What I will share are some of the output from a simple model for US 10-year Treasury bond yields.

1/n

I am working on a paper on why interest rates and yields are as low as they are. I will share some preliminary results here.

What I will share are some of the output from a simple model for US 10-year Treasury bond yields.

It is key to me that the model not only is statistically significantly, but is also economically significant. We need to understand economic developments within economic theory.

I have estimated a model for the US 10-year bond yield based on the following fundamental variables.

This of course captures the standard textbook relationship from growth theory (the Solow model) in which there is a positive relationship between real interest rates and real GDP as well as the Fischer equation where nominal interest rates are positive related to inflation.

Population growth (and demographics in general) should be expected to impact yields through numerous channels.

I would particularly highlight the impact on growth, risk appetite and savings. Overall we should expect higher population growth to increase yields.

This reflects the compensation investors would demand for lack of credibility of monetary policy.

This is measure of the slack in the US economy and should overall capture the US business cycle.

Futuremore, I have been playing around with different meausre of debt and leverage in the US economy - both private and public debt. None of these variables however, seem to have a statistically significant impact on US yields and rates.

The reason for this might be that these factors are correlated with growth, inflation and demographics.

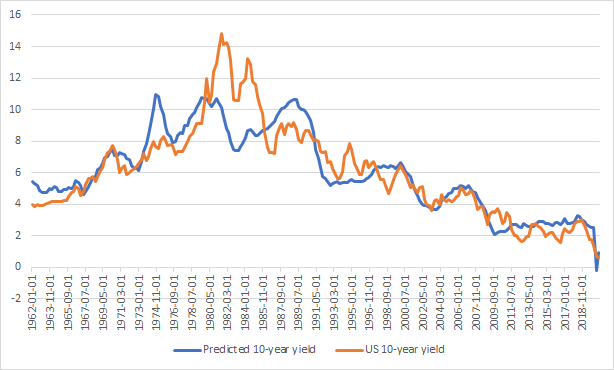

The graph below shows 10-years US yields and the predicted model.

We see the model has quite a good fit over the past nearly 60 years.

We also see that there are some well-known different periods - for example the Great Inflation of the 1970s when yields reached historically high levels and the present period where yields are very low.

I have looked at the following four periods:

The Great Inflation (1967-82)

Disinflation (1982-1992)

The Great Moderation (1992-2008)

The Great Stagnation (2008-today)

