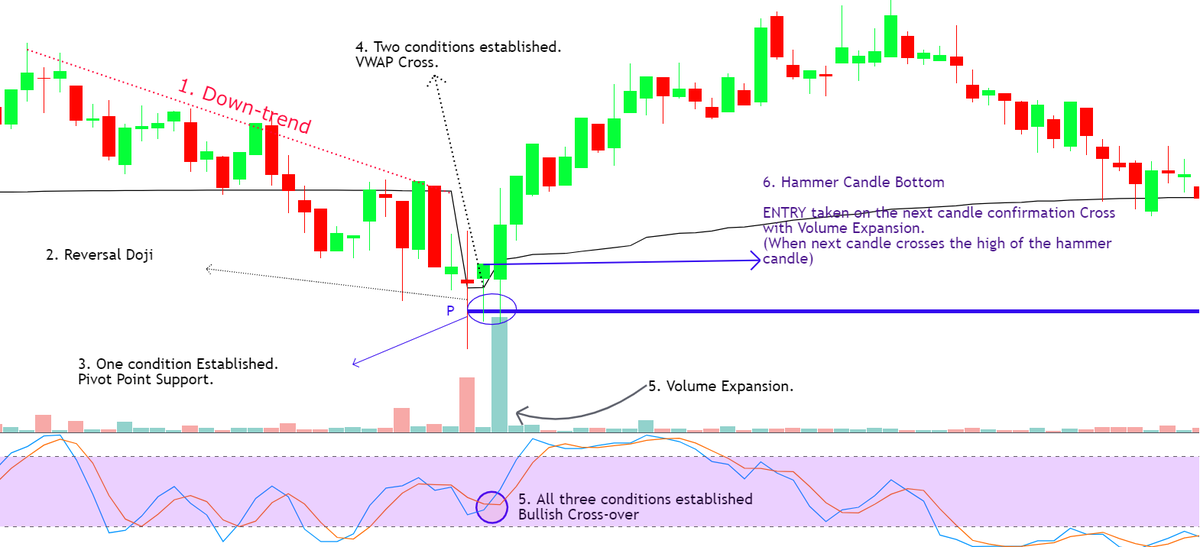

Suppose that for a given setup, price hits target before it reaches invalidation 70% of the time. Great, right? But getting filled is not guaranteed.

The more right you are about your trade setup, the less likely you are to get filled

By extension, getting filled actually lowers the Bayesian probability that you are right

Should I sacrifice some RRR to get filled more often?

The eternal dilemma of contrarian trading

Suppose that for a given setup, price hits target before it reaches invalidation 70% of the time. Great, right? But getting filled is not guaranteed.

Scenario 2: If only 40 out of 100 limits get filled, expected hit rate is 25%

Both scenarios have 30 losses in expectation, but the hit rate in the first is >2x better simply because more trades were taken

EV = hitrate * avg_win_R + (1-hitrate) * avg_loss_R

So we want argmax(EV), and we can compute this by seeing how hitrate and avg_win_R affect the EV of the setup.

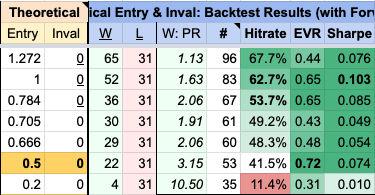

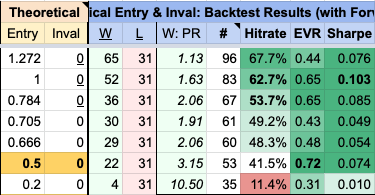

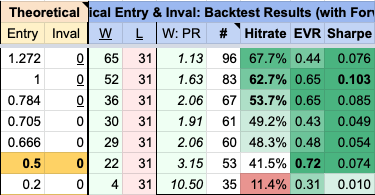

Here's a real example where I completed this optimization.

- the average win R tends to increase ("W:PR")

- the number of losses ("L") stays constant at 31

- but the number of trades taken decreases ("#")

- so the hit rate decreases, from a max of 67.7% to a min of 11.4%.

- Understand the tradeoff between RRR and hit rate. I talked about limit orders in this thread but a similar relationship applies to market entries too

- There are no easy answers here. Only the prospect of hard work collecting good data and learning from it.

💪

@Captain_Kole1 @melodyofrhythm @ape_rture @realadamli @7ommyZero @voicelessFvoice

More from Trading

You May Also Like

A list of cool websites you might now know about

A thread 🧵

1) Learn Anything - Search tools for knowledge discovery that helps you understand any topic through the most efficient

2) Grad Speeches - Discover the best commencement speeches.

This website is made by me

3) What does the Internet Think - Find out what the internet thinks about anything

4) https://t.co/vuhT6jVItx - Send notes that will self-destruct after being read.

A thread 🧵

1) Learn Anything - Search tools for knowledge discovery that helps you understand any topic through the most efficient

2) Grad Speeches - Discover the best commencement speeches.

This website is made by me

3) What does the Internet Think - Find out what the internet thinks about anything

4) https://t.co/vuhT6jVItx - Send notes that will self-destruct after being read.

I just finished Eric Adler's The Battle of the Classics, and wanted to say something about Joel Christiansen's review linked below. I am not sure what motivates the review (I speculate a bit below), but it gives a very misleading impression of the book. 1/x

The meat of the criticism is that the history Adler gives is insufficiently critical. Adler describes a few figures who had a great influence on how the modern US university was formed. It's certainly critical: it focuses on the social Darwinism of these figures. 2/x

Other insinuations and suggestions in the review seem wildly off the mark, distorted, or inappropriate-- for example, that the book is clickbaity (it is scholarly) or conservative (hardly) or connected to the events at the Capitol (give me a break). 3/x

The core question: in what sense is classics inherently racist? Classics is old. On Adler's account, it begins in ancient Rome and is revived in the Renaissance. Slavery (Christiansen's primary concern) is also very old. Let's say classics is an education for slaveowners. 4/x

It's worth remembering that literacy itself is elite throughout most of this history. Literacy is, then, also the education of slaveowners. We can honor oral and musical traditions without denying that literacy is, generally, good. 5/x

As someone\u2019s who\u2019s read the book, this review strikes me as tremendously unfair. It mostly faults Adler for not writing the book the reviewer wishes he had! https://t.co/pqpt5Ziivj

— Teresa M. Bejan (@tmbejan) January 12, 2021

The meat of the criticism is that the history Adler gives is insufficiently critical. Adler describes a few figures who had a great influence on how the modern US university was formed. It's certainly critical: it focuses on the social Darwinism of these figures. 2/x

Other insinuations and suggestions in the review seem wildly off the mark, distorted, or inappropriate-- for example, that the book is clickbaity (it is scholarly) or conservative (hardly) or connected to the events at the Capitol (give me a break). 3/x

The core question: in what sense is classics inherently racist? Classics is old. On Adler's account, it begins in ancient Rome and is revived in the Renaissance. Slavery (Christiansen's primary concern) is also very old. Let's say classics is an education for slaveowners. 4/x

It's worth remembering that literacy itself is elite throughout most of this history. Literacy is, then, also the education of slaveowners. We can honor oral and musical traditions without denying that literacy is, generally, good. 5/x