One segment I have been absolutely upbeat is IT/Tech. Tech has always been the hidden moat for many companies - AP/BFL to name a few. Tech is no longer a vertical in market. It has become horizontal that cuts across every single vertical.

More from Ameya

After getting good feedback on yesterday's thread on #routemobile I think it is logical to do a bit in-depth technical study. Place #twilio at center, keep #routemobile & #tanla at the periphery & see who is each placed.

This thread is inspired by one of the articles I read on the-ken about #postman API & how they are transforming & expediting software product delivery & consumption, leading to enhanced developer productivity.

We all know that #Twilio offers host of APIs that can be readily used for faster integration by anyone who wants to have communication capabilities. Before we move ahead, let's get a few things cleared out.

Can anyone build the programming capability to process payments or communication capabilities? Yes, but will they, the answer is NO. Companies prefer to consume APIs offered by likes of #Stripe #twilio #Shopify #razorpay etc.

This offers two benefits - faster time to market, of course that means no need to re-invent the wheel + not worrying of compliance around payment process or communication regulations. This makes entire ecosystem extremely agile

So I have been studying this entire communication layer as its relevance is ever growing with more devices coming online, staying connected, and relying on real-time communication. Not that this domain under penetrated, but there is a change underway.

— Ameya (@Finstor85) February 10, 2021

This thread is inspired by one of the articles I read on the-ken about #postman API & how they are transforming & expediting software product delivery & consumption, leading to enhanced developer productivity.

We all know that #Twilio offers host of APIs that can be readily used for faster integration by anyone who wants to have communication capabilities. Before we move ahead, let's get a few things cleared out.

Can anyone build the programming capability to process payments or communication capabilities? Yes, but will they, the answer is NO. Companies prefer to consume APIs offered by likes of #Stripe #twilio #Shopify #razorpay etc.

This offers two benefits - faster time to market, of course that means no need to re-invent the wheel + not worrying of compliance around payment process or communication regulations. This makes entire ecosystem extremely agile

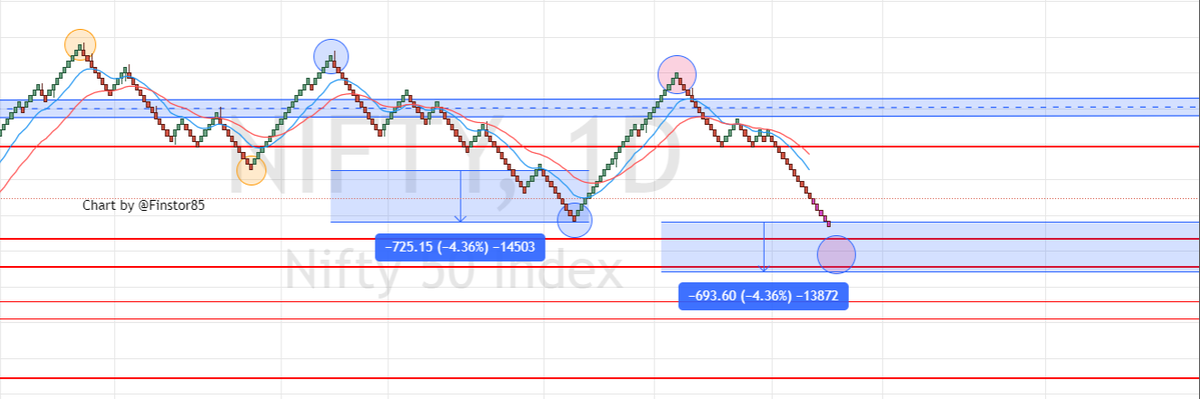

and we are in the range now! 15282 is the low of the range. I start buying between 15666-15282. Big Q is, will we stop in the range & reverse? Honestly, I don't know. All I know is range is here, deserves some allocation in core conviction ideas. #niftymasterchart https://t.co/RXuJb0dTWi

If we are to continue LH-LL setup & break 16666 on daily we will finally complete this drag near 15214. I am not bearish. In fact, this should give amazing opportunity to buy. Until then 16666-17300 continue to provide L-H range for traders. pic.twitter.com/tfIq00VJmZ

