EPC companies have razor thin margins, they aren't the places to bet on.

It's the commodity makers who make real money and within commodity makers it's the ones with least disruption to their price and limited competition.

In solar chain, these are the solar glass players ☀️👓

More from Tar ⚡

Open Question to fellow investors tracking Music Industry.

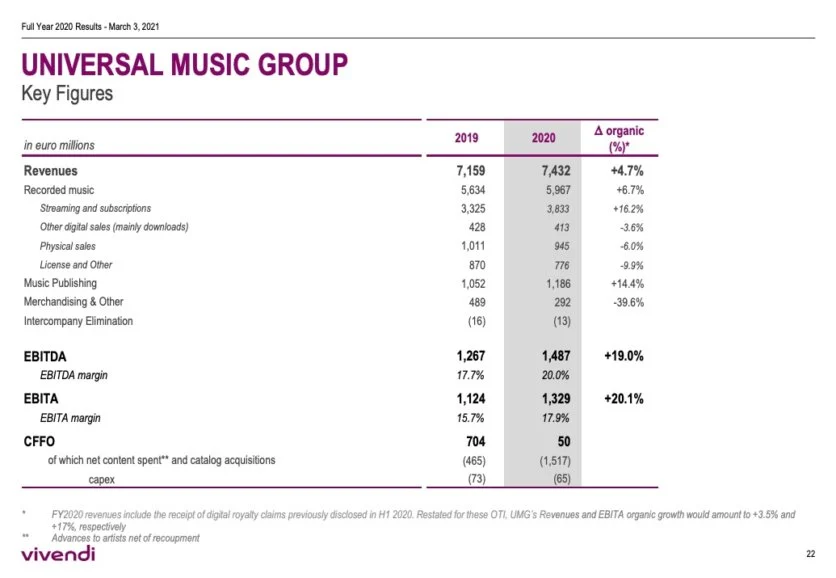

A business like Universal which controls more than 1/3rd of all published music globally is selling for less than 6x FY20 Sales.

Why are Indian businesses like Saregama / Tips selling for 11x, 20x their sales?

If I include all of the revenue generated by entire firm, its selling for ~4.5x FY20 Sales

Universal Listing Market Cap ~ 40 Billion USD

FY 20 Revenues ~ 8.87 B USD or 7.4B EUR

Catalogue of Music includes every international artist you can possibly name

Either Universal is grossly undervalued or Saregama/Tips are grossly overvalued.

https://t.co/aHzWSYtcUt

https://t.co/v0EMoCuYKX

A business like Universal which controls more than 1/3rd of all published music globally is selling for less than 6x FY20 Sales.

Why are Indian businesses like Saregama / Tips selling for 11x, 20x their sales?

If I include all of the revenue generated by entire firm, its selling for ~4.5x FY20 Sales

Universal Listing Market Cap ~ 40 Billion USD

FY 20 Revenues ~ 8.87 B USD or 7.4B EUR

Catalogue of Music includes every international artist you can possibly name

Either Universal is grossly undervalued or Saregama/Tips are grossly overvalued.

https://t.co/aHzWSYtcUt

Homework for all the interested participants here:

— Intrinsic Compounding (@soicfinance) June 27, 2021

Q1.Why 20% and not 50%+ Margins for UMG

Q2. Differences in dynamics between Western&Indian cos?

Q3. Trends in West vs Trends in India in the industry.

Research and find the answers. My job is done \U0001f601\U0001f64f

https://t.co/v0EMoCuYKX

If you see the ebitda of universal music its low 20% compared to our saregama 30% or tips 50%. So when you compare earnings saregama is 40x and tips is 30x and universal music is 30x. Also these type of companies are less( low or no capex with excellent and growinh cashflows)

— Srikanth V (@mynameisnani75) June 27, 2021

China Index has corrected ~40% since its peak

Lot of regulatory crackdown in China. Top rated companies are available for huge discounts. $BABA for example now has a market cap of less than 600 Billion and is bigger than Amazon in every regard.

I have been aggressively investing more in Chinese equities than Indian ones.

https://t.co/W1RWdKU3sy

Lot of regulatory crackdown in China. Top rated companies are available for huge discounts. $BABA for example now has a market cap of less than 600 Billion and is bigger than Amazon in every regard.

I have been aggressively investing more in Chinese equities than Indian ones.

https://t.co/W1RWdKU3sy