As someone who tried the blockbuster rinse and repeat short (unsuccessfully btw) on $gme almost a decade ago I'm quite familiar with the name. Burry's re-emergence at the end of 2018 & roughly $5ml gme position disclosure then put the stock on the deep value radar.

So I've followed DFV's $GME journey from beginning and think it says a lot about what's going on here. How do u go from $50k to $40ml deep value screening in about a year which btw beats $nflx and $amzn growth return holding for decades? A

As someone who tried the blockbuster rinse and repeat short (unsuccessfully btw) on $gme almost a decade ago I'm quite familiar with the name. Burry's re-emergence at the end of 2018 & roughly $5ml gme position disclosure then put the stock on the deep value radar.

$gme dropped like 50% in h1 2019 and his q2 disclosure indicated he had exited the name. It was at this time DFV emerged onto WSB with an essentially i'll take this shot at half MB's cost basis with the console refresh a year out thesis.

I don't recall him fully articulating the thesis then, but that really didn't matter as MB remerged with a 3-4% activist stake by the Aug 2019 about 70% lower than his year end 2018 cost basis. MB wanted a buyback immediately & criticized mgmt past capital alloc failures.

To be clear the thesis did not provide deep dive analysis on $GME or the industry. MB simply seemed to be of the view that the console refresh meant things were not ending anytime soon, and that simply buying back stock in size was the right move for mgmt.

DFV structured his position around that console launch rerate, and to his credit has been fantastic to watch with respect how he has managed that all the way. Also, the guy is just super affable and clearly passionate which is a rare mix in the space. But the thesis was wrong.

The console refresh was actually viewed negatively by people who did the deep analysis on the name and so was a large buyback even after they sold Spring wireless. Enter COVID-19....

As the value trap that was $GME was playing out the pandemic added its bizarro twist on all things. In theory it made the business an obvious and faster secular death, but in practice it provided a gasp of financial life for it.

$GME was expected to reduce costs, but the bear thesis assumed continued pressure on the balance sheet as profitability erosion was accelerating. Covid temporary halted all this.

This wasn't obvious to most people till the fall, and it definitely wasn't obvious to DFV in the summer when he posted his video explaining his entire thesis to the now growing audience on WSB. He was actually shocked the stock was under $4 with consoles now around the corner.

But the thesis started to catch some interest as gaming and hobby demand under covid combined with a high short interest was sprinkled on top of the console catalyst. Then the Chewy founder showed up at the end of august with a turnaround angle for the post-covid ecom era.

At this point DFV entered influencer land with his updates and the stock 3x pretty quick as the temporary covid benefits came to light. It's around here that the 'deep value' investment should been sold. But now it was an ecom-inflcr/turnaround stk w console lurking..MOAR!

On the bear side though nothing had changed, in fact the consensus view was the odds of a turnaround were now even less likely and the post-covid cliff looming now accelerated as far as digital delivery.

So, in sum the original thesis was wrong. In fact, GME would most likely blown up had it done an accelerated buyback. And console is proving to be exactly what the bears said it wud be. But Covid brought a giant audience to DFV who bought the same thesis.

And they bought the thesis because it was genuine, and to almost anyone who didn't really wade into things made perfect sense. Anecdotal online evidence of resilience of physical disks etc combined with hobby trading mania was enough for them.

And $chwy founder added a whole new narrative to the name. So, DFV was wrong enough to not be successful on his deep value buy before the consl refresh and lucky enough to catch a pandemic so bad that $gme couldn't continue failing on its path without some interruption.

This brings me to the last part. The current gamma squeeze and the chaos around it. The stock has gone from $20 to nearly $500 in nearly ten trading sessions. DFV has continued to hold his stock and bulk of options. This is most definitely not deep value investing.

More from Trading

Thread on Short straddle with adjustments:

Short straddle is non-directional strategy

Selling same strike price CALL/PUT option same underlying with same expiry.

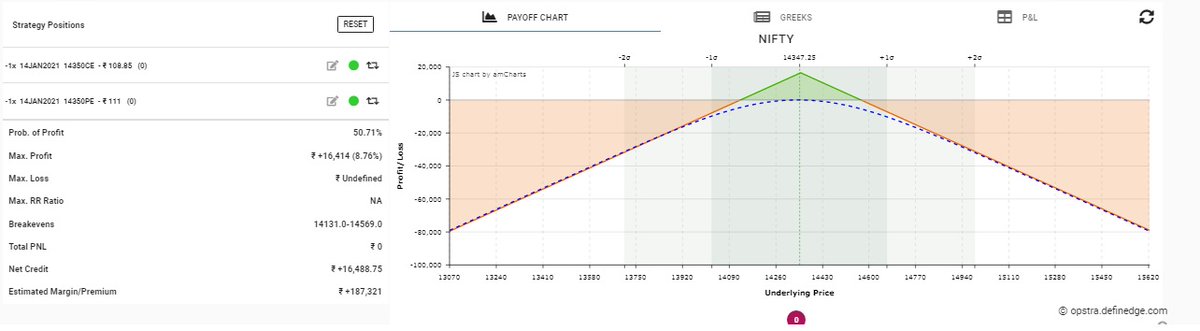

Nifty Spot at 14353, So you can sell 14350 CE as well 14350 PE of 14 Jan. Expiry.

