GLS is a leading developer and manufacturer of select high-value, non-commoditized APIs in chronic therapeutic areas, including CVS, CNS, pain, and diabetes;

As of FY21, API and CDMO contributed ~90.6 & 8.1% to GLS revenues respectively;

2/25

The company works with 16 of the top 20 generic pharma companies in the world and as of 31st May 2021, they have registered ~403 DMFs globally;

From the IPO proceeds, GLS will be using ~Rs 8bn as repayment of an outstanding purchase agreement to the promoter-

3/25

-for the spin-off of the API business. The company has also envisaged using Rs 1.53bn as capital expenditure;

This includes a new multi-usage facility, which will mainly focus on the company’s CDMO business aspiration from 4QFY23.

4/25

Key growth drivers for the Indian API industry:

👉India is on par with other countries in terms of technological capabilities and process efficiency;

👉The costs are very low in India: Domestic pharmaceutical facilities cost only 2/5th of what it costs to set up and-

5/25

👉China+1 strategy: In 2020, according to the DRHP, an estimated 40% of all factories in China have shut down -resulting in supply disruptions and higher costs. This has caused several major pharma countries to reconsider and reshuffle their API import sources.

6/25

👉Favorable labor cost: The cost of labor in China has more than doubled, from 5.2% of the total direct manufacturing cost to 10.6%, while in India, it has decreased from 6.1% to 5% (2015 data).

7/25

👉Largest US DMF filers: The fact that India has the largest percentage of DMFs filed in the US (15%) and the highest number of USFDA-approved API facilities is a significant ‘first-mover' advantage.

8/25

👉High Potent API could be a key driver: With a large no. of synthetic drugs' patents set to expire, a growing no. of small molecules in clinical trials, & a steady increase in contract manufacturing & research services, synthetic chemical API will continue to expand in India.

👉Government assistance: 1) Investments in Bulk Drug parks worth Rs 99.4bn, 2) PLI schemes, 3) Raising the FDI cap & 4) developing a new intellectual property rights (IPR) strategy to encourage innovation.

10/25

Glenmark LS API Business:

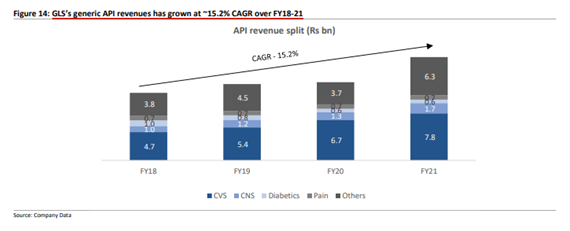

CVS is the largest segment with a 43% revenue share: Glenmark LS derives its API revenue from 5 key segments namely CVS, CNS, Diabetes, Pain & Others;

11/25

CVS is the largest segment for GLS in API as it makes up ~45% of FY21 API sales With key products being Olmesartan, Amiodarone, Telmisartan, Perindopril, Rosuvastatin and Cilostazo;

12/25

Other key segments include CNS, Diabetics, and Pain that contributed 9.8%, 3.6% & 4.1% of API sales, respectively.

13/25

In the near term, the company has announced its vision for growth by,

1) Diversifying customer base in existing markets and expanding its presence in semi-regulated markets like South Korea, Taiwan, Russia, Brazil, Mexico, and Saudi Arabia.

14/25

In these markets, the company will look for local partnerships;

2) Strive for improvement in market share increase in existing products;

3) New product launches which include complex API portfolios in Oncology, Peptides, and Iron Compounds.

15/25

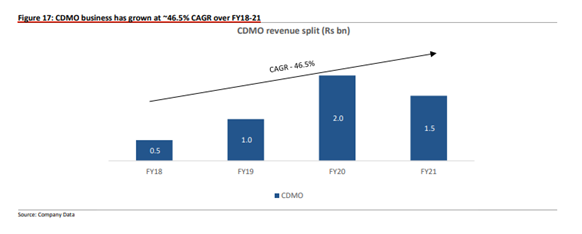

CDMO - Another growth driver:

In the last 3 years, GLS has started working with innovator companies for CDMO opportunities;

Due to this, the company was able to grow its business by 1.5-2x between 2018-21;

16/25

The company is also looking at the specialty business as it offers higher margins while the complex nature of the products leads to high customer stickiness.

17/25

Manufacturing:

3 of the 4 plants are USFDA approved;

Future CAPEX plans:

Plans to utilize ~Rs 1.53bn from the IPO proceeds towards CAPEX; includes enhancing the production capacity of Ankleshwar (FY22) and Dahej (in FY22&23) facilities to an aggregate annual capacity of 200KL.

The company says the expansion will help increase their generic API pipeline and grow the company’s Onco product pipeline;

Additionally, Glenmark LS will put up a new manufacturing facility, which is expected to be commercialized in 4QFY23;

19/25

The facility will be used primarily for the CDMO business and aid the company’s generic manufacturing API needs.

Financials:

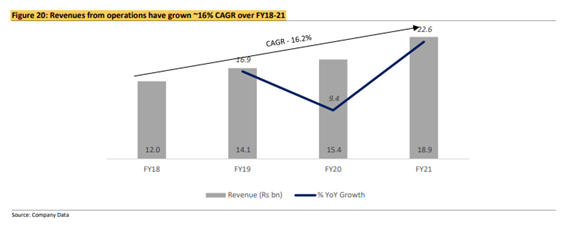

Revenue, EBITDA and PAT grew ~16%, 21% and 15% CAGR (FY18-21) respectively: In FY21, GLS’s operating revenue grew ~23% YoY to Rs 18.9bn.

20/25

The growth was primarily due to a ~32% YoY increase in the generic API business. The increase in the API business was due to the company’s expansion in EM and growth in regulated markets

21/25

Key Strengths (as mentioned in the RHP):

Leadership in Select High Value, Non-Commoditized APIs in Chronic Therapeutic Areas: Key products in the company’s portfolio include Atovaquone, Perindopril, Adapalene, and Zonisamide;

22/25

GLS holds a ~30% market share in these products & they contributed ~40% of the company’s FY20 sales;

Since 2015, company has been subjected to 37 regulatory audits (includes USFDA, Health Canada, & European agencies) & has not received any warning letters in this period;

23/25

In the last 3 years, the company’s R&D spends ranged between 2-3% of total sales; GLS employs ~213 people in its R&D division, which constitutes ~14% of total employee strength;

Key Concerns:

Regulatory Risk: In FY21, ~65% of sales come from regulated markets;

24/25

Dependence on key customers: GLS derives ~55.88% from its top 5 customers as of FY21;

Dependence on key products: As of FY21, the company derives ~66.36% of its revenues from its top 10 products in the generic API segment.

End of thread🧵

25/25