There are various Options Greeks like: Delta, Gamma, Vega, Rho, Theta.

A complete guide on how these #Option Greeks impact option price.

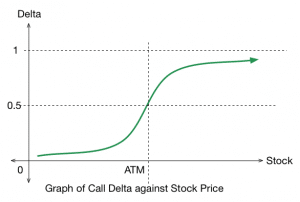

1/ Delta:

Delta is a measure of the sensitivity of an option’s price changes relative to the changes in the underlying asset’s price. In other words, if the price of the underlying asset increases by 1 points, the price of the option will change by delta amount.

Call option has positive delta, and put option has a negative delta.

As the options become ITM, the value of delta tends towards +1 for call and -1 for put.

Delta is important greeks to determine the hedge ratio for investors who want to hedge their portfolio.

2/ Gamma:

Gamma (Γ) is a measure of the delta’s change relative to the changes in the price of the underlying asset.

If the price of the underlying asset increases by 1 points, the option’s delta will change by the gamma amount.

Long options (call/put) have positive Gamma.

Gamma decreases as options move away from ATM, i.e. as options become OTM/ITM.

Think like this, Delta is basically the velocity and gamma is acceleration as taught in the physics.