— Ameya (@Finstor85) May 2, 2022

More from Tech

I could create an entire twitter feed of things Facebook has tried to cover up since 2015. Where do you want to start, Mark and Sheryl? https://t.co/1trgupQEH9

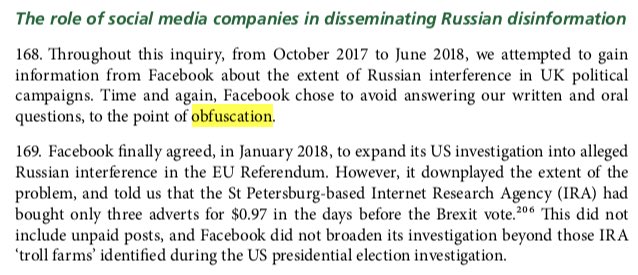

Ok, here. Just one of the 236 mentions of Facebook in the under read but incredibly important interim report from Parliament. ht @CommonsCMS https://t.co/gfhHCrOLeU

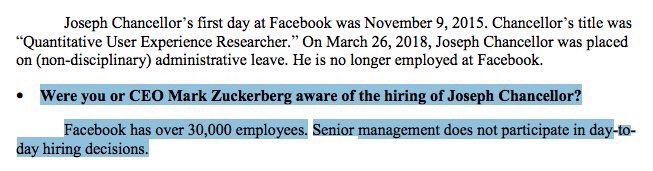

Let’s do another, this one to Senate Intel. Question: “Were you or CEO Mark Zuckerberg aware of the hiring of Joseph Chancellor?"

Answer "Facebook has over 30,000 employees. Senior management does not participate in day-today hiring decisions."

Or to @CommonsCMS: Question: "When did Mark Zuckerberg know about Cambridge Analytica?"

Answer: "He did not become aware of allegations CA may not have deleted data about FB users obtained through Dr. Kogan's app until March of 2018, when

these issues were raised in the media."

If you prefer visuals, watch this short clip after @IanCLucas rightly expresses concern about a Facebook exec failing to disclose info.

Ok, here. Just one of the 236 mentions of Facebook in the under read but incredibly important interim report from Parliament. ht @CommonsCMS https://t.co/gfhHCrOLeU

Let’s do another, this one to Senate Intel. Question: “Were you or CEO Mark Zuckerberg aware of the hiring of Joseph Chancellor?"

Answer "Facebook has over 30,000 employees. Senior management does not participate in day-today hiring decisions."

Or to @CommonsCMS: Question: "When did Mark Zuckerberg know about Cambridge Analytica?"

Answer: "He did not become aware of allegations CA may not have deleted data about FB users obtained through Dr. Kogan's app until March of 2018, when

these issues were raised in the media."

If you prefer visuals, watch this short clip after @IanCLucas rightly expresses concern about a Facebook exec failing to disclose info.

A company as powerful as @facebook should be subject to proper scrutiny. Mike Schroepfer, its CTO, told us that the buck stops with Mark Zuckerberg on the Cambridge Analytica scandal, which is why he should come and answer our questions @DamianCollins @IanCLucas pic.twitter.com/0H4VMhtIFu

— Digital, Culture, Media and Sport Committee (@CommonsCMS) May 23, 2018

Recently, the @CNIL issued a decision regarding the GDPR compliance of an unknown French adtech company named "Vectaury". It may seem like small fry, but the decision has potential wide-ranging impacts for Google, the IAB framework, and today's adtech. It's thread time! 👇

It's all in French, but if you're up for it you can read:

• Their blog post (lacks the most interesting details): https://t.co/PHkDcOT1hy

• Their high-level legal decision: https://t.co/hwpiEvjodt

• The full notification: https://t.co/QQB7rfynha

I've read it so you needn't!

Vectaury was collecting geolocation data in order to create profiles (eg. people who often go to this or that type of shop) so as to power ad targeting. They operate through embedded SDKs and ad bidding, making them invisible to users.

