1️⃣

First and foremost, sole reason for investing in National Pension Scheme:

💡tax saving and there by a place in retirement portfolio.

If you are investing in NPS for any other purpose, you are doing it wrong.

2️⃣

Two types of NPS Account - Tier I & Tier II

👉 Tier I Account: lock in account

👉 Tier II Account: invest and withdraw at will

Tier I Account is the account where all tax deductions are applicable.

Nothing in Tier II. Do not even open, it's useless.

To all NPS Tier II subscribers who have collectively subscribed ~ 3575 Crore:

1) Are you getting any tax benefits by investing in Tier II? No

2) Are you saving for retirement? It can be done through Mutual Funds!

3) Are you getting credit card rewards? It has stopped. 😄

3️⃣

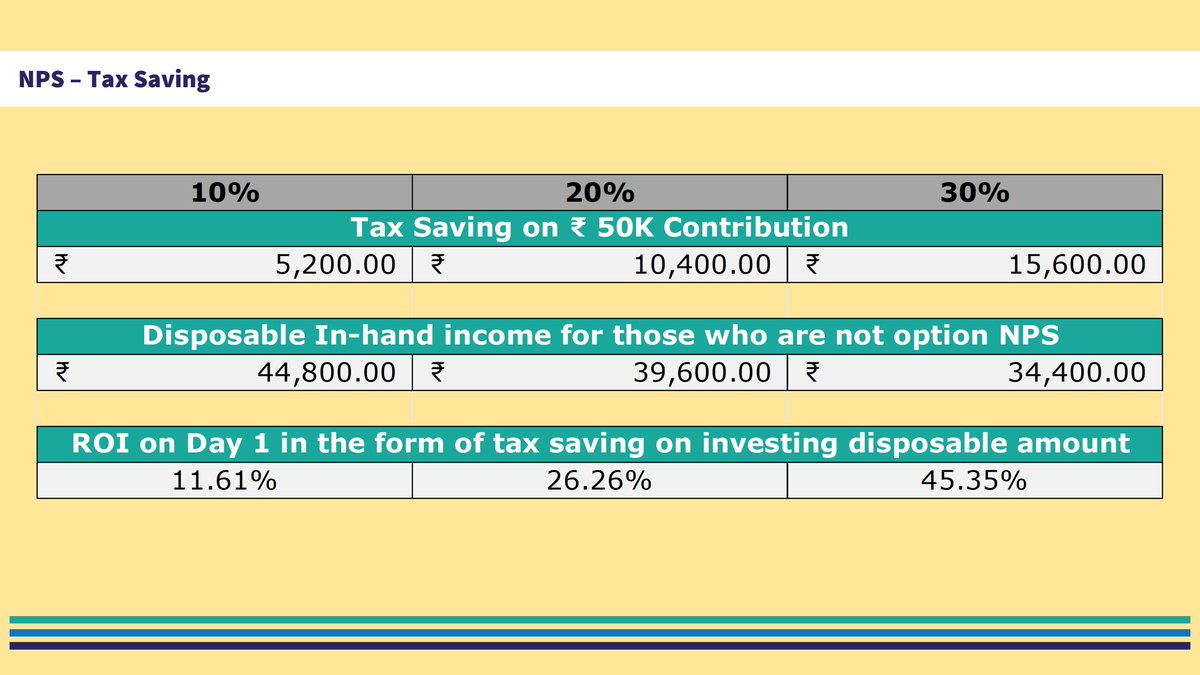

Tax Saving can be done in three sections

80CCD(1)

80CCD(1B)

80CCD(2)

80CCD(1)

This has a limit of 1.5 Lakh and is not over and above 80C Limit.

It is useful only for central government employees. Private Sector Employees and Self Employed have a lot of options for 80C - 1.5L

80CCD(1B)

This section provides additional deduction of ₹ 50K over and above 80C limit of ₹ 1.5 lakh.

All India Citizens - residents and NRIs can claim deduction under this section.

80CCD(2)

🤩 That should be the reaction of corporate employees who have the option of contributing in NPS through Employer.

So, employees can invest through their employer up to 10% of their Basic + DA. This amount will be tax deductible. Is there any capping for it, Yes.

There is a cap of 7.5 Lakhs, which includes contribution from employer towards EPF, NPS and any other superannuation fund.

the employer's contribution in excess of ₹ 7.50 lakh will be treated as perquisite and will be added to salary of the subscriber and taxed at slab rate.

