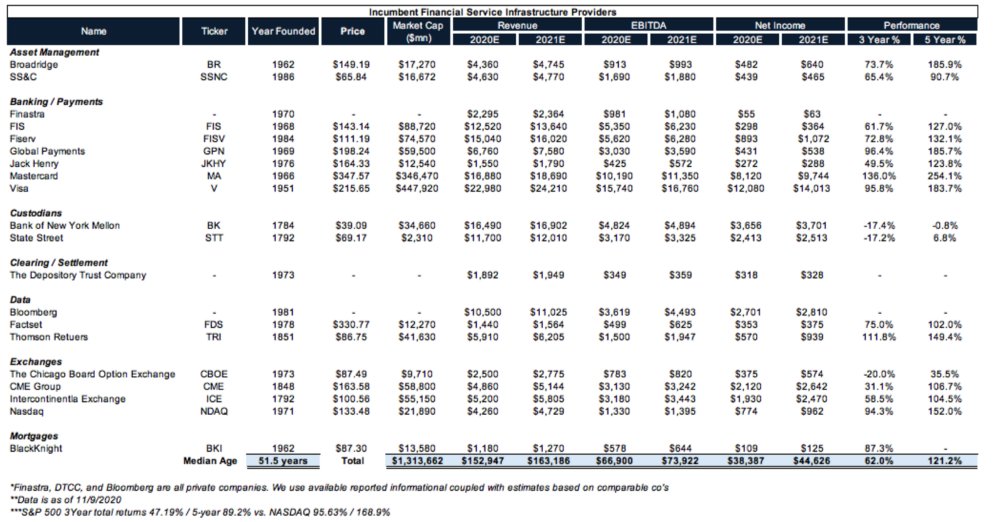

0/ We've highlighted FinTech infrastructure co's like BR, FIS, JKHY, MA, V, ICE, NDAQ, etc. as companies w/ a variety of moats that have led to dominant mkt share & outperformance despite being 50+ years old on avg.

$FISV had their investor day yesterday and laid out the why.

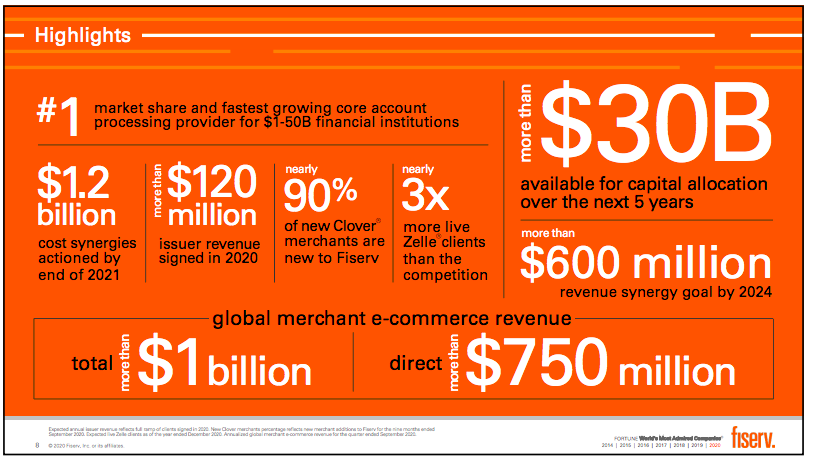

1/ $FISV highlights the fact that they have #1 market share in core accounting processing for $1-$50B FI’s; they are doing $1.0B in global e-Commerce revenue, and have more than $30B available for capital allocation over the next 5 years (read more M&A for FinTech co's)

