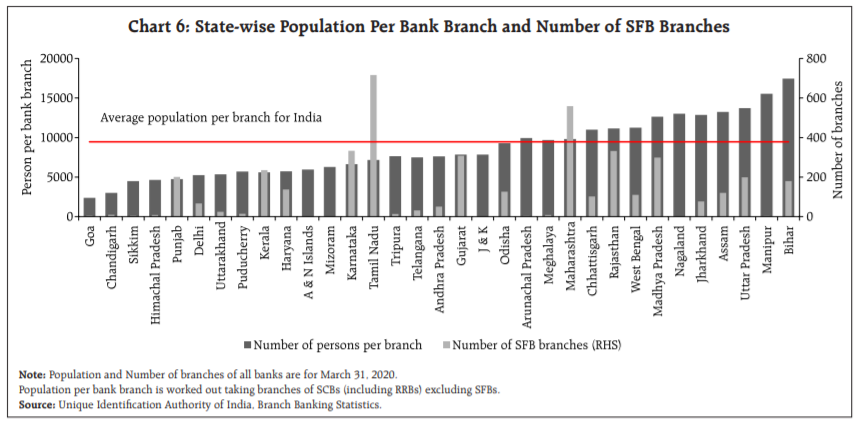

🧵While we in Fintech are Hoping for Challenger/Neo Banking Licences from RBI. Let's understand more about Small Finance Bank and from their success, try to see if a balance between Profitability (for business) and Financial Inclusion (for RBI) can be made for future usecase?👇

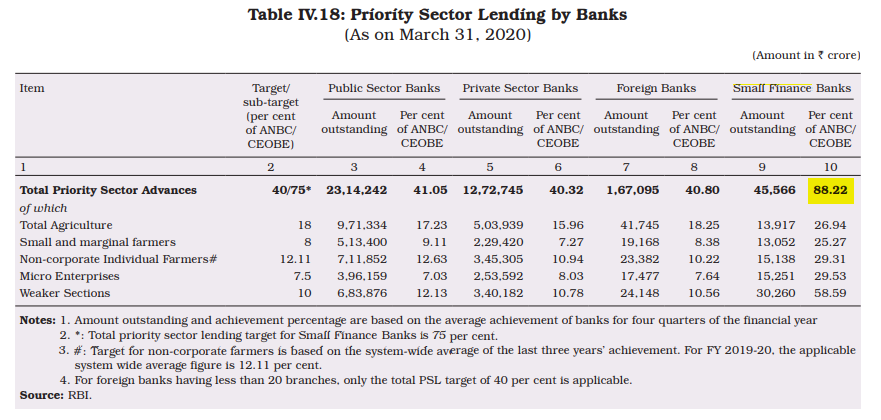

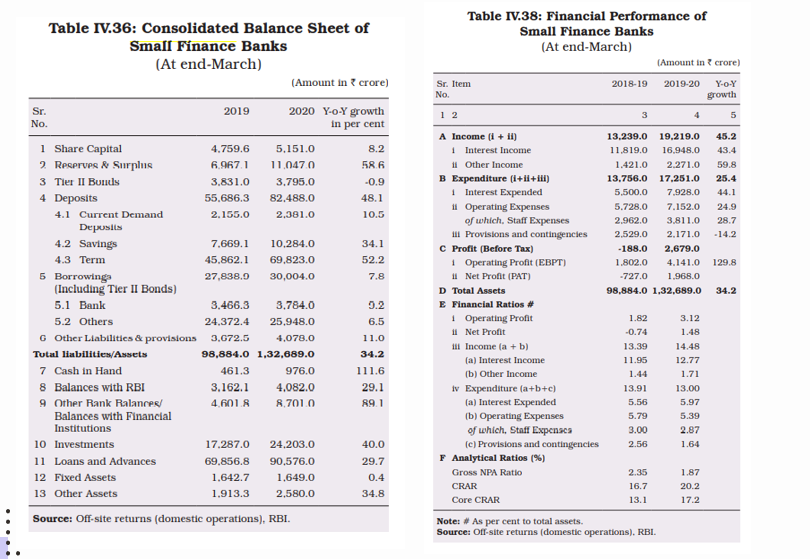

1. Priority Sector Lending (75% of their total lending) and 2. Branches for Unbanked (SFB were required to have 25% of their branches in rural unbanked centres (population shall be less than 10,000)

More from Business

1/An interesting thing happened tonight. I was scrolling through clubhouse and found WileyCEO, Godfather of Grime (kicked off Twitter in July for antisemitic tweets) speaking. So I tweeted this (and included a screen shot, later deleted as I found out TOS don't allow it ...