4️⃣

NPS gives two options to choose from

Active Choice & Auto Choice

basically it gives you an option to choose asset allocation of your investments within four asset classes:

Equity → E

Corporate Bond → C

Government Sec → G

Alternate Investment Fund → A

Active Choice:

You can choose the asset allocation subject to the following capping:

E should be less than or equal to 75%

A should be less than or equal to 5%

75% is maximum permitted equity allocation up to the age of 50 years, thereafter it goes down 2.5% every year till it reaches 50% at 60 years. The tapering off in equity allocation is done on birth date of the subscriber.

Auto Choice:

Three Lifecycle funds, in all three equity starts tapering down at the age of 36.

LC75 - Aggressive Life Cycle Fund: up to 35 years - 75% equity thereafter, equity starts coming down and reach 15% by the age of 55 years.

LC50 - Moderate Life Cycle Fund: up to 35 years - 50% equity thereafter, equity starts coming down and reach 10% by the age of 55 years.

LC25 - Conservative Life Cycle Fund: up to 35 years - 25% equity thereafter, equity starts coming down and reach 5% by the age of 55 years.

Always choose Active Choice, with maximum equity and remaining in Corporate Bonds or Government Bonds.

Ignore the Alternate Investments:

Currently the portfolios of REITs, InvITs and Perpetual Bonds.

5️⃣

NPS has EEE Status but with a twist.

You get tax exemption for invested amount

the growth of capital is also tax exempt

and the maturity proceeds are also tax exempt

BUT

40% of the maturity proceeds needs to be invested in a pension bearing annuity.

Those who are in their 20s and 30s and even in 40s, please note, there is a long period before the lock-in ends, so it is very likely that annuity may get replaced by something like Systematic Withdrawal Plan. Need not worry about it.

Invest and start saving taxes.

6️⃣

You can withdraw the money from NPS at the age of 60 or superannuation (means: retirement age, mostly 58 or 60).

You have three options:

1) At 60, exit full.

take 60% lumpsum and invest the 40% in annuity

2) Continuation

You can invest till 70 years of age and extend till 75. Need to make minimum contribution of ₹ 6000 every year.

3) Deferment

You can defer the withdrawal and withdraw anytime before 75.

You can defer only the annuity withdrawal or lumpsum withdrawal.

It doesn't make any sense to withdraw the annuity component at 60. Let it grow till 75.

Reason: Annuities are very return inefficient.

7️⃣

👉 If you are in 50s, there is a trick.

If total accumulated corpus is less than or equal to ₹ 5 Lakh, one can withdraw 100% lumpsum

Start Contributing in NPS, choose 100% G as asset class, save taxes, withdraw everything at 60

You can use this option for 80CCD(1) as well

👉 If your employers doesn't have corporate NPS option. Please request your HR to make it available.

Our clients have got it done in their organization are now saving decent amount of taxes.

👉 If you are a small entrepreneur and are worried that you don't have the option to invest in corporate NPS, then get your company registered in corporate NPS.

Company can claim expense and you will not be taxed.

(one of our client has done it without our advise, salute to RH)

👉 low cost proponents, this is for you.

None of the Pension Fund manager has beaten the benchmark on 6 months, 1,2,3,5,7,10 years.

Tier I

Invest only that amount which gives you tax deductions. And don't forget the lock-in and Annuity thing.

Tier II

Don't open

👉 If you are NRI and want to retire outside India, don't do NPS.

a) the moment citizen status changes, NPS account will be closed.

b) ₹50K per annum will not make decent corpus for your heirs to come to India for settlement of Account.

8️⃣

You need to maintain balance between liquidity, tax saving, long term goals and loan repayments.

This is more of a personal finance thing but it is important that I say it here.

Real Life Case:

If you are 27, single parent, sole bread earner of the family, about to get married in another 4-6 months, need to fund the education of younger sibling.. NPS is not for you.

Don't focus on on tax saving / retirement planning through NPS, there is a long lock-in

Immediate Focus should be on insurances, creating enough liquidity for siblings education, own marriage, health care fund for family and creating a decent emergency fund.

once your sibling starts working, you can focus on long term goals including NPS.

Last week, I wrote about Health Insurance

https://t.co/c4cdT79Spj