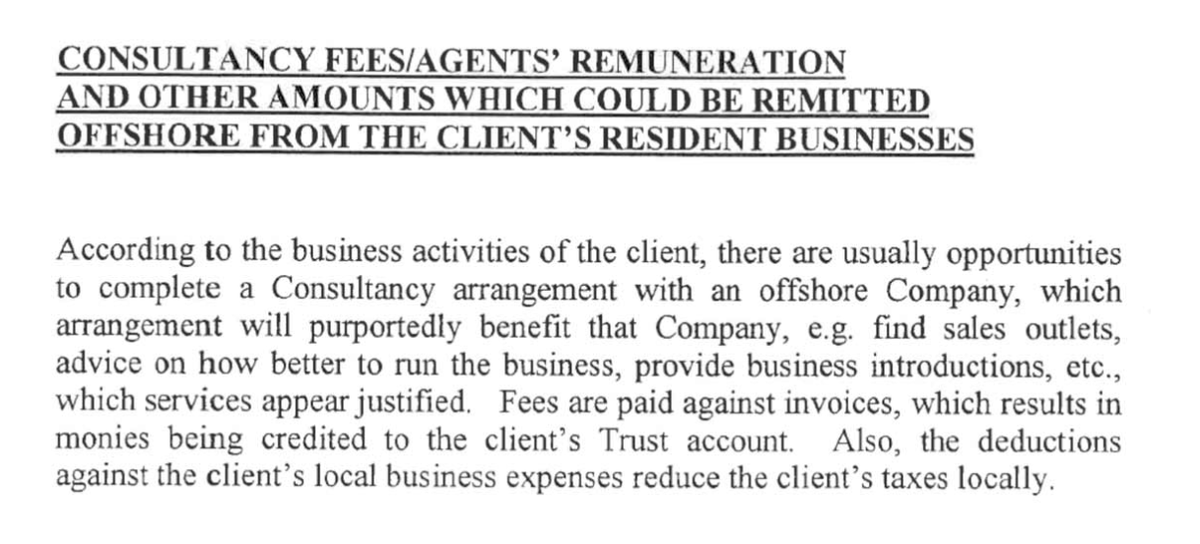

For instance, you could hire an offshore company to do some fake consulting for your business (who knows what consultants do anyway, right?). Your payments go to your offshore account, and you get to write off the fees as an expense.

