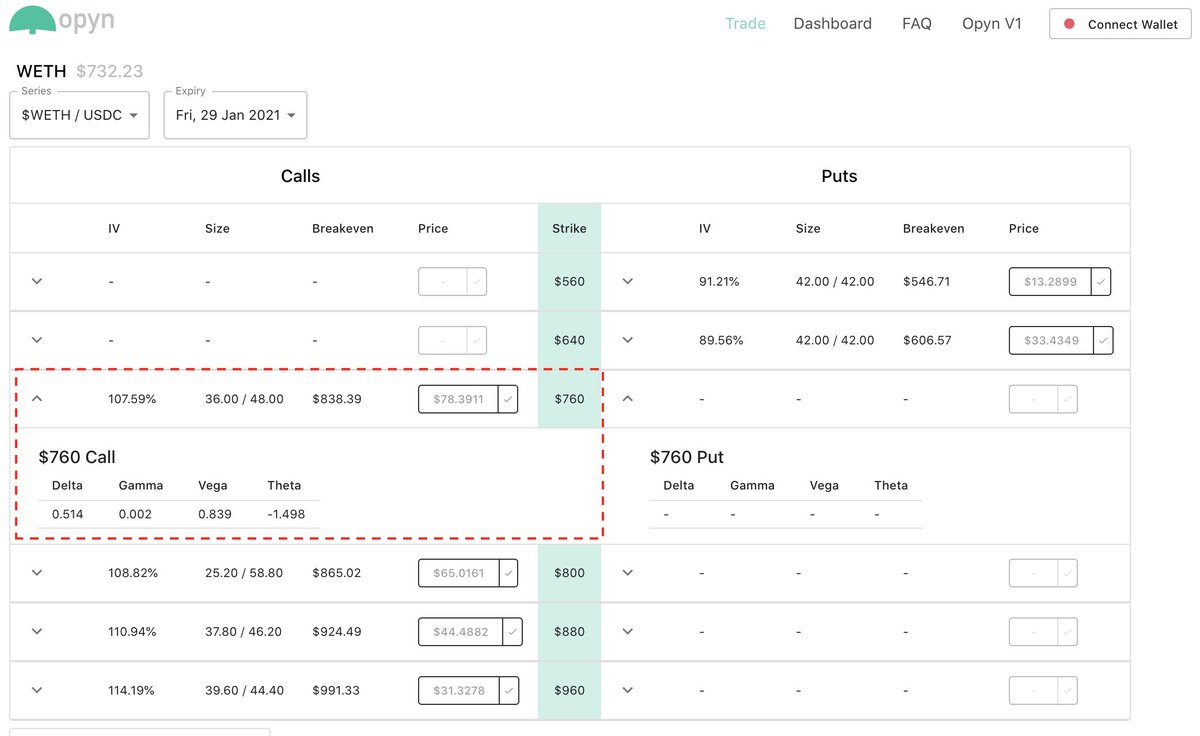

1. Congrats to the @opyn_ team for launching V2 - very exciting! I’m happy that the new V2 dashboard has a clean layout with greeks and implied vols for each respective option. It’s also a pleasant surprise to see the prices are closely in line with @DeribitExchange's options.

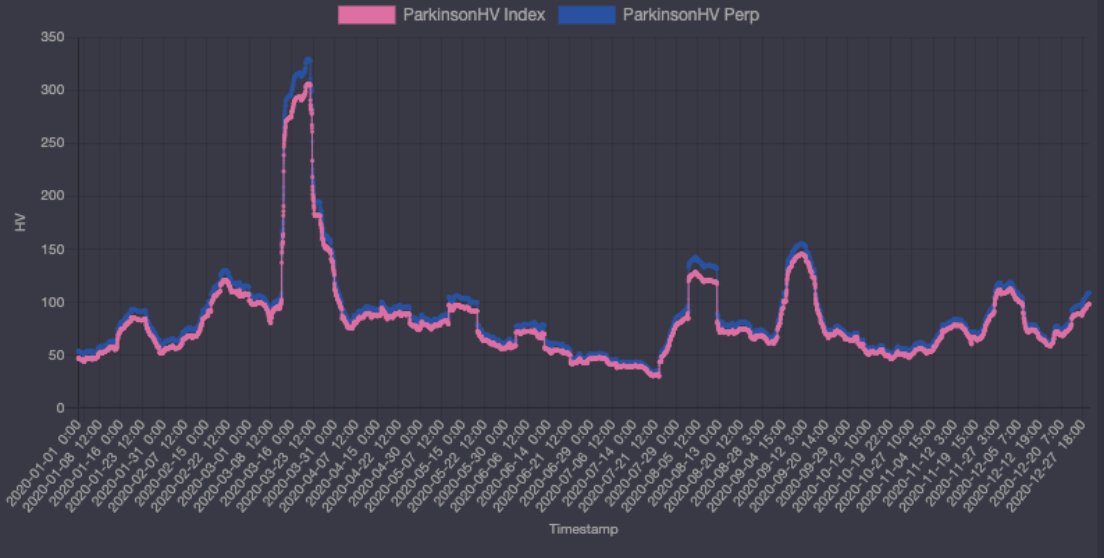

- Realized Volatility

- Implied Volatility

- Delta

LONG: Call Option: +0.514 ETH Delta

SHORT: @dydxprotocol ETH: -0.514 ETH Delta

------------------------------------------------

Net Portfolio Delta Exposure = 0

More from Crypto

We are actively working to launch on @binance Smart Chain #BSC .

