1. Company's Background:

• Incorporated in 1987, Company is a leading decorative aesthetic parts supplier to Auto and Consumer durables Companies in India.

• It is basically a design to delivery player in the industry.

• The end markets served are 2W, PV, CD, CV, Medical devices, Farm equipment & sanitary ware.

• It supplied over 115 million parts with more than 6,000 SKUs in FY21 to around 170 customer locations in approximately 90 cities across 20 countries.

• Product offerings include decals and body graphics, 2D & 3D appliques/dials, 3D lux badges, domes, overlays, aluminum badges, IMD/IML, lens mask assembly & chrome-plated injection molding plastic parts apart from 2-W & PV aftermarket accessories under ‘Transform’ brand.

2. Products:

One of the few aesthetics product manufacturers in India which offers advanced technology products such as Capacitive Overlays, Optical plastics, 3D Dials, and IML/IMD’s.

Successful Diversification:

• The company has diversified its product offering from traditional aesthetics products (Decals, Logos, 2D Appliques, and Domes) to advanced products (3D Lux Logos/Badges, 3D Appliques, Lens Mask Assemblies, Optical Plastics, IME’s and IMLs/IMDs).

• The Company has also recently started offering products that use Chrome-plated printed and painted Injection Moulded plastic parts, such as Wheel covers, Radiator grills, and Door handles, following the acquisition of its Subsidiary Exotech Ltd.

Different Products, and Product wise Contribution:

3. INDUSTRY OVERVIEW

• Aesthetics is an important purchase consideration for buyers of discretionary consumer products such as automobiles and consumer durables, thereby being a product differentiator for OEMs.

• Unlike other auto components, aesthetic products are compact in size and require a lesser outlay on logistics costs, thereby enabling manufacturers to set up plants at cheaper locations away from automobile hubs.

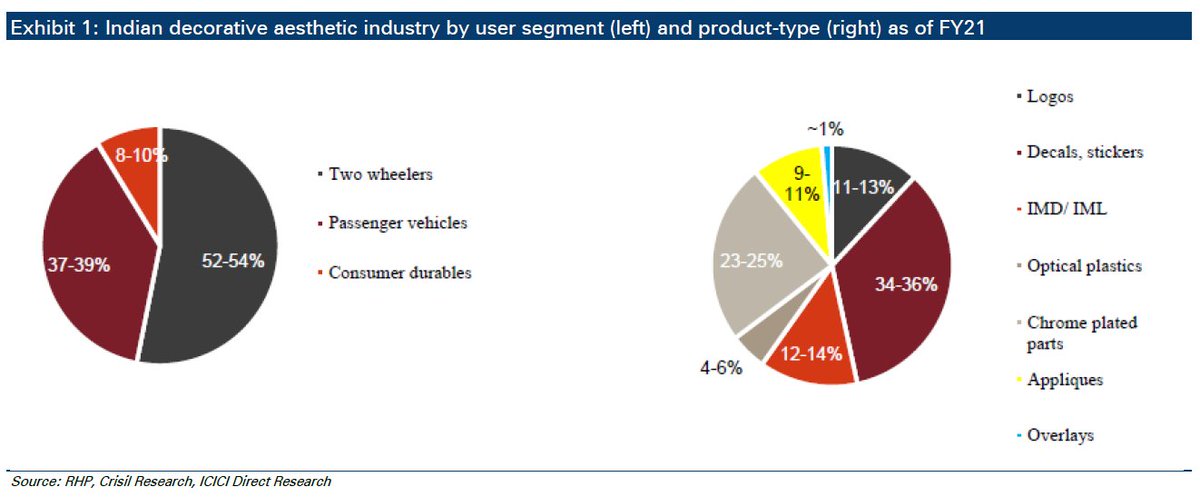

• As per Crisil Research, the size of the decorative aesthetic market in India catering to OEMs was at ~| 1,990 crores in FY21, with 2-W, PV & consumer durables comprising 52-54%, 37-39%, and 8-10% of demand, respectively.

• In terms of products, decals, stickers and aluminum badges accounted for 34-36% of the industry, followed by chrome-related products (23-25%), in-mold decorations/labels i.e. IMD/IML (12-14%) & appliques (9-11%).

• Globally, the decorative aesthetics industry for major PV markets like US & EU was at US$2.7 billion in CY19, as per Crisil Research.