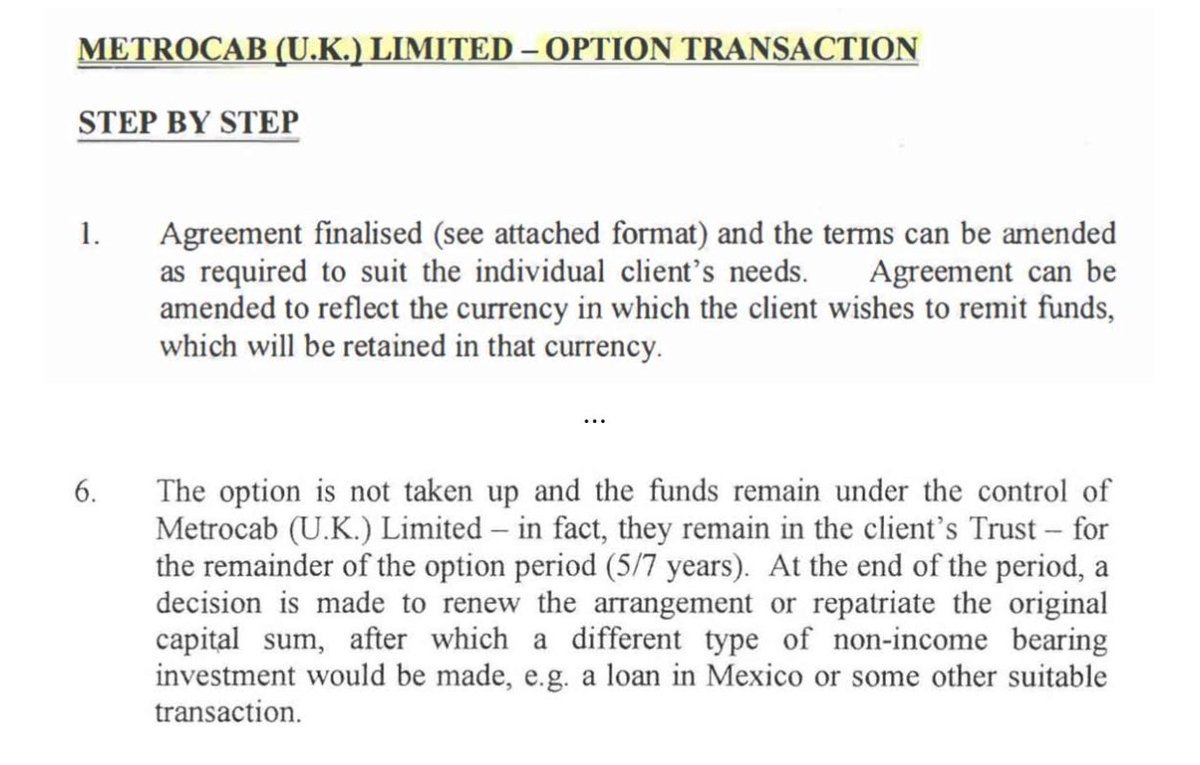

Lose your money on bad “investments.” You can lucratively lose 6-figure sums by lending to and investing in companies that never show a profit (or even care to earn one). Then you get to write off the planned losses at tax time.

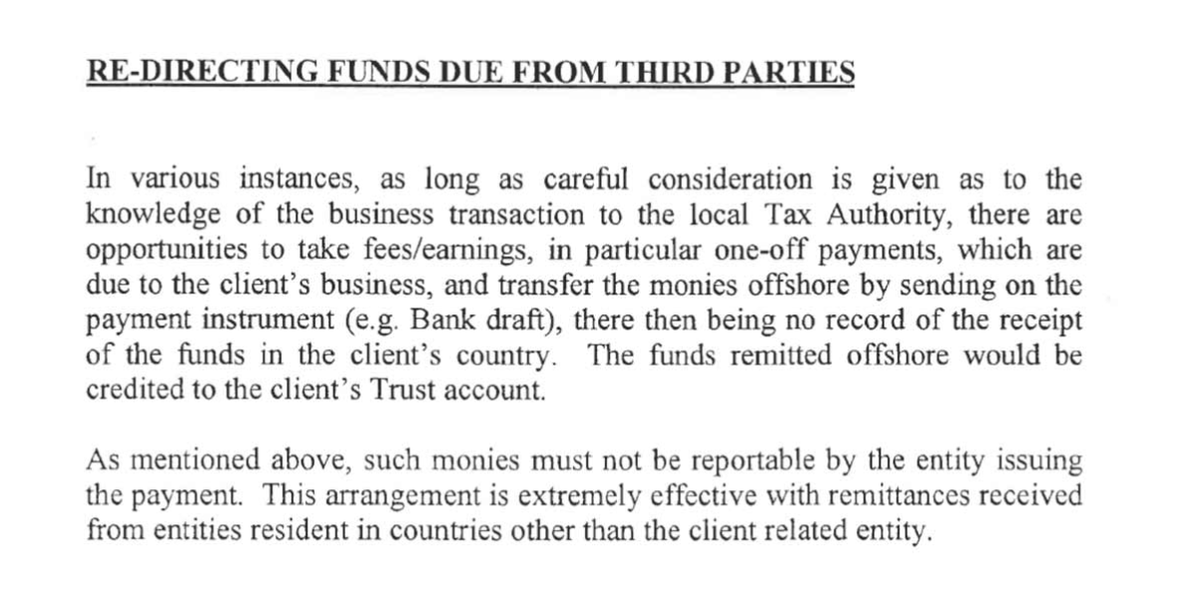

Does someone owe you money? Don’t invoice them—have them send that payment directly into your offshore account, so you never have to declare it.

Owe your money to a third party (who is, in effect, you). If you can produce a contract that says you owe money—that becomes a business expense.

Sell off part of your business (to a secretive entity you happen to control). If you don’t appear to own the business, you don’t have to pay taxes on its profits.

And if you’re curious about what else showed up in that batch of 350,000 leaked documents, read more from @GlobalRepCentre: https://t.co/vtAregqTwR

More from Finance

Thread: P&F Super Pattern

An effective price pattern defined using properties of P&F charts.