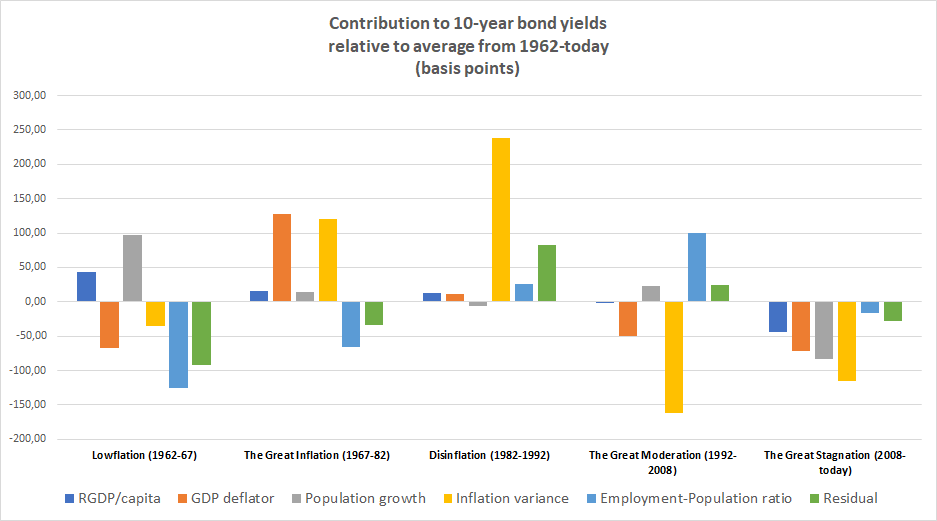

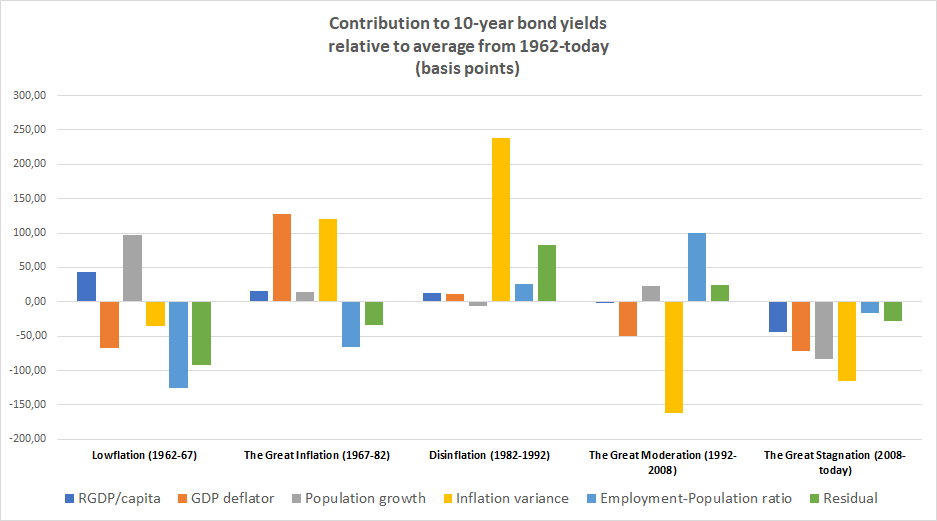

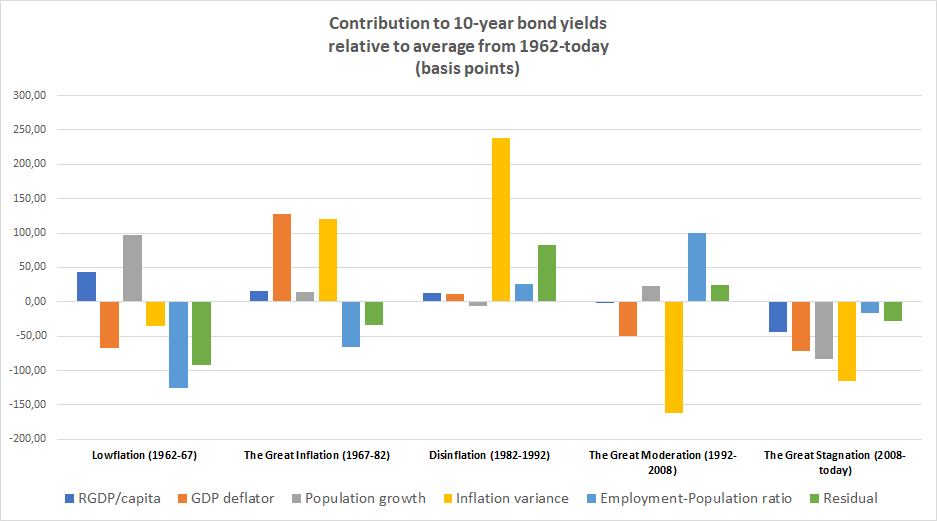

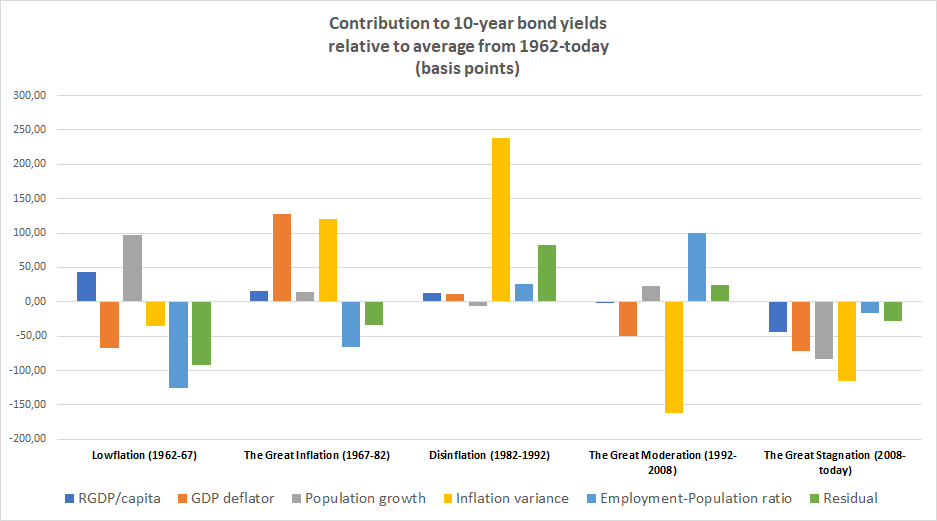

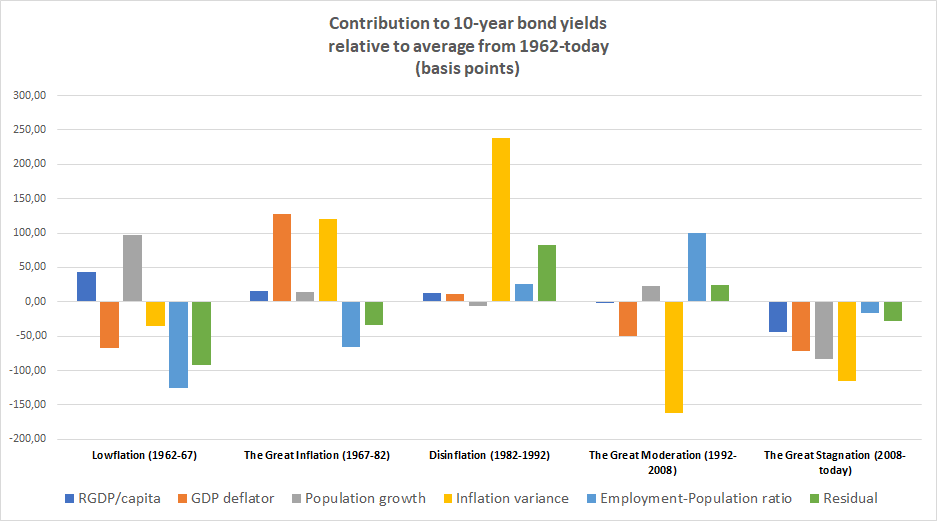

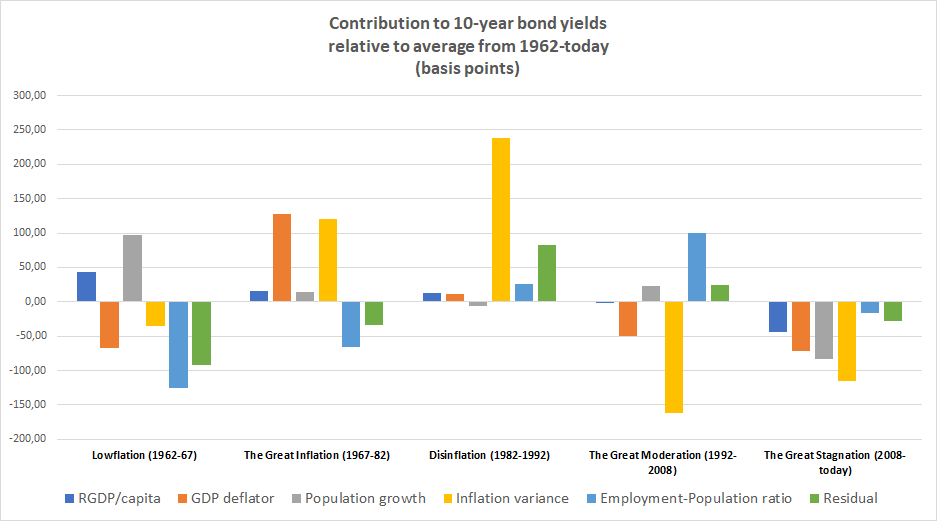

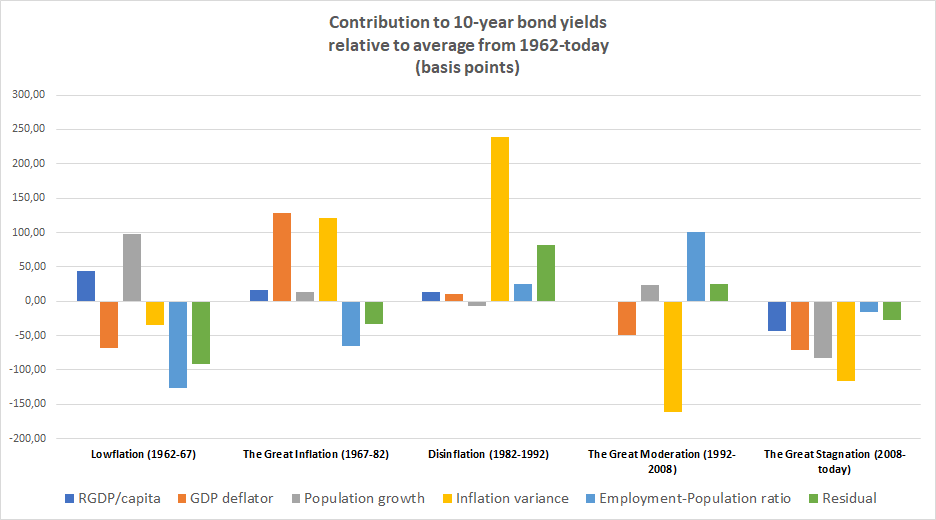

The table below shows the decomposition of the contribution (basis points) to yields from the different factors in the models (note we split NGDP between RGDP growth and inflation).

The decomposition is done RELATIVE to the average impact on yields during the period from 1962 and until today.

Lowflation (1962-67)

During this period yields and rate where low relative to the historical average for the whole estimation period.

We that during the Lowflation period inflation was as was inflation variance. Hence, we had a period of nominal stability as well as some slack in the US economy with higher population growth than employment growth.

...

Higher RGDP/cap growth and pop. growth on the other hand were contributing to higher yields during the lowflation period but the other factors where stronger resulting in overall low yields in this period.

The Great Inflation started around 1967 and ended around 1982.

During this period US-yields and rates rose to historically high levels and the main driver was significant monetary instability with rising and volatile US inflation.

