2/x

But before we dive into the bill, a quick note from my soap box… This whole process is absurd. They JUST released a 5k+ page bill, and they are going to vote on it TODAY.

They aren't even pretending to have time to read what they're voting on anymore.

*Steps off soap box*

3/x

Ok... on to the meat. Let's start by answering the question that so many are already asking... “Will I be getting another #stimulus check?”

The answer, like last time, is “Maybe.”

Notably, the maximum stimulus amount per person this time around is $600.

4/x

Under the CARES Act, adults got $1,200 for themselves, and $500 for children as a ‘base amount.’ This time, it’s $600 for each person.

So, for instance, a single filer w/ no kids starts w/ base of $600. Family of five, like this👇starts w/ a base amount of $600 x 5 = $3k

5/x

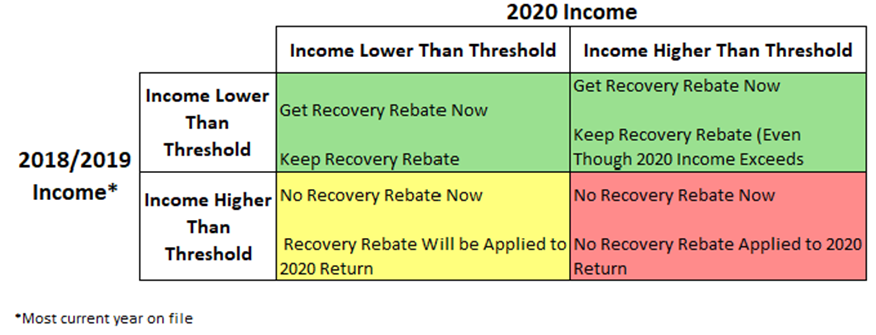

But those amounts" will be reduced once income exceeds the following thresholds:

Single: $75,000

Joint: $150,000

HOH: $112,500

As was the case under the CARES Act, the ‘base’ stimulus check will phase out by $5 for every $100 a taxpayer is over their applicable threshold.

6/x

Some thoughts...

- This is another 2020 refundable credit

- The checks will be paid now based on 2019 AGI

- Qualifications look the same as CARES (e.g., kids STILL only count if they can be claimed for the Child Tax Credit)

If your income is much different than 2019, see👇

7/x

Congress also addressed a BIG issue w/ 1st payments. What happens to payments made to dead people?

In short, they EXPLICITLY state people who died before 2020 do NOT get stimulus checks. Reading between lines, that SHOULD mean those who died early this year DO get them🤷♂️

8/x

Ahhh... seems Congress further clarified this point for Round 1 checks as well.

For those who have been following me closely, you know this was my prediction. And why I urged people to consider waiting to refund checks sent to 2020 decedents, despite contrary IRS guidance.

9/x

Moving on. You may recall that back in August, President Trump signed an Executive Order that allowed payroll taxes through the end of the year to be deferred (he wanted to eliminate them entirely, but lacked statutory authority).

Well, good news for some of those folks...

10/x

Originally, the amounts were to be repaid from Jan 21 - April 21. But the Act extends that to Dec 21.

Bottom line… deferrals still must be repaid, but can be spread over a longer time, so Q1 2021 cashflow will be a little bit better for those who deferred in Q4 2020.

11/x

As to who this pertains to, notably, employers were given the OPTION to participate.

Some did, but most didn’t b/c it was complex and, frankly, wasn’t all that great of a benefit for workers🙄

BUT Fed employees were FORCED to participate. So that's a good starting point.

12/

Of note to educators, if you spend $ on PPE or cleaning supplies for the classroom, those expenses can be used towards your Educator Expense deduction.

Unfortunately, no change to the $250 limit.

(Side note: Teachers should not have to shell out $ to keep classrooms safe)

13/

Back to BIG news... taxation (or rather, lack thereof) of forgiven #PaycheckProtectionProgram (#PPP) loans.

Mercifully, Congress has ended the debate. Businesses CAN deduct expenses paid w/ PPP funds. This DOES sort of provide a double benefit to business owners, but...

14/

It's worth noting many business owners kept employees on payroll ONLY b/c they had the #PPP loan.

Eliminating the deduction for those expenses would have resulted in potential hardship to those biz owners for doing what the law was designed to do... keep people on payroll.

15/

Nice little nugget here for #CPAs. Looks like Congress is going to let lenders forgo issuing a 1099 for forgiven PPP debt.

One less entry to make on the return, and 1,454,882 questions about why the client received a 1099 for a non-taxable event avoided!

16/

Wasn't aware this was really up for debate before, but Act clarifies that Coronavirus-Related Distributions CAN be made from Money Purchase plans.

Reminder: These distributions are allowed through 12/31/20. A similar provision is included though (more on this in a bit)

17/

Employers: The refundable payroll tax credits for sick + family leave created by Families First Act (pre-CARES Act legislation) are extended through March 2021.

Self-employed individuals are also given the option to use prior-year's net earnings instead of current year.

18/

OK... Let's get back to another BIG TICKET ITEM; the extension and expansion of the Paycheck Protection Program...

Perhaps the craziest thing in this bill... Congress just gave SBA 10 DAYS to write Regs... over Christmas. Somebody was clearly on Congress's naughty list.

19/

There's A LOT here on PPP.

For starters, all sorts of new qualifying expenses, including COVERED:

- Operations Expenditures

- Property Damage Costs

- Supplier Costs

- Worker Protection Expenditures

Also, PPP loans may have long-term legs. Officially moved to SBA Act...

20/

I'd surmise that part of this is that Congress may want to use some PPP loans as a tool in future disaster scenarios without having to literally re-write

the book again.

May we all be so lucky as to never need to take a PPP loan at any point in the future.

21/

Now... about those new eligible PPP expenses, what exactly are all those "Covered" expenses?🤔

Easier to show you than to tell you on this one.

See below👇

22/

Tangent: Going through this Section of the Act is a royal pain in the butt.

Not only is it a monstrous amount of legalese, but SO MUCH of it refers back to the CARES Act, so you kind of have to look at this bill, and splice it into the CARES Act to figure out what's up.

23/

Continuing the 2020 theme of making the shelf-life of my writing that of warm milk in the sun, Congress has also updated the choice of Covered Periods for PPP borrowers.

Now ALL borrowers can choose 8-week or 24-week period (choice was only allowed for pre-6/5/20 loans)

24/

BTW... did you notice the chalkboard on the last tweet. Not bad, eh?

I digress (this bill is 5,000+ pages, so that'll happen a few more times. You'll just have to bear w/ me)...

Back to work... While there has been speculation about potentially letting small(ish) PPP...

25/

loans receive automatic forgiveness, it appears that won't happen.

BUT, the Act mandates SBA create a 1-page-or-less Forgiveness App for PPP borrowers of less than $150k.

Ironic Congress instructed SBA to make a 1-page form via a 5k+ page law🤣

BTW, SBA has 24 days⏱️