The @CNIL notes that profiling based off of geolocation presents particular risks since it reveals people's movements and habits. As risky, the processing requires consent — this will be the heart of their assessment.

Interesting point: they justify the decision in part because of how many people COULD be targeted in this way (rather than how many have — though they note that too). Because it's on a phone, and many have phones, it is considered large-scale processing no matter what.

It's all in French, but if you're up for it you can read:

• Their blog post (lacks the most interesting details): https://t.co/PHkDcOT1hy

• Their high-level legal decision: https://t.co/hwpiEvjodt

• The full notification: https://t.co/QQB7rfynha

I've read it so you needn't!

Vectaury was collecting geolocation data in order to create profiles (eg. people who often go to this or that type of shop) so as to power ad targeting. They operate through embedded SDKs and ad bidding, making them invisible to users.

The @CNIL notes that profiling based off of geolocation presents particular risks since it reveals people's movements and habits. As risky, the processing requires consent — this will be the heart of their assessment.

Interesting point: they justify the decision in part because of how many people COULD be targeted in this way (rather than how many have — though they note that too). Because it's on a phone, and many have phones, it is considered large-scale processing no matter what.

"I really want to break into Product Management"

make products.

"If only someone would tell me how I can get a startup to notice me."

Make Products.

"I guess it's impossible and I'll never break into the industry."

MAKE PRODUCTS.

Courtesy of @edbrisson's wonderful thread on breaking into comics – https://t.co/TgNblNSCBj – here is why the same applies to Product Management, too.

There is no better way of learning the craft of product, or proving your potential to employers, than just doing it.

You do not need anybody's permission. We don't have diplomas, nor doctorates. We can barely agree on a single standard of what a Product Manager is supposed to do.

But – there is at least one blindingly obvious industry consensus – a Product Manager makes Products.

And they don't need to be kept at the exact right temperature, given endless resource, or carefully protected in order to do this.

They find their own way.

make products.

"If only someone would tell me how I can get a startup to notice me."

Make Products.

"I guess it's impossible and I'll never break into the industry."

MAKE PRODUCTS.

Courtesy of @edbrisson's wonderful thread on breaking into comics – https://t.co/TgNblNSCBj – here is why the same applies to Product Management, too.

"I really want to break into comics"

— Ed Brisson (@edbrisson) December 4, 2018

make comics.

"If only someone would tell me how I can get an editor to notice me."

Make Comics.

"I guess it's impossible and I'll never break into the industry."

MAKE COMICS.

There is no better way of learning the craft of product, or proving your potential to employers, than just doing it.

You do not need anybody's permission. We don't have diplomas, nor doctorates. We can barely agree on a single standard of what a Product Manager is supposed to do.

But – there is at least one blindingly obvious industry consensus – a Product Manager makes Products.

And they don't need to be kept at the exact right temperature, given endless resource, or carefully protected in order to do this.

They find their own way.

Ok, I’ve told this story a few times, but maybe never here. Here we go. 🧵👇

I was about 6. I was in the car with my mother. We were driving a few hours from home to go to Orlando. My parents were letting me audition for a tv show. It would end up being my first job. I was very excited. But, in the meantime we drove and listened to Rush’s show.

There was some sort of trivia question they posed to the audience. I don’t remember what the riddle was, but I remember I knew the answer right away. It was phrased in this way that was somehow just simpler to see from a kid’s perspective. The answer was CAROUSEL. I was elated.

My mother was THRILLED. She insisted that we call Into the show using her “for emergencies only” giant cell phone. It was this phone:

I called in. The phone rang for a while, but someone answered. It was an impatient-sounding dude. The screener. I said I had the trivia answer. He wasn’t charmed, I could hear him rolling his eyes. He asked me what it was. I told him. “Please hold.”

Wish I had the audio of Rush Limbaugh telling me off on the phone on his show when I was six. In the meantime, RIP.

— Shannon Woodward (@shannonwoodward) February 17, 2021

I was about 6. I was in the car with my mother. We were driving a few hours from home to go to Orlando. My parents were letting me audition for a tv show. It would end up being my first job. I was very excited. But, in the meantime we drove and listened to Rush’s show.

