They’re a fintech lending, e-commerce focused, service that allows nonprime customers to borrow money and purchase durable goods such as: Fridge’s, Tables, Couches, etc

Thread: Bull Case on $FSRV

$FSRV is a great investment due to strong balance sheet, incredible growth in both earnings and revenue, and serve a competitive niche within this fintech market. I am very excited to be apart of this, undervalued, long term investment opportunity:

They’re a fintech lending, e-commerce focused, service that allows nonprime customers to borrow money and purchase durable goods such as: Fridge’s, Tables, Couches, etc

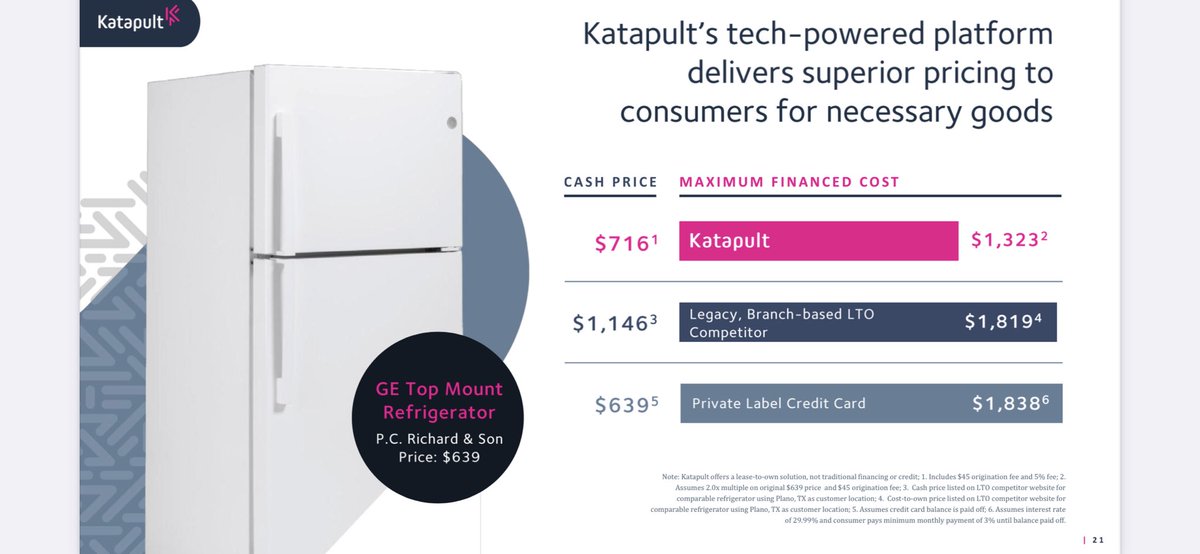

Some consumers with little to no credit often times don’t get approved, and it can be costly. Katapult leverages AI and ML to allocate money to them CHEAPER and faster than ever before.

