What are dividend yield funds?

A thread 🧵👇

Bonus: Comments on HDFC Dividend Yield Fund (NFO)

an important advantage of investing in such funds for large investors is tax arbitrage.

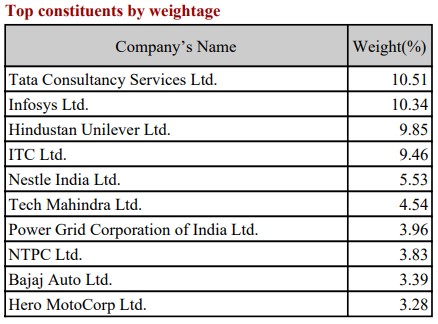

- Scheme will invest a minimum of 65% of corpus in high dividend yield stocks.

- Preference will be given to stocks with a consistent history of paying dividends.

- Stock having higher DY than the Nifty 50 index will be preferred. (Most PSU utility and energy companies qualify).

- Investing in low capital intensive business (Most IT companies).

- Ability to increase dividend payouts.

- Dividend yield at 1x - 2x of 10-year G-sec yield.

- It will be sector and market cap agnostic.

My take on this NFO:

- Most of the stocks in portfolio will be PSU utility & energy cos that have not performed well in terms of share price growth. In some cases, The dividend yield was fully offset by the decline in share price thereby yielding zero or negative returns.

- Valuation could be a cause of concern while investing in FMCG companies even when they have stable dividend payouts. Time correction in such companies may result in below-par returns for the scheme.

- IT companies have displayed stability in terms of dividends along with decent stock price growth and are trading at reasonable valuations. A higher weightage to these companies may result in good performance of the scheme.

- Median expense ratio of this category of funds is around 1.5%. This coupled with lower share price growth stocks could lead to below-par returns.

More from Bank

Last week the @ECB extended its current asset purchase program, now totalling €1.8 tn. Several EU states can borrow at negative interest rates.

10 years ago, the eurozone almost collapsed, a result of a misconstructed currency that was meant to fail from the outset.

A thread👇

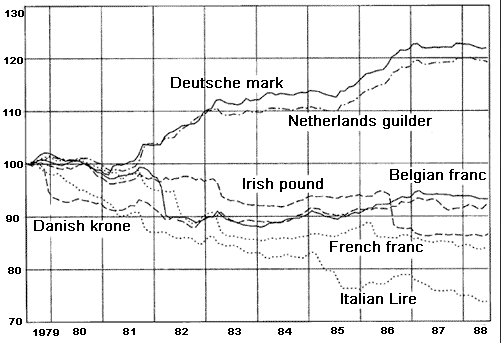

1/Before the introduction of the euro, fluctuating exchange rates were seen as threat for economic integration & embarrassment for those who were inflating their currencies faster than others.

The European Monetary System, set up in 1979, was an attempt to stabilise fx rates.

2/The EMS was doomed to fail as members applied different monetary policies while trying to keep their fx rates in a pre-defined corridor.

The German Bundesbank refused to devalue the Mark when other centr. banks inflated their currencies - strengthening the Mark by comparison.

3/Traditionally, Southern EU countries have been more prone to inflation & high debt levels due to a large public sector, strong labour unions & generous pension systems.

Northern countries like Germany & the Netherlands typically had more prudent monetary & fiscal policies.

4/To get rid of the stubbornly conservative Bundesbank & monetise public deficits more easily, Southern countries spearheaded by France pushed for a single currency and used Germany’s desire for reunification in 1989 to make it give up the D-Mark.

10 years ago, the eurozone almost collapsed, a result of a misconstructed currency that was meant to fail from the outset.

A thread👇

1/Before the introduction of the euro, fluctuating exchange rates were seen as threat for economic integration & embarrassment for those who were inflating their currencies faster than others.

The European Monetary System, set up in 1979, was an attempt to stabilise fx rates.

2/The EMS was doomed to fail as members applied different monetary policies while trying to keep their fx rates in a pre-defined corridor.

The German Bundesbank refused to devalue the Mark when other centr. banks inflated their currencies - strengthening the Mark by comparison.

3/Traditionally, Southern EU countries have been more prone to inflation & high debt levels due to a large public sector, strong labour unions & generous pension systems.

Northern countries like Germany & the Netherlands typically had more prudent monetary & fiscal policies.

4/To get rid of the stubbornly conservative Bundesbank & monetise public deficits more easily, Southern countries spearheaded by France pushed for a single currency and used Germany’s desire for reunification in 1989 to make it give up the D-Mark.

Saturday marks the 30th anniversary of German reunification.

— HODLdax (@HODLdax) September 30, 2020

Did you that Germany had to sacrifice its national currency for it?

Let\u2019s look back at the fateful decisions leading to the Euro, a secretive project driven by much political interest and little economic reason.\U0001f447 pic.twitter.com/XcWgBOr29O