For those who were trading in 2017 or earlier bull markets this may be obvious, but these kinds of corrections are typically driven by overleveraged longs, not whales dumping on you. That hasn’t started yet. Let me break down why it happens and why it is worse on the weekends.

There is a very real chance that BTC barely moves as this bull market plays out. The days of BTC as on-ramp to crypto are over, it\u2019s being bypassed almost completely as new money comes in primarily via stablecoins.

— kain.eth (@kaiynne) August 30, 2020

More from Bitcoin

The defi matrix

As each asset class goes on-chain, it can be stored in a digital wallet. And it can be traded against other such assets. Not just cryptocurrencies, but national digital currencies, personal tokens, etc.

We’re about to enter an age of global monetary competition.

The defi matrix is the table of all pair wise trades. It’s the fiat/stablecoin pairs, the fiat/crypto pairs, the crypto/crypto pairs, and much more besides.

Uniswap-style automatic market making for everything. Every possession you have, constantly marked to market by ~2040.

More liquidity, less currency?

This is an interesting point. Cash doesn’t make you money. In fact, it can lose you money in an inflating environment.

Reliable, 24/7 mark-to-market on everything is hard — but if achieved, means less % of assets in cash.

AMMs boost BTC. Here's why.

- All assets trade against all assets in the defi matrix

- Automated market makers give liquidity for rare pairs

- Everything is marked-to-market 24/7

- Value of cash drops, as you can liquidate instantly

- The new no-op is to keep your assets in BTC

Basically, automated market makers like @Uniswap boost BTC in the long term, because they allow *everything* to be priced in BTC terms, and *anyone* to switch out of BTC into their asset of choice.

Though in practice this may mean WBTC/RenBTC [or ETH!] rather than BTC itself.

As each asset class goes on-chain, it can be stored in a digital wallet. And it can be traded against other such assets. Not just cryptocurrencies, but national digital currencies, personal tokens, etc.

We’re about to enter an age of global monetary competition.

The defi matrix is the table of all pair wise trades. It’s the fiat/stablecoin pairs, the fiat/crypto pairs, the crypto/crypto pairs, and much more besides.

Uniswap-style automatic market making for everything. Every possession you have, constantly marked to market by ~2040.

More liquidity, less currency?

This is an interesting point. Cash doesn’t make you money. In fact, it can lose you money in an inflating environment.

Reliable, 24/7 mark-to-market on everything is hard — but if achieved, means less % of assets in cash.

Thus less use for currencies as people can more easily store their wealth into assets and easily trade them.

— Pierre-Yves Gendron (@pierreyvesg7) February 24, 2021

AMMs boost BTC. Here's why.

- All assets trade against all assets in the defi matrix

- Automated market makers give liquidity for rare pairs

- Everything is marked-to-market 24/7

- Value of cash drops, as you can liquidate instantly

- The new no-op is to keep your assets in BTC

Basically, automated market makers like @Uniswap boost BTC in the long term, because they allow *everything* to be priced in BTC terms, and *anyone* to switch out of BTC into their asset of choice.

Though in practice this may mean WBTC/RenBTC [or ETH!] rather than BTC itself.

Ok, so what is the significance of the @lagarde statement on bitcoin?

We were offered a very open insight (but slightly flawed analysis) into top level policy perspective behind the crack down on selfhosted wallets.

https://t.co/1LTzrxHbgs 1/32

'It is a speculative asset, by any account. If you look at the price movements... '

It starts with an economic price perspective and we can learn that ECB is closely monitoring this price movement as one of the many indicators.

So we are in the classic central bank frame 2/32

'Those who thought it would turn into a currency. Sorry, it is an asset not a currency.'