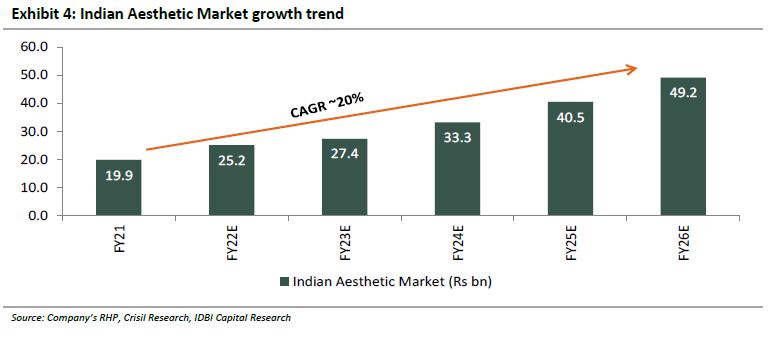

• Crisil Research expects the Indian decorative aesthetic market catering to OEMs to grow at 20% CAGR to ~| 4,920 crores by FY26E, led by growth in the underlying application segments, shift towards premium products (e.g. bigger cars, higher demand for mid/top car variants)

• Higher penetration of superior aesthetic products (such as optical plastics and chrome-related parts) and technology shift towards newer products that cost more.

• The Indian decorative aesthetics industry caters to leading auto OEMs, global independent tier-I automotive component makers, and also consumer appliance companies.

4. MANAGEMENT

Experienced and qualified Management is leading the company.

5. STRENGTHS

• Beneficiary of EV Disruption

• Leading aesthetics solutions provider

• Premium Play:- SJS collaborated with Suzuki to design and develop graphics for Swift, Ertiga, and WagonR models and has also previously worked with Honda Motorcycle, Royal Enfield, TVS Motors, Eureka Forbes, Bajaj Auto, and Whirlpool

• Strong Financial: With EBIDTA margin ranging between 29-30% and sales CAGR around 15% over FY2014-2020, SJS is 3rd largest player aesthetics player per CRISIL

• Large Customer Base

• Debt Free entity, High ROCE cash-generating business.

Acquisition of Exotech Ltd

• Acquired on April 5, 2021, by SJS, Exotech Plastics business includes manufacturing, assembling, producing, painting, chrome plating including injection molded items, etc.

• Exotech’s customer base includes leading passenger vehicles automotive OEMs and Tier-1 suppliers and customers in 2W, PV, CD, Farm equipment, and Sanitary ware industries

• Exotech was acquired on a share purchase basis upon payment of Rs 640mn with which the company forayed into the Chrome plating business in FY22.

• Acquisition is likely to enhance the company’s product portfolio, manufacturing capabilities, and customer base and will also help in enhancing cross-selling opportunities.

6. Manufacturing Facilities:

• Manufacturing facilities are located in Bengaluru (annual capacity of 20.8 crore units), with the April 2021 acquisition of subsidiary Exotech having an annual capacity of 2.95 crore units in Pune.

7. Customers:

The average age of relationships with its top-10 customers spans 15 years.

The company typically enters into a customer relationship for a specific product and then seeks to increase business share with them by pursuing cross-selling opportunities and expanding into other products and geographies with the customer and its related entities.

8. Financials:

The company is debt-free and cash-rich with a high ROCE generating business.

9. Key Risks:

• Inorganic Growth Risk

• Client and Segment concentration

• Heavy 2-W exposure could act as a growth headwind in the future.

• Raw Material Prices:- Principal raw materials used in manufacturing SJS aesthetic products are plastics, aluminum, and plastic polymers such as PVC, inks, chemicals, and adhesives.

Raw material costs formed ~38.4% of revenues from operations in FY21.

Raw material costs are higher for Exotech (~54.5% in FY21) with key raw materials being polymer granules, chemicals, paints, copper, nickel, tapes, and packing materials.

The company procured ~33.7% of raw materials from outside India in FY21.

11. Shareholding:

Promotor: 50.37%

FII: 6.04%

DII:18.32%

PUBLIC:25.27%

12. Valuations:

The industry is expected to grow at 20% CAGR over the next 5 years and SJS will be one of the biggest beneficiaries having high ROCE and a cash-generating business model.

With the company focuses on increasing export which will give a much-needed boost to revenue and growth

We believe sales will grow at 20% and EBITDA margin in the range of 26%-28% over the next 3 years. So we can expect EPS of around 34 in FY’24 and a price target of Rs 650.

13. Q3FY22 Highlights of the Business:

Industry Headwinds:

• Domestic PV industry sales volumes declined by 15% yoy led by supply chain disruptions

• Domestic 2W industry sales volumes were down by 25% YoY as retail sales remained weak due to a sharp increase in the cost of ownership of 2W and supply chain issues

• Automotive sales in India recorded the lowest numbers in 10 years this festive season.

• Major OEMs reduced productions as their semiconductor chip supplies have dried up, Improvement from mid-2022 onwards.

• Pressures of rising demand, but supply remaining as-is, the global chip shortage conundrum may continue this year, with some improvements to be seen from mid-2022 onwards.

• Some large chip manufacturers in U.S. and Europe are expanding their manufacturing capacity, which may aid in the recovery of the automotive industry from mid year

Sources: Company's website, RHP and brokerage reports.