2/ ... and several folks also asked me to remove it which I promptly did afterwards).... Coming into the CH room, I fully intended to confront him about how hurtful his comments in July were. But as I listened to the folks in the room, I decided to go a different direction ....

3/ the conversation jumped around, covered many topics and there were between 8-14 people up on stage. But a recurring thread was discussion of racism, bigotry, comparison of it in the US vs UK vs elsewhere.

4/ when I got a chance to speak, I had 5 bullets written down: a) we should harness technology and capitalism to make reparations for what America did to Black people. I gave https://t.co/SlrW8zCd58 (a project a couple friends co-started) as an example) ...

5/ b) capitalism and product know-how and technology can be harnessed for social justice c) historically oppressed minorities need to stick together and lastly, d) "Wiley, how could you say such hurtful things about Jews as a people?" That's what I had ready to say, anyway.

2/ ... and several folks also asked me to remove it which I promptly did afterwards).... Coming into the CH room, I fully intended to confront him about how hurtful his comments in July were. But as I listened to the folks in the room, I decided to go a different direction ....

3/ the conversation jumped around, covered many topics and there were between 8-14 people up on stage. But a recurring thread was discussion of racism, bigotry, comparison of it in the US vs UK vs elsewhere.

4/ when I got a chance to speak, I had 5 bullets written down: a) we should harness technology and capitalism to make reparations for what America did to Black people. I gave https://t.co/SlrW8zCd58 (a project a couple friends co-started) as an example) ...

5/ b) capitalism and product know-how and technology can be harnessed for social justice c) historically oppressed minorities need to stick together and lastly, d) "Wiley, how could you say such hurtful things about Jews as a people?" That's what I had ready to say, anyway.

Introducing "The Balloon Effect"

Many businesses & creators have experienced a similar pattern of success.

From @MrBeastYT and @MorningBrew to @oatly and @Rovio.

Let's break down what "The Balloon Effect" is and examples of it in real life.

Keep reading 👇

1/ What is "The Balloon Effect"?

It is a particular pattern of growth.

It is not Instagram's growth trajectory.

It is not https://t.co/5axsTUKek6's growth trajectory.

"The Balloon Effect" is defined by several years of hard work & grit complemented by slow, linear growth.

2/ And then one day, one month, or one quarter...everything changes.

A business hits a tipping point and its trajectory shifts entirely.

Gradual growth turns to exponential growth & your brand and your size explode.

Like a step function.

3/ Now, you're probably wondering.

Why is it called "The Balloon Effect"?

Because filling/popping a water balloon follows the exact pattern I just described (and so many businesses experience).

Long unsexy slog 👉 Exponential tipping point.

4/ Initially, you turn on the faucet & water takes up space in the empty balloon.

Through effort you open the faucet, yet the results are unexciting.

But it's what must be done for water (or growth) to happen at all.

It's not sexy, but it's necessary.

Many businesses & creators have experienced a similar pattern of success.

From @MrBeastYT and @MorningBrew to @oatly and @Rovio.

Let's break down what "The Balloon Effect" is and examples of it in real life.

Keep reading 👇

1/ What is "The Balloon Effect"?

It is a particular pattern of growth.

It is not Instagram's growth trajectory.

It is not https://t.co/5axsTUKek6's growth trajectory.

"The Balloon Effect" is defined by several years of hard work & grit complemented by slow, linear growth.

2/ And then one day, one month, or one quarter...everything changes.

A business hits a tipping point and its trajectory shifts entirely.

Gradual growth turns to exponential growth & your brand and your size explode.

Like a step function.

3/ Now, you're probably wondering.

Why is it called "The Balloon Effect"?

Because filling/popping a water balloon follows the exact pattern I just described (and so many businesses experience).

Long unsexy slog 👉 Exponential tipping point.

4/ Initially, you turn on the faucet & water takes up space in the empty balloon.