Here she summarises a classic debate on what is currency and what is needed for that. Based on the holy three: unit of account, means of payment, store of value. 3/32

The summary is classic, but too narrow and does not incorporate the wider financial history viewpoints on money, currencies and the way we pay. 4/32

ECB overlooks the de facto unit of account role of bitcoin, having been used to 200 years of having cash around whic is both the unit of account and a means of payment. 5/32

We were offered a very open insight (but slightly flawed analysis) into top level policy perspective behind the crack down on selfhosted wallets.

https://t.co/1LTzrxHbgs 1/32

ECB President Christine Lagarde called for global regulation of #Bitcoin, saying the digital currency had been used for money laundering activities in some instances and that any loopholes needed to be closed. Follow #ReutersNext updates here: https://t.co/4MgFy4jnw5 pic.twitter.com/qlBtoDuZLW

— Reuters (@Reuters) January 13, 2021

'It is a speculative asset, by any account. If you look at the price movements... '

It starts with an economic price perspective and we can learn that ECB is closely monitoring this price movement as one of the many indicators.

So we are in the classic central bank frame 2/32

'Those who thought it would turn into a currency. Sorry, it is an asset not a currency.'

Here she summarises a classic debate on what is currency and what is needed for that. Based on the holy three: unit of account, means of payment, store of value. 3/32

The summary is classic, but too narrow and does not incorporate the wider financial history viewpoints on money, currencies and the way we pay. 4/32

ECB overlooks the de facto unit of account role of bitcoin, having been used to 200 years of having cash around whic is both the unit of account and a means of payment. 5/32

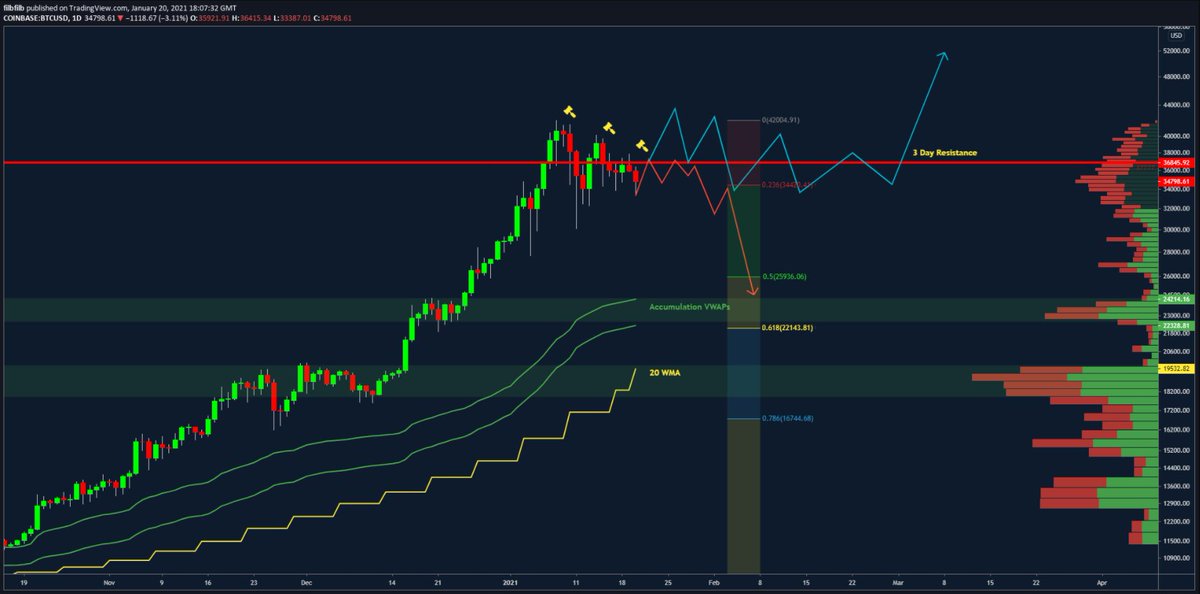

#Bitcoin update:

- Trapped in consolidation between $30 and $38k

- Lower highs and supply above c$38k

- Buying interest on the books £30-33k

- Meme consolidation triangle

- 20 wma @ $19.5k

- Accumulation VWAPs in the 20s

- underlying tether fud

- 61.8% retracement c. $22k

- 3 Day predator unconfirmed Orange candle

- Demand at low $30s was tested today and has since bounced & Coinbase led price on the drop

- Market structure is complex - Triangle is misleading

- Lots of orders stacked @ 30-33k.

- Market is fearful in the demand zone as shown by funding; i do not think we are ready to drop quite yet; Expecting longer consolidation.