(1/n)

*RETWEET for max response

Bullish short straddle: Selling 14400 CE and 14400 PE of same expiry.

Bearish short straddle: Selling 14250 CE and 14250 PE of same expiry.

You can sell straddle as per your market view.

If you are natural view sell CE and PE at ATM strike.

(2/n)

Short straddle has limited profit potential (only premium) and unlimited risk without adjustment.

In Example, Short straddle of 14350, Breakeven is (14131.0-14569.0), need 1.7Lac Margin to sell straddle.

Maximum profit: 16k and Loss: Unlimited, Winning probability: 50%

(3/n)

If market staying near at 14350 then win. Probability increase slowly. Rewards also increase slowly.

Volatility(IV) is also play important role in selling straddle, Like If IV increase so straddle premium increase and IV cool off so premium casually comes down.

(4/n)

Short straddle adjustment:

https://t.co/59Lr64kEtK way to limit the overnight risk.

Convert short straddle in Ironfly, its nothing we have to add long strangle in short straddle it become Ironfly. It gives the good Risk Rewards.

(5/n)

Short straddle is non-directional strategy

Selling same strike price CALL/PUT option same underlying with same expiry.

Nifty Spot at 14353, So you can sell 14350 CE as well 14350 PE of 14 Jan. Expiry.

(1/n)

*RETWEET for max response

Bullish short straddle: Selling 14400 CE and 14400 PE of same expiry.

Bearish short straddle: Selling 14250 CE and 14250 PE of same expiry.

You can sell straddle as per your market view.

If you are natural view sell CE and PE at ATM strike.

(2/n)

Short straddle has limited profit potential (only premium) and unlimited risk without adjustment.

In Example, Short straddle of 14350, Breakeven is (14131.0-14569.0), need 1.7Lac Margin to sell straddle.

Maximum profit: 16k and Loss: Unlimited, Winning probability: 50%

(3/n)

If market staying near at 14350 then win. Probability increase slowly. Rewards also increase slowly.

Volatility(IV) is also play important role in selling straddle, Like If IV increase so straddle premium increase and IV cool off so premium casually comes down.

(4/n)

Short straddle adjustment:

https://t.co/59Lr64kEtK way to limit the overnight risk.

Convert short straddle in Ironfly, its nothing we have to add long strangle in short straddle it become Ironfly. It gives the good Risk Rewards.

(5/n)

You May Also Like

1/ 👋 Excited to share what we’ve been building at https://t.co/GOQJ7LjQ2t + we are going to tweetstorm our progress every week!

Week 1 highlights: getting shortlisted for YC W2019🤞, acquiring a premium domain💰, meeting Substack's @hamishmckenzie and Stripe CEO @patrickc 🤩

2/ So what is Brew?

brew / bru : / to make (beer, coffee etc.) / verb: begin to develop 🌱

A place for you to enjoy premium content while supporting your favorite creators. Sort of like a ‘Consumer-facing Patreon’ cc @jackconte

(we’re still working on the pitch)

3/ So, why be so transparent? Two words: launch strategy.

jk 😅 a) I loooove doing something consistently for a long period of time b) limited downside and infinite upside (feedback, accountability, reach).

cc @altimor, @pmarca

4/ https://t.co/GOQJ7LjQ2t domain 🍻

It started with a cold email. Guess what? He was using BuyMeACoffee on his blog, and was excited to hear about what we're building next. Within 2w, we signed the deal at @Escrowcom's SF office. You’re a pleasure to work with @MichaelCyger!

5/ @ycombinator's invite for the in-person interview arrived that evening. Quite a day!

Thanks @patio11 for the thoughtful feedback on our YC application, and @gabhubert for your directions on positioning the product — set the tone for our pitch!

Week 1 highlights: getting shortlisted for YC W2019🤞, acquiring a premium domain💰, meeting Substack's @hamishmckenzie and Stripe CEO @patrickc 🤩

2/ So what is Brew?

brew / bru : / to make (beer, coffee etc.) / verb: begin to develop 🌱

A place for you to enjoy premium content while supporting your favorite creators. Sort of like a ‘Consumer-facing Patreon’ cc @jackconte

(we’re still working on the pitch)

3/ So, why be so transparent? Two words: launch strategy.

jk 😅 a) I loooove doing something consistently for a long period of time b) limited downside and infinite upside (feedback, accountability, reach).

cc @altimor, @pmarca

4/ https://t.co/GOQJ7LjQ2t domain 🍻

It started with a cold email. Guess what? He was using BuyMeACoffee on his blog, and was excited to hear about what we're building next. Within 2w, we signed the deal at @Escrowcom's SF office. You’re a pleasure to work with @MichaelCyger!

5/ @ycombinator's invite for the in-person interview arrived that evening. Quite a day!

Thanks @patio11 for the thoughtful feedback on our YC application, and @gabhubert for your directions on positioning the product — set the tone for our pitch!