#Superpattern #Pointandfigure #Definedge

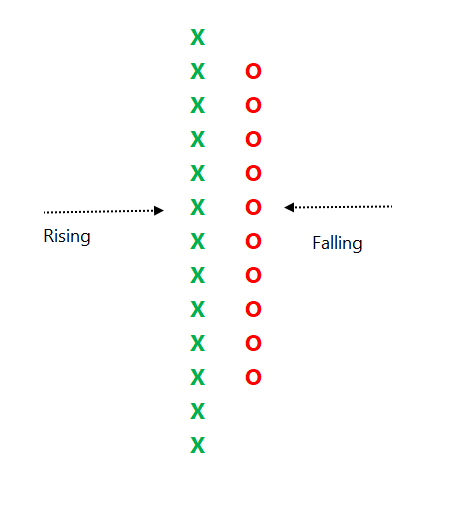

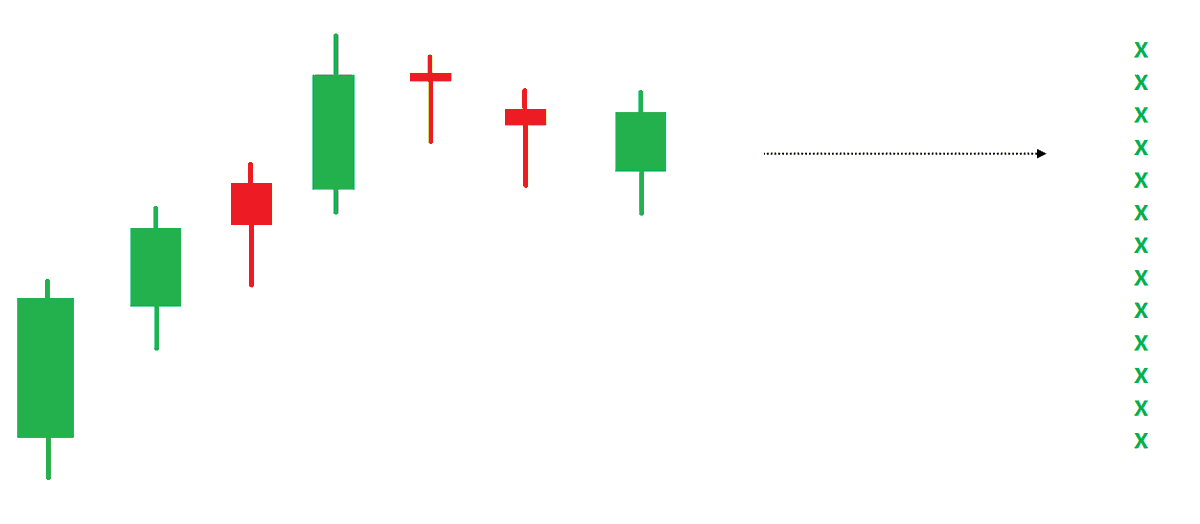

Point & Figure is an oldest charting method where price is plotted vertically, and the chart moves only when price moves. It is a different way of looking at the price, the objective box-value and reversal value offers advantage of identifying objective price patterns.

When price is moving up, it is plotted in a column of 'X'. When it is going down, it is plotted in a column of ‘O’. Normally, three-box reversal criteria is used to define the trend & reversal. Unlike a bar or candle, the P&F column can have multiple sessions in it.

Link to know more about the subject:

https://t.co/2xtLAVPBvm

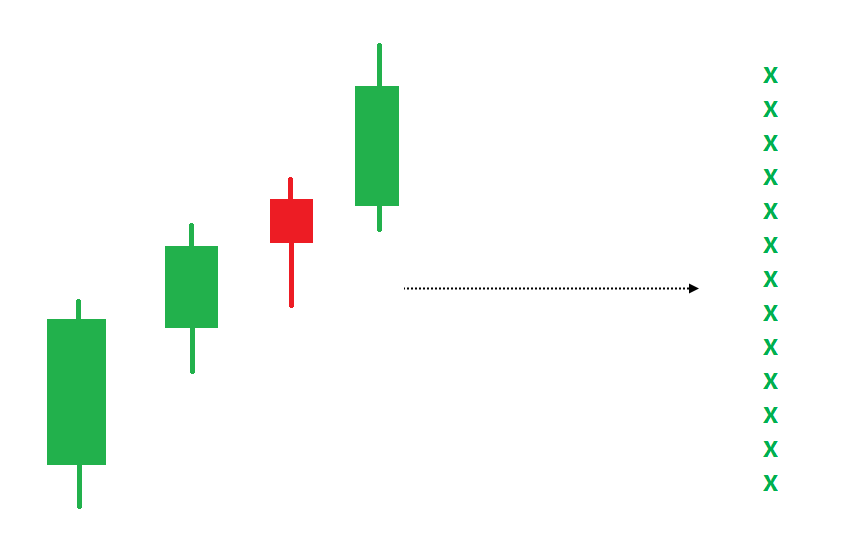

See below chart. Price is in a strong uptrend, P&F chart would produce a long of column of 'X' with more number of boxes in it.

If such a trend is followed by some time bars without meaningful price correct, P&F chart would not move, and it will remain in column of 'X' in such a scenario.