- New Tether output has been on hold but new money came today

- Tether case request for 30 more days; could be indicative of consolidation

- Breakdown in price deeper than high $20s / lower $30s would IMO most likely require FUD induced event

- If stars align 20 WMA is catching up fast and will probably be resting in with the accumulation VWAPs, 61.8% retracement &d drives into big buy orders.

- Why did we stop @ $40k?

- Miners deep in profit vs. 654 average; time to tp

- SImilar response in other cycles

https://t.co/Iurd68NnZZ

- Trapped in consolidation between $30 and $38k

- Lower highs and supply above c$38k

- Buying interest on the books £30-33k

- Meme consolidation triangle

- 20 wma @ $19.5k

- Accumulation VWAPs in the 20s

- underlying tether fud

- 61.8% retracement c. $22k

- 3 Day predator unconfirmed Orange candle

- Demand at low $30s was tested today and has since bounced & Coinbase led price on the drop

- Market structure is complex - Triangle is misleading

- Lots of orders stacked @ 30-33k.

- Market is fearful in the demand zone as shown by funding; i do not think we are ready to drop quite yet; Expecting longer consolidation.

- New Tether output has been on hold but new money came today

- Tether case request for 30 more days; could be indicative of consolidation

- Breakdown in price deeper than high $20s / lower $30s would IMO most likely require FUD induced event

- If stars align 20 WMA is catching up fast and will probably be resting in with the accumulation VWAPs, 61.8% retracement &d drives into big buy orders.

- Why did we stop @ $40k?

- Miners deep in profit vs. 654 average; time to tp

- SImilar response in other cycles

https://t.co/Iurd68NnZZ

To chaiye chalte h 12K ki taraf.

#BTC https://t.co/Yd4iZqC42s

#BTC https://t.co/Yd4iZqC42s

I don't know why Crypto YouTubers are so bullish on BTC right from the top \U0001f61b while the charts are saying something else. Won't be surprised to see the entire retracement of the marked rise. #BTC pic.twitter.com/SQJkjAfZme

— Aakash Gangwar (@akashgngwr823) April 30, 2022

You May Also Like

Trading view scanner process -

1 - open trading view in your browser and select stock scanner in left corner down side .

2 - touch the percentage% gain change ( and u can see higest gainer of today)

3. Then, start with 6% gainer to 20% gainer and look charts of everyone in daily Timeframe . (For fno selection u can choose 1% to 4% )

4. Then manually select the stocks which are going to give all time high BO or 52 high BO or already given.

5. U can also select those stocks which are going to give range breakout or already given range BO

6 . If in 15 min chart📊 any stock sustaing near BO zone or after BO then select it on your watchlist

7 . Now next day if any stock show momentum u can take trade in it with RM

This looks very easy & simple but,

U will amazed to see it's result if you follow proper risk management.

I did 4x my capital by trading in only momentum stocks.

I will keep sharing such learning thread 🧵 for you 🙏💞🙏

Keep learning / keep sharing 🙏

@AdityaTodmal

1 - open trading view in your browser and select stock scanner in left corner down side .

2 - touch the percentage% gain change ( and u can see higest gainer of today)

Making thread \U0001f9f5 on trading view scanner by which you can select intraday and btst stocks .

— Vikrant (@Trading0secrets) October 22, 2021

In just few hours (Without any watchlist)

Some manual efforts u have to put on it.

Soon going to share the process with u whenever it will be ready .

"How's the josh?"guys \U0001f57a\U0001f3b7\U0001f483

3. Then, start with 6% gainer to 20% gainer and look charts of everyone in daily Timeframe . (For fno selection u can choose 1% to 4% )

4. Then manually select the stocks which are going to give all time high BO or 52 high BO or already given.

5. U can also select those stocks which are going to give range breakout or already given range BO

6 . If in 15 min chart📊 any stock sustaing near BO zone or after BO then select it on your watchlist

7 . Now next day if any stock show momentum u can take trade in it with RM

This looks very easy & simple but,

U will amazed to see it's result if you follow proper risk management.

I did 4x my capital by trading in only momentum stocks.

I will keep sharing such learning thread 🧵 for you 🙏💞🙏

Keep learning / keep sharing 🙏

@AdityaTodmal