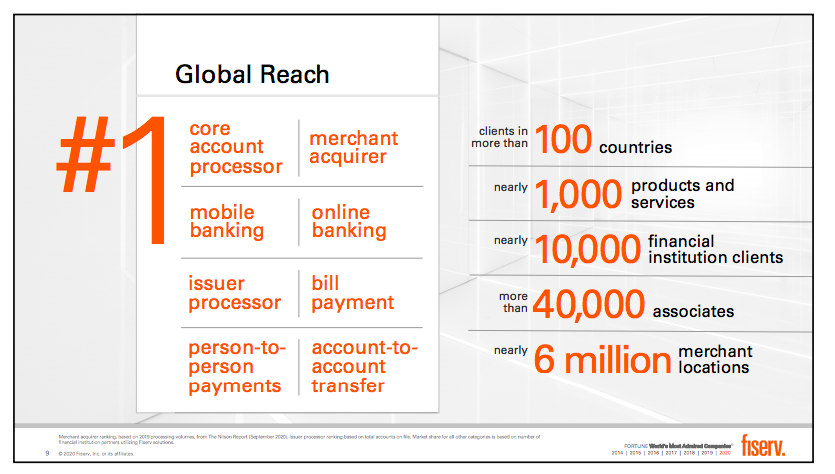

2/ They have global reach with clients in more than 100 countries, more than 1,000 products & services, 10,000+ FI clients, & 6M merchant locations.

All while being #1 as a core account processor, merchant acquirer, bill pay, P2P payments, etc...

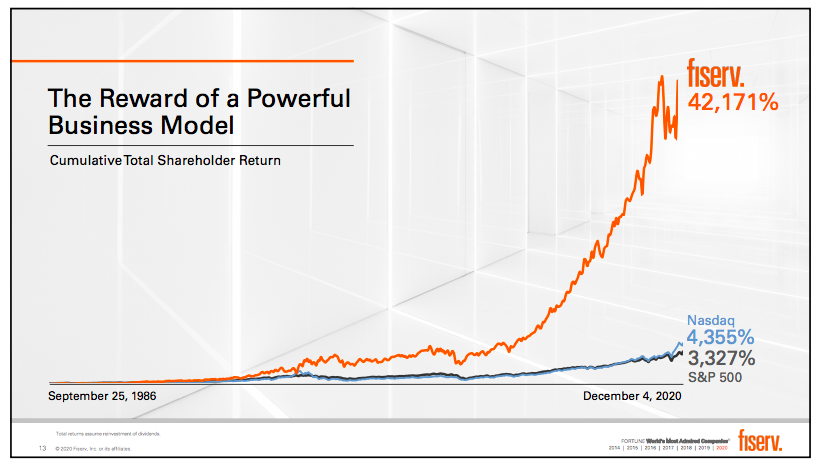

3/ This business model + market positioning has led to incredibly strong outperformance since inception ~35 years ago with cumulative $FISV shareholder returns of +42,171% vs. the $SPY at 3,327% & Nasdaq at 4,355%.

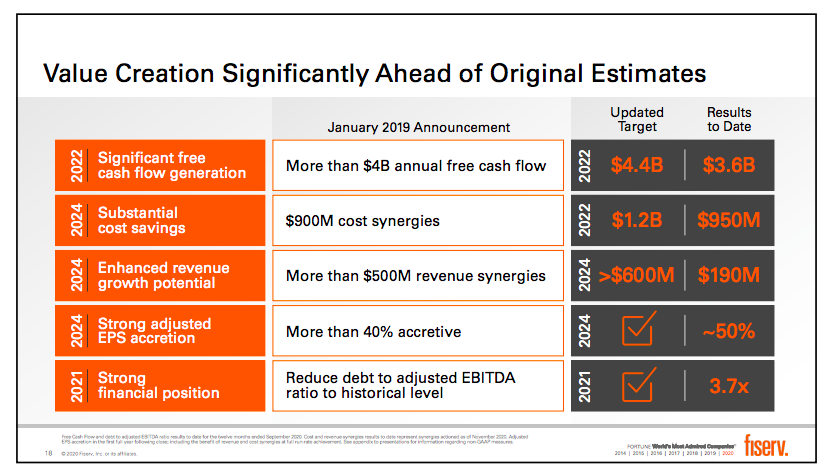

4/ $FISV has grown via a series of acquisitions over the past 30 years most recently the $22B tie up w/ First Data.

They highlight the progress on the deal & new goals post integration.

M&A is a skill & FISV has it financially; tech integration leaves something to be desired