Through effort you open the faucet, yet the results are unexciting.

But it's what must be done for water (or growth) to happen at all.

It's not sexy, but it's necessary.

You May Also Like

So friends here is the thread on the recommended pathway for new entrants in the stock market.

Here I will share what I believe are essentials for anybody who is interested in stock markets and the resources to learn them, its from my experience and by no means exhaustive..

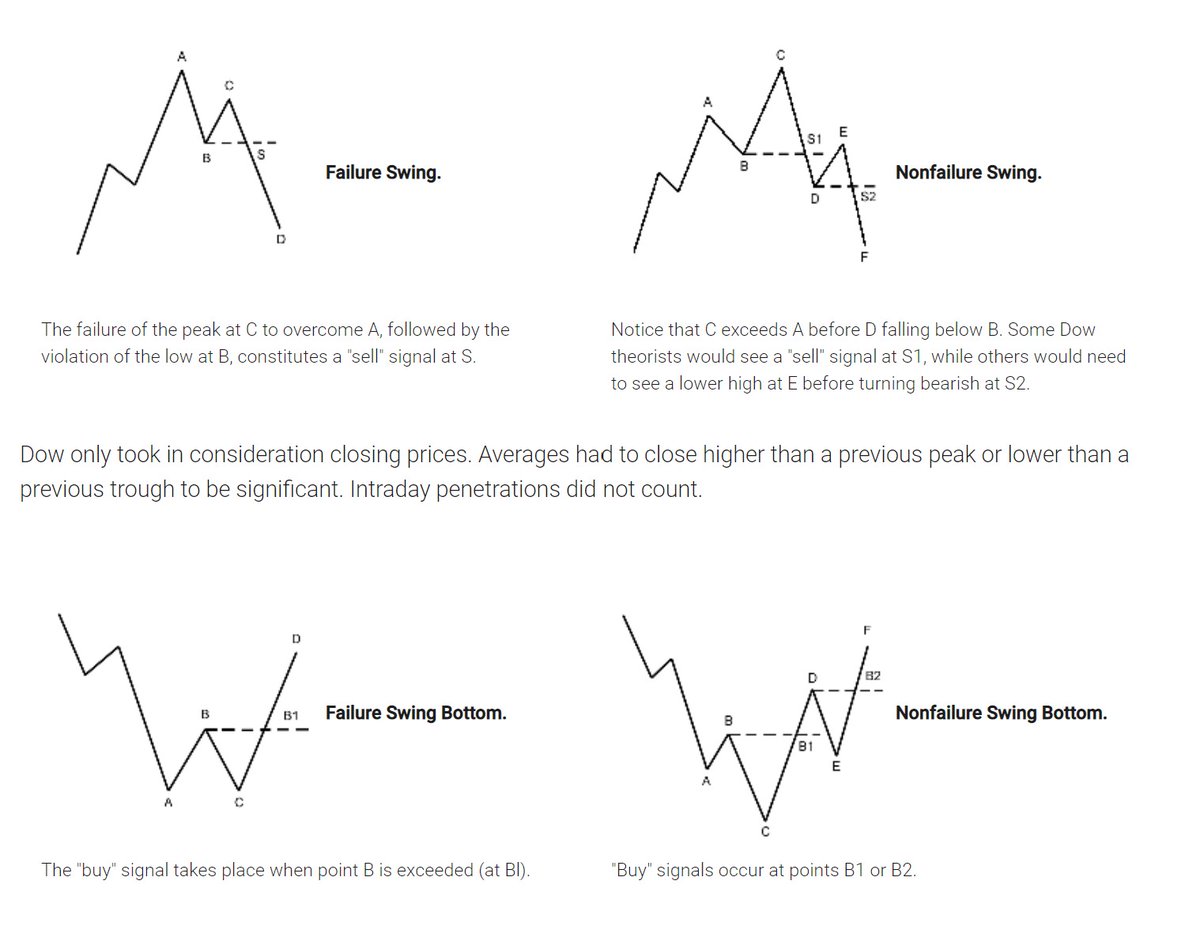

First the very basic : The Dow theory, Everybody must have basic understanding of it and must learn to observe High Highs, Higher Lows, Lower Highs and Lowers lows on charts and their

Even those who are more inclined towards fundamental side can also benefit from Dow theory, as it can hint start & end of Bull/Bear runs thereby indication entry and exits.