There was some sort of trivia question they posed to the audience. I don’t remember what the riddle was, but I remember I knew the answer right away. It was phrased in this way that was somehow just simpler to see from a kid’s perspective. The answer was CAROUSEL. I was elated.

My mother was THRILLED. She insisted that we call Into the show using her “for emergencies only” giant cell phone. It was this phone:

I called in. The phone rang for a while, but someone answered. It was an impatient-sounding dude. The screener. I said I had the trivia answer. He wasn’t charmed, I could hear him rolling his eyes. He asked me what it was. I told him. “Please hold.”

You May Also Like

And here they are...

THE WINNERS OF THE 24 HOUR STARTUP CHALLENGE

Remember, this money is just fun. If you launched a product (or even attempted a launch) - you did something worth MUCH more than $1,000.

#24hrstartup

The winners 👇

#10

Lattes For Change - Skip a latte and save a life.

https://t.co/M75RAirZzs

@frantzfries built a platform where you can see how skipping your morning latte could do for the world.

A great product for a great cause.

Congrats Chris on winning $250!

#9

Instaland - Create amazing landing pages for your followers.

https://t.co/5KkveJTAsy

A team project! @bpmct and @BaileyPumfleet built a tool for social media influencers to create simple "swipe up" landing pages for followers.

Really impressive for 24 hours. Congrats!

#8

SayHenlo - Chat without distractions

https://t.co/og0B7gmkW6

Built by @DaltonEdwards, it's a platform for combatting conversation overload. This product was also coded exclusively from an iPad 😲

Dalton is a beast. I'm so excited he placed in the top 10.

#7

CoderStory - Learn to code from developers across the globe!

https://t.co/86Ay6nF4AY

Built by @jesswallaceuk, the project is focused on highlighting the experience of developers and people learning to code.

I wish this existed when I learned to code! Congrats on $250!!

THE WINNERS OF THE 24 HOUR STARTUP CHALLENGE

Remember, this money is just fun. If you launched a product (or even attempted a launch) - you did something worth MUCH more than $1,000.

#24hrstartup

The winners 👇

#10

Lattes For Change - Skip a latte and save a life.

https://t.co/M75RAirZzs

@frantzfries built a platform where you can see how skipping your morning latte could do for the world.

A great product for a great cause.

Congrats Chris on winning $250!

#9

Instaland - Create amazing landing pages for your followers.

https://t.co/5KkveJTAsy

A team project! @bpmct and @BaileyPumfleet built a tool for social media influencers to create simple "swipe up" landing pages for followers.

Really impressive for 24 hours. Congrats!

#8

SayHenlo - Chat without distractions

https://t.co/og0B7gmkW6

Built by @DaltonEdwards, it's a platform for combatting conversation overload. This product was also coded exclusively from an iPad 😲

Dalton is a beast. I'm so excited he placed in the top 10.

#7

CoderStory - Learn to code from developers across the globe!

https://t.co/86Ay6nF4AY

Built by @jesswallaceuk, the project is focused on highlighting the experience of developers and people learning to code.

I wish this existed when I learned to code! Congrats on $250!!