An effective price pattern defined using properties of P&F charts.

#Superpattern #Pointandfigure #Definedge

Point & Figure is an oldest charting method where price is plotted vertically, and the chart moves only when price moves. It is a different way of looking at the price, the objective box-value and reversal value offers advantage of identifying objective price patterns.

When price is moving up, it is plotted in a column of 'X'. When it is going down, it is plotted in a column of ‘O’. Normally, three-box reversal criteria is used to define the trend & reversal. Unlike a bar or candle, the P&F column can have multiple sessions in it.

Link to know more about the subject:

https://t.co/2xtLAVPBvm

See below chart. Price is in a strong uptrend, P&F chart would produce a long of column of 'X' with more number of boxes in it.

If such a trend is followed by some time bars without meaningful price correct, P&F chart would not move, and it will remain in column of 'X' in such a scenario.

Ok here is the explanation. Grab a cup of coffee and read on. If you have not read/noticed this, you will see intraday options movement in a new light.

Say we have two options, one 50 delta ATM options and another 30 delta OTM option. Normally for a 100 point move, the ATM option will move 50 points and the OTM option will move 30 points. But in a high volatile environment, the OTM option will also move nearly 50 points

To understand why this happens, first understand why an ATM option is 50 delta. An ATM option has the probability of 50% of expiring as ITM. The price just has to close a rupee above the strike for the CE to be ITM and vice versa for PEs

Now think of a highly volatile day like today. If someone is asked where the BNF will close for the day or expiry, no one can answer. BNF can close freakin anywhere, That makes every option of an equal probability of being ITM. So all options have a 50% probability of being ITM

Hence, when a huge volatile move starts, all OTM options behave like ATM options. This phenomenon was first observed in the Black Monday crash of 1987 at Wall Street, which also gave rise to the volatility skew/smirk

In a high IV environment or when the market is very volatile

— Subhadip Nandy (@SubhadipNandy16) January 21, 2022

" OTM options will behave like ATM options", one will get almost the same delta movement

Say we have two options, one 50 delta ATM options and another 30 delta OTM option. Normally for a 100 point move, the ATM option will move 50 points and the OTM option will move 30 points. But in a high volatile environment, the OTM option will also move nearly 50 points

To understand why this happens, first understand why an ATM option is 50 delta. An ATM option has the probability of 50% of expiring as ITM. The price just has to close a rupee above the strike for the CE to be ITM and vice versa for PEs

Now think of a highly volatile day like today. If someone is asked where the BNF will close for the day or expiry, no one can answer. BNF can close freakin anywhere, That makes every option of an equal probability of being ITM. So all options have a 50% probability of being ITM

Hence, when a huge volatile move starts, all OTM options behave like ATM options. This phenomenon was first observed in the Black Monday crash of 1987 at Wall Street, which also gave rise to the volatility skew/smirk

You May Also Like

1/ Here’s a list of conversational frameworks I’ve picked up that have been helpful.

Please add your own.

2/ The Magic Question: "What would need to be true for you

3/ On evaluating where someone’s head is at regarding a topic they are being wishy-washy about or delaying.

“Gun to the head—what would you decide now?”

“Fast forward 6 months after your sabbatical--how would you decide: what criteria is most important to you?”

4/ Other Q’s re: decisions:

“Putting aside a list of pros/cons, what’s the *one* reason you’re doing this?” “Why is that the most important reason?”

“What’s end-game here?”

“What does success look like in a world where you pick that path?”

5/ When listening, after empathizing, and wanting to help them make their own decisions without imposing your world view:

“What would the best version of yourself do”?

Please add your own.

2/ The Magic Question: "What would need to be true for you

1/\u201cWhat would need to be true for you to\u2026.X\u201d

— Erik Torenberg (@eriktorenberg) December 4, 2018

Why is this the most powerful question you can ask when attempting to reach an agreement with another human being or organization?

A thread, co-written by @deanmbrody: https://t.co/Yo6jHbSit9

3/ On evaluating where someone’s head is at regarding a topic they are being wishy-washy about or delaying.

“Gun to the head—what would you decide now?”

“Fast forward 6 months after your sabbatical--how would you decide: what criteria is most important to you?”

4/ Other Q’s re: decisions:

“Putting aside a list of pros/cons, what’s the *one* reason you’re doing this?” “Why is that the most important reason?”

“What’s end-game here?”

“What does success look like in a world where you pick that path?”

5/ When listening, after empathizing, and wanting to help them make their own decisions without imposing your world view:

“What would the best version of yourself do”?