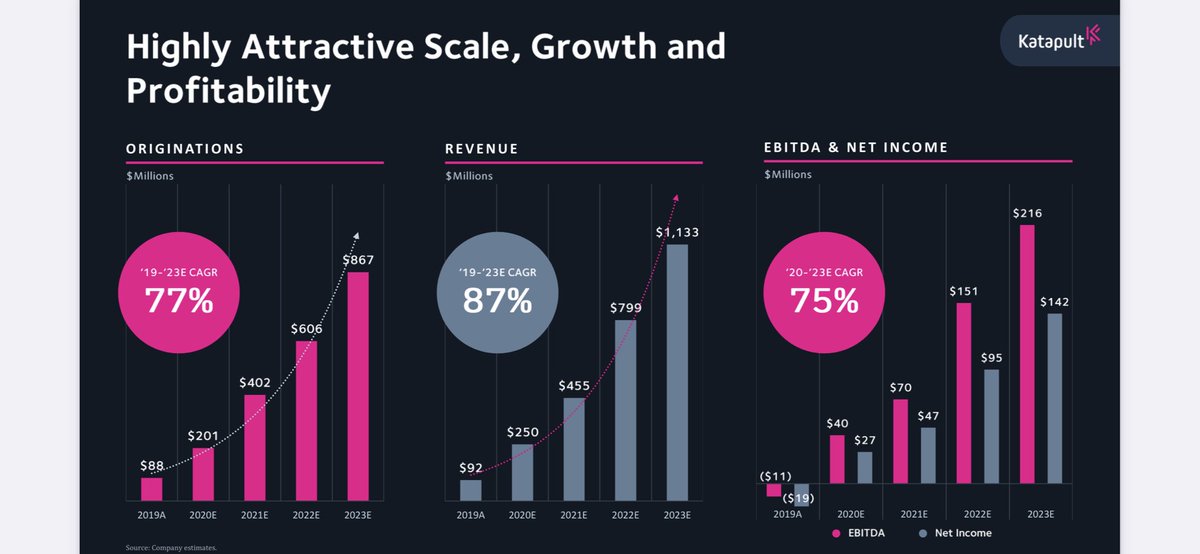

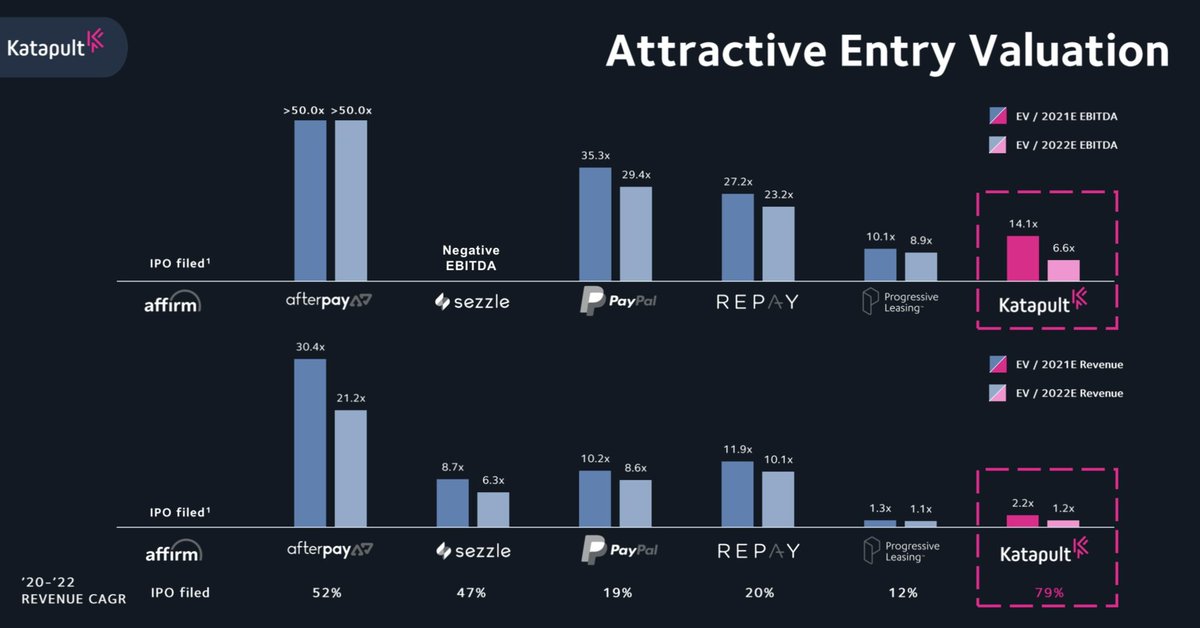

They have both grown revenue AND EBITDA at astounding rates. They hit profitability this year and grew 171% YoY. They project they will have a CAGR of EBITDA and Net Income at 75% 🤯🤯

This is a profit and growth monster, an investors dream!

