Why #JubilantIngrevia can be next big growth story?

Here is the thread.

Pharma serving to regulated market are under stress due product price erosion. Market is comfortably giving higher multiples to step down segment in value chain i.e. raw material suppliers.

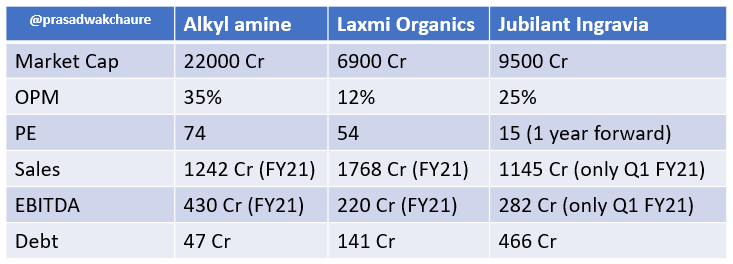

Jubilant Ingravia has posted superb Q1 numbers which fetched my attention. Stock is trading below one year forward 15x PE multiples & 2x of sales.

Key points:

Super diversified product & client portfolio

Leadership position for many products in India and in the World

Last year company reduced debt by 600 Cr while lined up 900 Cr Capex for next 3 years

1.Molasses to Ethanol to Acetaldehyde to Pyridine derivatives to Nutritional products

2.Ethanol to acetic anhydride

3.Ethanol to ethyl acetate

4. Ethanol to acetic acid to ketene to Diketene

https://t.co/8ZAj2kgcHE

Research report by @VineetGala is nice read

https://t.co/R1pKR7CbMg