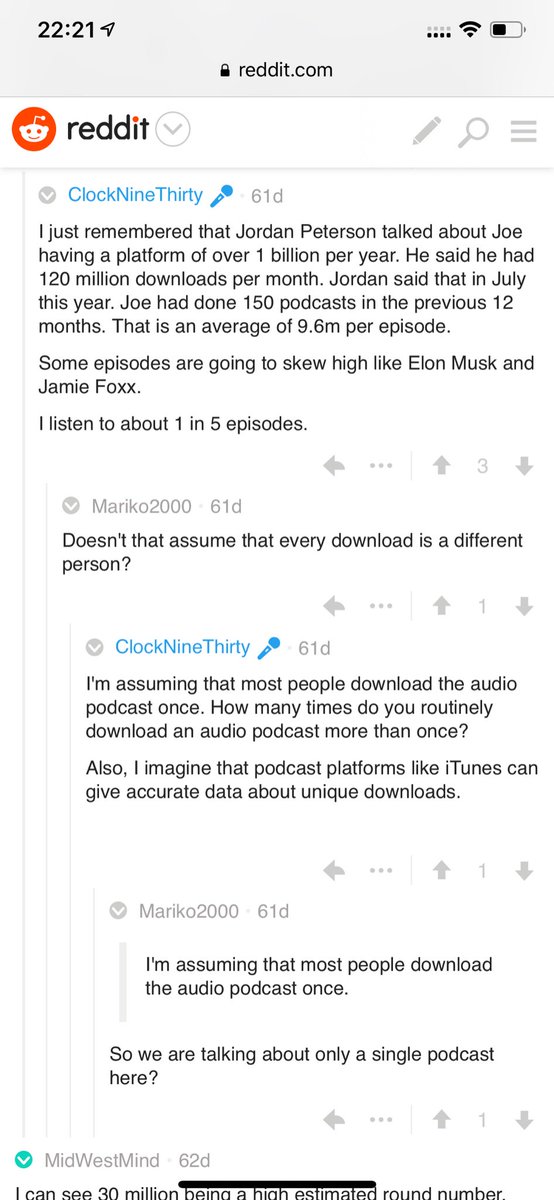

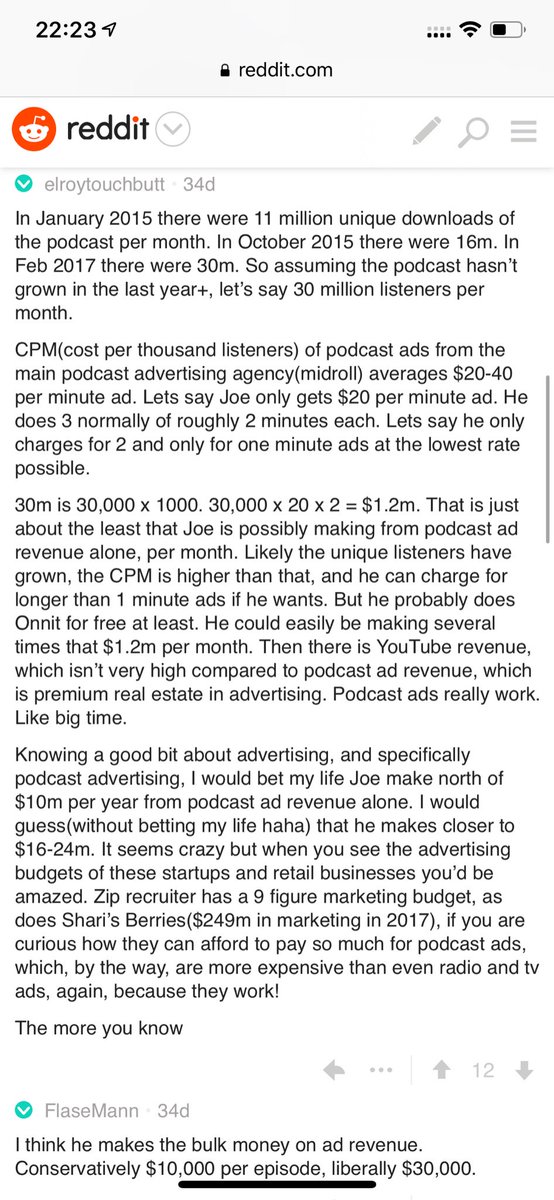

Joe Rogan's podcast is now is listened to 1.5+ billion times per year at around $50-100M/year revenue.

Independent and 100% owned by Joe, no networks, no middle men and a 100M+ people audience.

👏

https://t.co/RywAiBxA3s

Joe is the #1 / #2 podcast (depends per week) of all podcasts

120 million plays per month source https://t.co/k7L1LfDdcM

https://t.co/aGcYnVDpMu

Independent and 100% owned by Joe, no networks, no middle men and a 100M+ people audience.

👏

https://t.co/RywAiBxA3s

Joe is the #1 / #2 podcast (depends per week) of all podcasts

120 million plays per month source https://t.co/k7L1LfDdcM

https://t.co/aGcYnVDpMu