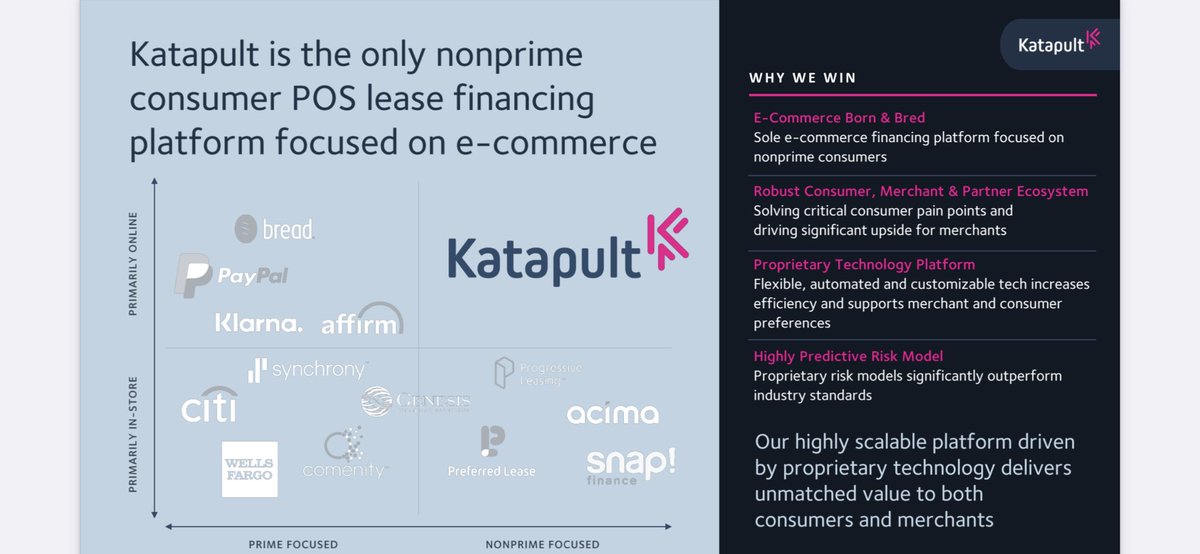

Lending isn’t a new service, and neither is leveraging AI/ML. But Katapult’s customer segment is niche, as nobody else wants to do it. They stand in their own quadrant, providing a long runway for niche growth.

They’re very forward looking and also a younger company. They still have not penetrated their total market or brought awareness to their solution for their total market. They have a clear strategy to do this and diversify their product.

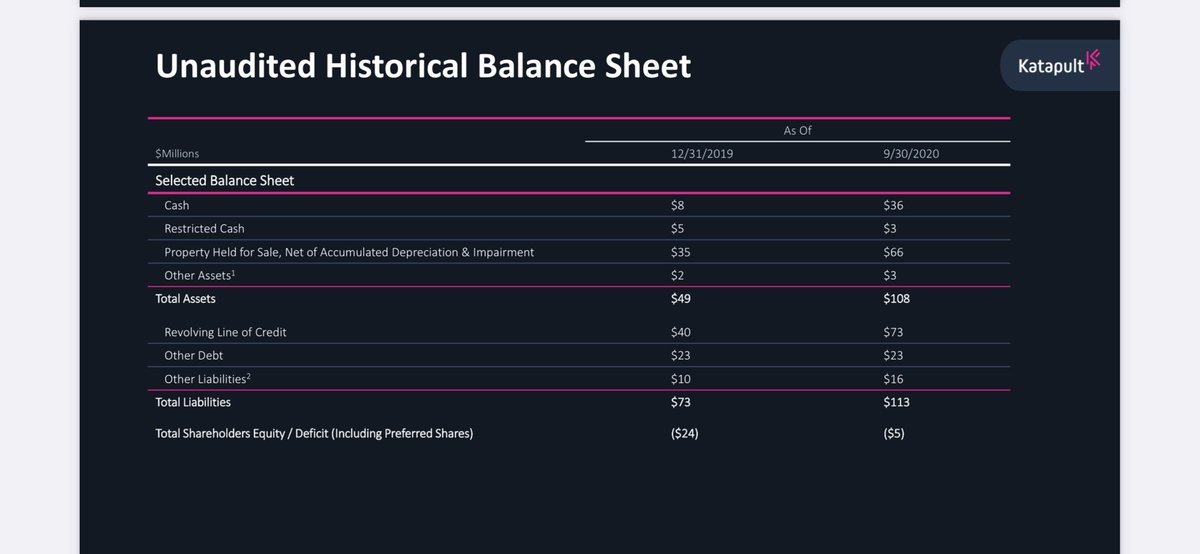

This is one where I’ve seen a few investors stumble up on when they see that big ‘liabilities’ number. But one must understand what “revolving line of credit” means. Once you do, one can assume they’re using the liquidity to lend more.