It is notable that during this period not only higher inflation pushed up yields, but equally inflation variance contributed to a similar degree to higher yields. We here see that the lose of monetary policy credibility is very costly.

In 1979 Paul Volcker became Federal Reserve chairman and the following year initiated an effort to reestablish monetary policy credibility and to push down inflation.

However, we here date the disinflation period from 1982 and until 1992.

The Fed's efforts paid off and inflation dropped markedly during this period relative to the Great Inflation period.

However, it is notable that bond yields did not immediately drop to reflect 1-to-1 and inflation variance - measured as 10-year moving variance in quarter/quarter changes in the GDP deflation remained high.

One can of course discuss this measure, but it seems to pretty well capture the fact that it took time to gain credibility about the Fed's renewed commitment to low inflation .

Hence, we see that this lack of credibility measured as inflation variance kept 10-year yields nearly 250bp higher than it would have been if the Fed had had the kind of credibility it had during the 1960s or after 1992.

More from For later read

How I created content in 2020

A thread...

Back in Aug 2016, I started creating content to share my experiences as an entrepreneur.

Over 3 years I had put out 1,200+ hours of content - posting every week without

Little did I know that something I started almost 4 years back would give my life an entirely new direction.

At the end of 2019, my biggest platform was LinkedIn with ~700K followers.

In Jan 2020, I decided to build a team that would help me with the content.

I ran a month long recruitment drive to hire a team of interns.

It comprised 4 detailed rounds - starting with my loved 20 questions, then an assignment, then a WhatsApp video round and finally F2F.

Through 1,200+ applications, I finally selected 6 profiles, starting March.

I am a firm believer in @peterthiel's one task, one person philosophy

So the team was structured such that everyone was responsible for ONLY one task

1. Content ideas

2. Videography

3. Video editing

4. LinkedIn (+TikTok) distribution

5. FB+IG distribution

6. YouTube distribution

A thread...

Back in Aug 2016, I started creating content to share my experiences as an entrepreneur.

Over 3 years I had put out 1,200+ hours of content - posting every week without

August 2016.

— Ankur Warikoo (@warikoo) October 2, 2020

It has been 3 months since LinkedIn had launched its video feature.

And I had been waiting for it to be activated on my profile.

A thread...

Little did I know that something I started almost 4 years back would give my life an entirely new direction.

