Thread on the Molotov-Ribbentrop Pact:

1. In August, 1939, Stalin called on the UK and France to form an anti-fascist alliance. It was only after they rejected this proposal that the USSR signed the Molotov-Ribbentrop Pact to buy time in order to prepare for the war.

More from Economy

1/OK, let's take a little break from Coup Twitter, and think about an economic issue:

How can we build up the wealth of the middle class?

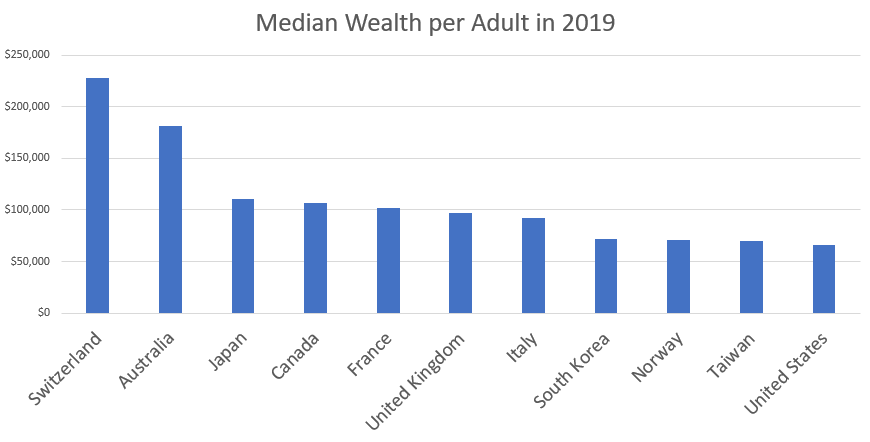

2/The typical American has surprisingly little wealth compared to the typical resident of many other developed countries.

This is a fact that is not widely known or appreciated.

3/Now, some people argue that stuff like Social Security or social insurance programs should be included in wealth. But I chose to focus on private wealth because I think having assets you can sell whenever you want is important to

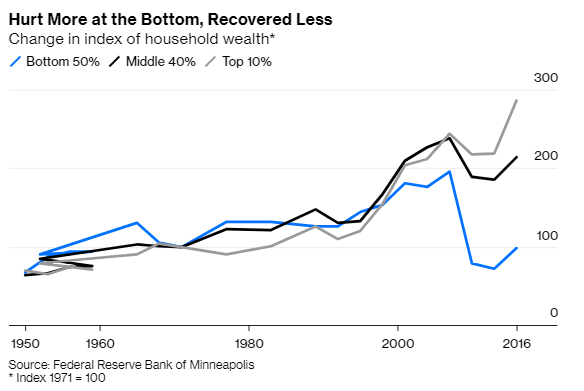

4/For many decades after World War 2, middle-class wealth in America was on a smooth upward trajectory.

Then the housing crash came, and all that changed. Suddenly the rich were still doing well but everyone else was seeing the end of their American Dream.

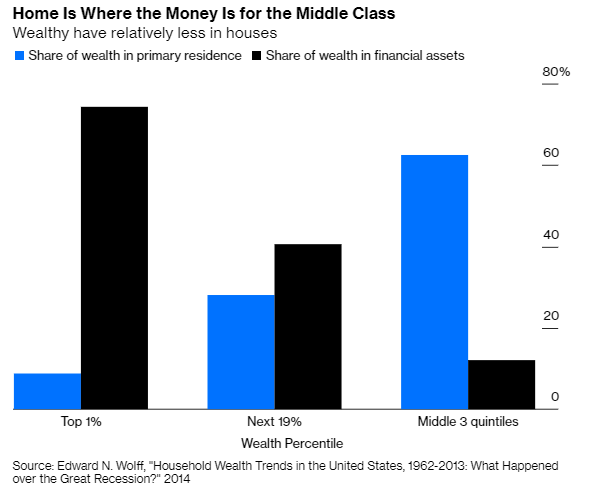

5/Why the divergence?

Because the American middle class has its wealth in houses -- specifically, in the houses they live in.

It's the rich who own stocks.

How can we build up the wealth of the middle class?

2/The typical American has surprisingly little wealth compared to the typical resident of many other developed countries.

This is a fact that is not widely known or appreciated.

3/Now, some people argue that stuff like Social Security or social insurance programs should be included in wealth. But I chose to focus on private wealth because I think having assets you can sell whenever you want is important to

Yes, these numbers don't include things like Social Security, just privately held wealth. They're not an attempt to capitalize every possible future income stream.

— Noahtogolpe \U0001f407 (@Noahpinion) January 10, 2021

4/For many decades after World War 2, middle-class wealth in America was on a smooth upward trajectory.

Then the housing crash came, and all that changed. Suddenly the rich were still doing well but everyone else was seeing the end of their American Dream.

5/Why the divergence?

Because the American middle class has its wealth in houses -- specifically, in the houses they live in.

It's the rich who own stocks.

You May Also Like

Ivor Cummins has been wrong (or lying) almost entirely throughout this pandemic and got paid handsomly for it.

He has been wrong (or lying) so often that it will be nearly impossible for me to track every grift, lie, deceit, manipulation he has pulled. I will use...

... other sources who have been trying to shine on light on this grifter (as I have tried to do, time and again:

Example #1: "Still not seeing Sweden signal versus Denmark really"... There it was (Images attached).

19 to 80 is an over 300% difference.

Tweet: https://t.co/36FnYnsRT9

Example #2 - "Yes, I'm comparing the Noridcs / No, you cannot compare the Nordics."

I wonder why...

Tweets: https://t.co/XLfoX4rpck / https://t.co/vjE1ctLU5x

Example #3 - "I'm only looking at what makes the data fit in my favour" a.k.a moving the goalposts.

Tweets: https://t.co/vcDpTu3qyj / https://t.co/CA3N6hC2Lq

He has been wrong (or lying) so often that it will be nearly impossible for me to track every grift, lie, deceit, manipulation he has pulled. I will use...

... other sources who have been trying to shine on light on this grifter (as I have tried to do, time and again:

Ivor Cummins BE (Chem) is a former R&D Manager at HP (sourcre: https://t.co/Wbf5scf7gn), turned Content Creator/Podcast Host/YouTube personality. (Call it what you will.)

— Steve (@braidedmanga) November 17, 2020

Example #1: "Still not seeing Sweden signal versus Denmark really"... There it was (Images attached).

19 to 80 is an over 300% difference.

Tweet: https://t.co/36FnYnsRT9

Example #2 - "Yes, I'm comparing the Noridcs / No, you cannot compare the Nordics."

I wonder why...

Tweets: https://t.co/XLfoX4rpck / https://t.co/vjE1ctLU5x

Example #3 - "I'm only looking at what makes the data fit in my favour" a.k.a moving the goalposts.

Tweets: https://t.co/vcDpTu3qyj / https://t.co/CA3N6hC2Lq