YES! 1,000x over yes. Affirm, their competitors/partner, will be going the IPO route soon and will, without a doubt, be over valued. With a high CAGR, attractive EBITDA valuation, and attractive revenue valuation. This is a buy.

More from Trading

𝗡𝗶𝗳𝘁𝘆-𝗕𝗮𝗻𝗸𝗻𝗶𝗳𝘁𝘆 𝗢𝗽𝘁𝗶𝗼𝗻 𝗕𝘂𝘆𝗶𝗻𝗴 𝗦𝘁𝗿𝗮𝘁𝗲𝗴𝘆

Complete Backtest and Indicator link

🧵 A Thread 🧵

𝗦𝗲𝘁𝘂𝗽:

🔸 Monthly Option Buying

🔸 50 ema on 3 min timeframe

🔸 Supertrend 10 , 3

🔸 Chart : Banknifty , Nifty Futures as we backtested on futures

🔸 Entry 9:20 to 3:00

🔸 Max 3 Entries per day

🔸 Premium nearest to 200 Rs only

[2/18]

Why Monthly Option buying ?

🔸 Less theta decay compared to weekly options

🔸 Less Volatility

🔸 Supertrend and MA Settings

[3/18]

🔸 Indicator Link

🔸 Click on the below 𝘭𝘪𝘯𝘬 -> 𝘈𝘥𝘥 𝘵𝘰 𝘍𝘢𝘷𝘰𝘶𝘳𝘪𝘵𝘦𝘴 -> 𝘈𝘥𝘥 𝘰𝘯 𝘊𝘩𝘢𝘳𝘵 from favourites and start using it !

🔸 https://t.co/zVXavqLBto

[4/18]

𝗜𝗻𝗱𝗶𝗰𝗮𝘁𝗼𝗿 𝗦𝗲𝘁𝘁𝗶𝗻𝗴𝘀 :

🔸 Max 6 Trades per day ( Both CE and PE buy)

🔸 Timings 9:20 am to 3:00 pm

🔸 Supertrend : 10,3

🔸 Moving Average 50 ema

[5/18]

Complete Backtest and Indicator link

🧵 A Thread 🧵

𝗦𝗲𝘁𝘂𝗽:

🔸 Monthly Option Buying

🔸 50 ema on 3 min timeframe

🔸 Supertrend 10 , 3

🔸 Chart : Banknifty , Nifty Futures as we backtested on futures

🔸 Entry 9:20 to 3:00

🔸 Max 3 Entries per day

🔸 Premium nearest to 200 Rs only

[2/18]

Why Monthly Option buying ?

🔸 Less theta decay compared to weekly options

🔸 Less Volatility

🔸 Supertrend and MA Settings

[3/18]

🔸 Indicator Link

🔸 Click on the below 𝘭𝘪𝘯𝘬 -> 𝘈𝘥𝘥 𝘵𝘰 𝘍𝘢𝘷𝘰𝘶𝘳𝘪𝘵𝘦𝘴 -> 𝘈𝘥𝘥 𝘰𝘯 𝘊𝘩𝘢𝘳𝘵 from favourites and start using it !

🔸 https://t.co/zVXavqLBto

[4/18]

𝗜𝗻𝗱𝗶𝗰𝗮𝘁𝗼𝗿 𝗦𝗲𝘁𝘁𝗶𝗻𝗴𝘀 :

🔸 Max 6 Trades per day ( Both CE and PE buy)

🔸 Timings 9:20 am to 3:00 pm

🔸 Supertrend : 10,3

🔸 Moving Average 50 ema

[5/18]