Everytime Punit sir tweets I have to read it thrice.

There is so much knowledge and free research available in every single tweet of his✌🏻👌🏼

The demand for specialty alcohols (ethanol) used in a wide range of consumer & commercial products has risen in global market\U0001f9ec

— Punit (@punitbansal14) August 3, 2021

Image 1: US annual sales of cleaning products ($bn)

Image 2: Industry value chain in Pharma & Agro

Image 3: Speciality alcohol business (8% MS)\U0001f1ee\U0001f1f3 https://t.co/3GyFDONwqA pic.twitter.com/EqheflcWEJ

More from Tar ⚡

ROCE 1 Yr: 32.7%

ROCE 3 Yr: 24.8%

ROE: 27.4%

ROE 3 Yr: 19%

Op Margin: 28.4%

Reserves: 32% of Current Market Cap

Debt: Nil

Profit CAGR 3Yrs: 54%

Debtor Days: 15

Inventory Turnover > 5

CFO YoY Increase : 160%

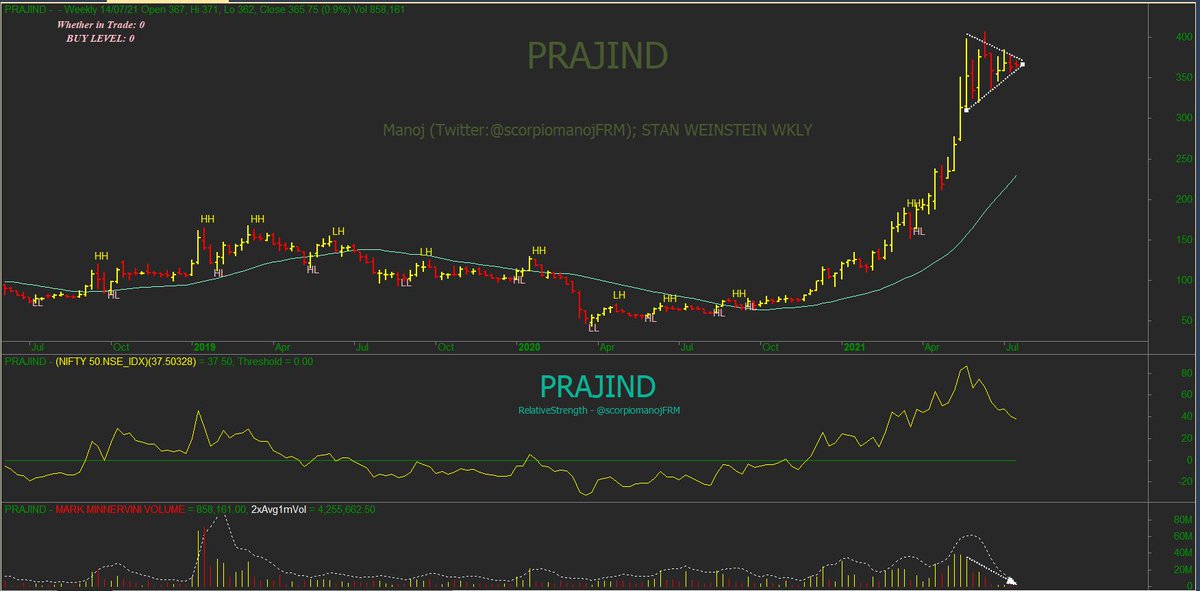

Some of you got it correct. Its Anjali Portland.

The company just acquired another cement company that will double the total sales immediately.

https://t.co/2xVnpJapPy

The acquisition was financed by adding debt, so interest costs from next quarter will go up but still great!

For a company that operates in a cyclical sector like cement!

What I liked is that the company was able to maintain the balance sheet and margins even in a down cycle.

With real estate sector reviving, this can be a great bet from here.

No recommendations, just an observation.

Market started re-rating the stock as soon as they announced acquisition.

Someone did some work on details of acquisition, sharing the thread

@drprashantmish6 @Investor_Mohit

— Arun Choudhary FCA (@YOUNGBRUJ) July 9, 2021

1) Information on cement sector in India

India at 550 MTPA is the 2nd largest cement producer globally. Expected to move to 650 MTPA by 2025E pic.twitter.com/GqtcSk03TU

Please do your due diligence and do not copy me blindly here

My investments in IEX are part of an experiment to hold a good stock for 10 yrs + buying sporadically

IEX has also started ground work for trading carbon credits

Still believe this is one stock where dividend every year in 10 years can be equal to my entire investment amount considering it throws up so much cash

Still maintain

NSE + Zerodha =

#IEX in my PF is a giant growing dividend paying Gorilla

— Tar \u26a1 (@itsTarH) October 18, 2021

Main reason I don't mess around with my holdings is cause I expect it to.

Pay Dividend = to my investment within the next decade

Glad they are considering Bonus Issue (tax favorable) instead of Cash Dividend. pic.twitter.com/2cLt6yK0Xw