Next basic is Wyckoff's Theory. It tells how accumulation and distribution happens with regularity and how the market actually

Dow theory is old but

Here I will share what I believe are essentials for anybody who is interested in stock markets and the resources to learn them, its from my experience and by no means exhaustive..

First the very basic : The Dow theory, Everybody must have basic understanding of it and must learn to observe High Highs, Higher Lows, Lower Highs and Lowers lows on charts and their

Even those who are more inclined towards fundamental side can also benefit from Dow theory, as it can hint start & end of Bull/Bear runs thereby indication entry and exits.

Next basic is Wyckoff's Theory. It tells how accumulation and distribution happens with regularity and how the market actually

Dow theory is old but

Old is Gold....

— Professor (@DillikiBiili) January 23, 2020

this Bharti Airtel chart is a true copy of the Wyckoff Pattern propounded in 1931....... pic.twitter.com/tQ1PNebq7d

MASTER THREAD on Short Strangles.

Curated the best tweets from the best traders who are exceptional at managing strangles.

• Positional Strangles

• Intraday Strangles

• Position Sizing

• How to do Adjustments

• Plenty of Examples

• When to avoid

• Exit Criteria

How to sell Strangles in weekly expiry as explained by boss himself. @Mitesh_Engr

• When to sell

• How to do Adjustments

• Exit

Beautiful explanation on positional option selling by @Mitesh_Engr

Sir on how to sell low premium strangles yourself without paying anyone. This is a free mini course in

1st Live example of managing a strangle by Mitesh Sir. @Mitesh_Engr

• Sold Strangles 20% cap used

• Added 20% cap more when in profit

• Booked profitable leg and rolled up

• Kept rolling up profitable leg

• Booked loss in calls

• Sold only

2nd example by @Mitesh_Engr Sir on converting a directional trade into strangles. Option Sellers can use this for consistent profit.

• Identified a reversal and sold puts

• Puts decayed a lot

• When achieved 2% profit through puts then sold

Curated the best tweets from the best traders who are exceptional at managing strangles.

• Positional Strangles

• Intraday Strangles

• Position Sizing

• How to do Adjustments

• Plenty of Examples

• When to avoid

• Exit Criteria

How to sell Strangles in weekly expiry as explained by boss himself. @Mitesh_Engr

• When to sell

• How to do Adjustments

• Exit

1. Let's start option selling learning.

— Mitesh Patel (@Mitesh_Engr) February 10, 2019

Strangle selling. ( I am doing mostly in weekly Bank Nifty)

When to sell? When VIX is below 15

Assume spot is at 27500

Sell 27100 PE & 27900 CE

say premium for both 50-50

If bank nifty will move in narrow range u will get profit from both.

Beautiful explanation on positional option selling by @Mitesh_Engr

Sir on how to sell low premium strangles yourself without paying anyone. This is a free mini course in

Few are selling 20-25 Rs positional option selling course.

— Mitesh Patel (@Mitesh_Engr) November 3, 2019

Nothing big deal in that.

For selling weekly option just identify last week low and high.

Now from that low and high keep 1-1.5% distance from strike.

And sell option on both side.

1/n

1st Live example of managing a strangle by Mitesh Sir. @Mitesh_Engr

• Sold Strangles 20% cap used

• Added 20% cap more when in profit

• Booked profitable leg and rolled up

• Kept rolling up profitable leg

• Booked loss in calls

• Sold only

Sold 29200 put and 30500 call

— Mitesh Patel (@Mitesh_Engr) April 12, 2019

Used 20% capital@44 each

2nd example by @Mitesh_Engr Sir on converting a directional trade into strangles. Option Sellers can use this for consistent profit.

• Identified a reversal and sold puts

• Puts decayed a lot

• When achieved 2% profit through puts then sold

Already giving more than 2% return in a week. Now I will prefer to sell 32500 call at 74 to make it strangle in equal ratio.

— Mitesh Patel (@Mitesh_Engr) February 7, 2020

To all. This is free learning for you. How to play option to make consistent return.

Stay tuned and learn it here free of cost. https://t.co/7J7LC86oW0