To make this transition easy & understandable for everyone, we are answering most frequently asked questions here.

Ready? Go! 🔥

1/24

#DeFi #YieldFarming

Q1 - What are the benefits of holding the $VALUE token on the Ethereum Mainnet network? Give me reasons not to sell. Some are assuming that the VALUE token will be abandoned now that vBSWAP is being created. Can you clarify the use case for VALUE?

👉 $VALUE will always be a governance & profit receiving token of the whole ecosystem if staked in #vGov. With the new farming token on #BSC , gvVALUE holders will get extra rewards at BSC if they choose to bridge their gvVALUE to BSC & stake in gvVALUE-B/BUSD 98/2 pool.

Q2 - What do I need to do with my VALUE tokens that are staked in vGov? Is it OK to leave them in the vGov?

👉If you have VALUE but aren't staking in the vGov & you would like to participate in the BSC expansion, you will need to stake your VALUE in the vGov to receive gvVALUE.

If you are staking in vGov but don't see the correct gvVALUE amount in your wallet, go to vGov (https://t.co/udXn5IJtVx) to unlock your gvVALUE from the old contract. There will be a bridge from ETH to BSC to move gvVALUE and vUSD over.

To make this transition easy & understandable for everyone, we are answering most frequently asked questions here.

Ready? Go! 🔥

1/24

#DeFi #YieldFarming

Q1 - What are the benefits of holding the $VALUE token on the Ethereum Mainnet network? Give me reasons not to sell. Some are assuming that the VALUE token will be abandoned now that vBSWAP is being created. Can you clarify the use case for VALUE?

👉 $VALUE will always be a governance & profit receiving token of the whole ecosystem if staked in #vGov. With the new farming token on #BSC , gvVALUE holders will get extra rewards at BSC if they choose to bridge their gvVALUE to BSC & stake in gvVALUE-B/BUSD 98/2 pool.

Q2 - What do I need to do with my VALUE tokens that are staked in vGov? Is it OK to leave them in the vGov?

👉If you have VALUE but aren't staking in the vGov & you would like to participate in the BSC expansion, you will need to stake your VALUE in the vGov to receive gvVALUE.

If you are staking in vGov but don't see the correct gvVALUE amount in your wallet, go to vGov (https://t.co/udXn5IJtVx) to unlock your gvVALUE from the old contract. There will be a bridge from ETH to BSC to move gvVALUE and vUSD over.

Back with another #FreeLoveFriday. Last time, we covered how Mastercoin/@Omni_Layer pioneered digital asset issuance on blockchains. Today, let’s discuss @Chainlink and the vital role it plays in connecting blockchains to the real world.

I have said repeatedly that digital asset issuance is the killer application for blockchains. The next frontier is bringing real world assets to networks like @AvalancheAVAX, but we often face a significant problem:

Namely, how do you get data from the real world onto blockchains and into applications running on them? More critically, how do you achieve that securely and transparently in real-time? Smart contracts are tamper-proof, but they're only as reliable as their input data.

Enter ChainLink in September 2017, with a whitepaper outlining a vision for a decentralized network of “oracles,” entities that inject facts from the external world into blockchains in a suitable format for smart contracts.

Until ChainLink, oracles were trusted and centralized. This is a huge problem for high-value assets and smart contracts. High value projects, such as @CelsiusNetwork, @synthetix_io, @Aaveaave and others depend critically on oracle data.

Back with another #FreeLoveFriday. My first thread focused on what I love about Bitcoin, and features we borrowed for @AvalancheAVAX. Today, let's focus on @Omni_Layer, or as OGs knew it, Mastercoin https://t.co/fXFgmaeUEz

— Emin G\xfcn Sirer (@el33th4xor) January 15, 2021

I have said repeatedly that digital asset issuance is the killer application for blockchains. The next frontier is bringing real world assets to networks like @AvalancheAVAX, but we often face a significant problem:

Namely, how do you get data from the real world onto blockchains and into applications running on them? More critically, how do you achieve that securely and transparently in real-time? Smart contracts are tamper-proof, but they're only as reliable as their input data.

Enter ChainLink in September 2017, with a whitepaper outlining a vision for a decentralized network of “oracles,” entities that inject facts from the external world into blockchains in a suitable format for smart contracts.

Until ChainLink, oracles were trusted and centralized. This is a huge problem for high-value assets and smart contracts. High value projects, such as @CelsiusNetwork, @synthetix_io, @Aaveaave and others depend critically on oracle data.