At the end of 2019, my biggest platform was LinkedIn with ~700K followers.

In Jan 2020, I decided to build a team that would help me with the content.

I ran a month long recruitment drive to hire a team of interns.

It comprised 4 detailed rounds - starting with my loved 20 questions, then an assignment, then a WhatsApp video round and finally F2F.

Through 1,200+ applications, I finally selected 6 profiles, starting March.

I am a firm believer in @peterthiel's one task, one person philosophy

So the team was structured such that everyone was responsible for ONLY one task

1. Content ideas

2. Videography

3. Video editing

4. LinkedIn (+TikTok) distribution

5. FB+IG distribution

6. YouTube distribution

Part of what is going on here is that large sectors of evangelicalism are poorly equipped to help people deal with basic struggles, let alone the ubiquitous pornography addictions that most of their men have been enslaved to for years.

On the one hand, there's a high standard of holiness. On the other hand, there's a model of growth that is basically "Try Harder to Mean it More." Identify the relevant scriptural truth & believe it with all of your sincerity so that you may access the Holy Spirit's help to obey.

Helping sincere believers believe and obey the Bible facts is pretty much all the Holy Spirit does these days, other than convict us of our sins in light of the Bible facts.

If you know you are sincere and hate your sin and believe the right Bible facts as hard as you can but continue to be enslaved to your pornography addiction, what else left for you to do? Just Really, Just Really, Just Really Trust God and Give it to Him?

To suggest that there are other strategies available sounds to those formed in this model of growth like one is also suggesting that the Bible is insufficient, but it also suggests something just as threatening- that there are aspects of reality that are not immediately apparent.

There\u2019s this crazy horseshoe where where having a strong emphasis on human sinfulness just turns into a power washer that blasts all harm and wrong-doing down to the same level of things people (re: men) inevitably do given half a chance. https://t.co/BLOWzpf1RA

— Laura Robinson (@LauraRbnsn) February 13, 2021

On the one hand, there's a high standard of holiness. On the other hand, there's a model of growth that is basically "Try Harder to Mean it More." Identify the relevant scriptural truth & believe it with all of your sincerity so that you may access the Holy Spirit's help to obey.

Helping sincere believers believe and obey the Bible facts is pretty much all the Holy Spirit does these days, other than convict us of our sins in light of the Bible facts.

If you know you are sincere and hate your sin and believe the right Bible facts as hard as you can but continue to be enslaved to your pornography addiction, what else left for you to do? Just Really, Just Really, Just Really Trust God and Give it to Him?

To suggest that there are other strategies available sounds to those formed in this model of growth like one is also suggesting that the Bible is insufficient, but it also suggests something just as threatening- that there are aspects of reality that are not immediately apparent.

Nice to discover Judea Pearl ask a fundamental question. What's an 'inductive bias'?

I crucial step on the road towards AGI is a richer vocabulary for reasoning about inductive biases.

explores the apparent impedance mismatch between inductive biases and causal reasoning. But isn't the logical thinking required for good causal reasoning also not an inductive bias?

An inductive bias is what C.S. Peirce would call a habit. It is a habit of reasoning. Logical thinking is like a Platonic solid of the many kinds of heuristics that are discovered.

The kind of black and white logic that is found in digital computers is critical to the emergence of today's information economy. This of course is not the same logic that drives the general intelligence that lives in the same economy.

Help! What precisely is "inductive bias"? Some ML researchers are in the opinion that the machine learning category of \u2018inductive biases\u2019 can allow us to build a causal understanding of the world. My Ladder of Causation says: "This is mathematically impossible". Who is right? 1/

— Judea Pearl (@yudapearl) February 14, 2021

I crucial step on the road towards AGI is a richer vocabulary for reasoning about inductive biases.

explores the apparent impedance mismatch between inductive biases and causal reasoning. But isn't the logical thinking required for good causal reasoning also not an inductive bias?

An inductive bias is what C.S. Peirce would call a habit. It is a habit of reasoning. Logical thinking is like a Platonic solid of the many kinds of heuristics that are discovered.

The kind of black and white logic that is found in digital computers is critical to the emergence of today's information economy. This of course is not the same logic that drives the general intelligence that lives in the same economy.